200 years of investing: why time helps investors but does not guarantee success

Almost everyone has a compelling reason to invest for the long term: to secure a decent retirement, save for their children's education, help them with their first mortgage payment, or simply build up a nest egg for a rainy day. Economist Denis Elakhovsky studied the history of various assets' performance not just over the long term, but over the super-long term, spanning decades and even longer.

The yield hierarchy: facts versus illusions

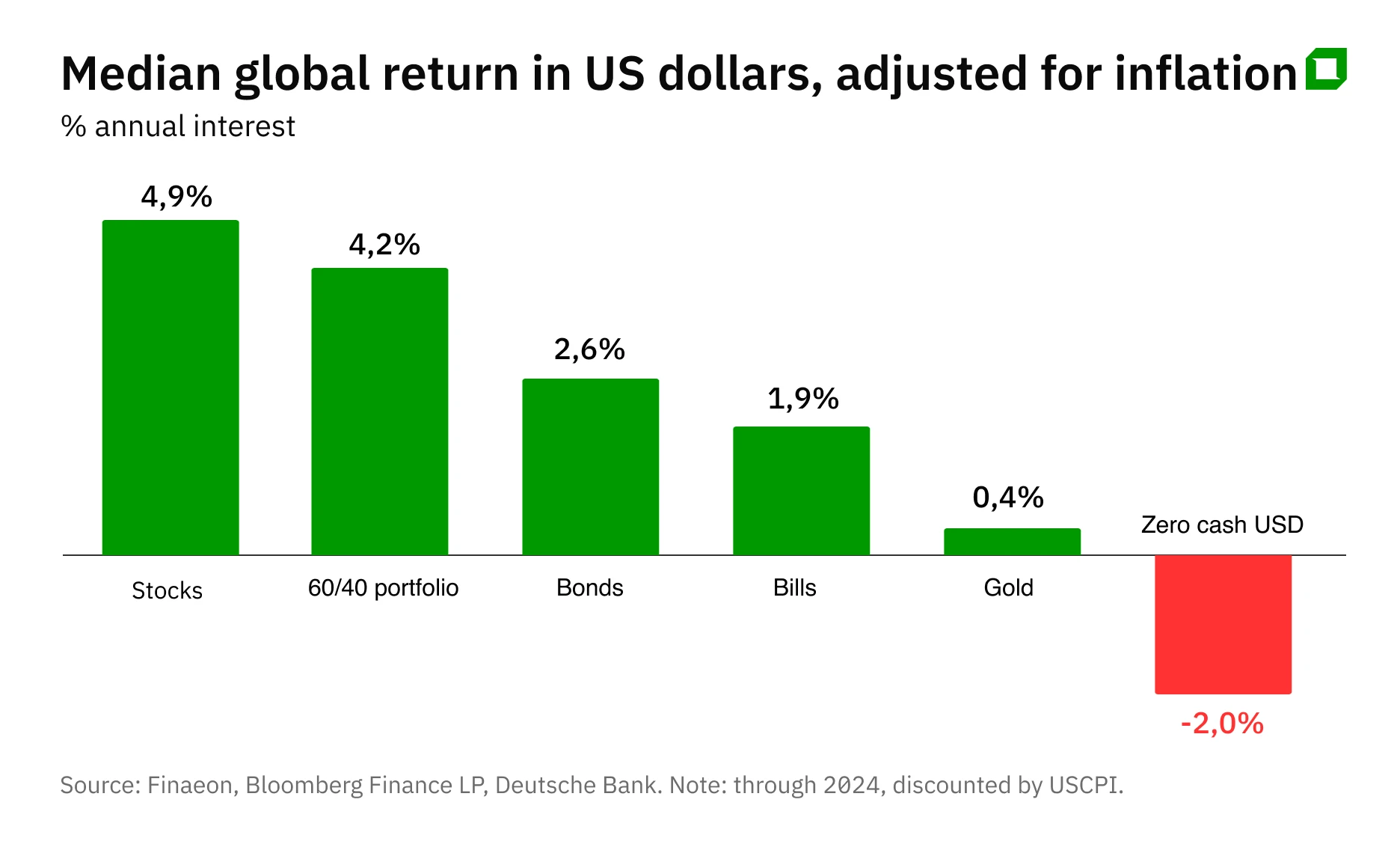

A large-scale study by Deutsche Bank experts analyzed the performance of investments in 56 countries over the past 200 years, from 1824 to 2024.

The main conclusion from two centuries of data sounds optimistic: investors have consistently been rewarded for taking risks. Looking at the median global return in US dollars adjusted for inflation, there are no surprises: stocks generated the highest returns at 4.9% per annum, while cash generated a real loss of 2% per annum.

The conclusion seems simple: buy stocks and wait. But hidden in the details are pitfalls that can wipe out the results of even the most disciplined investor.

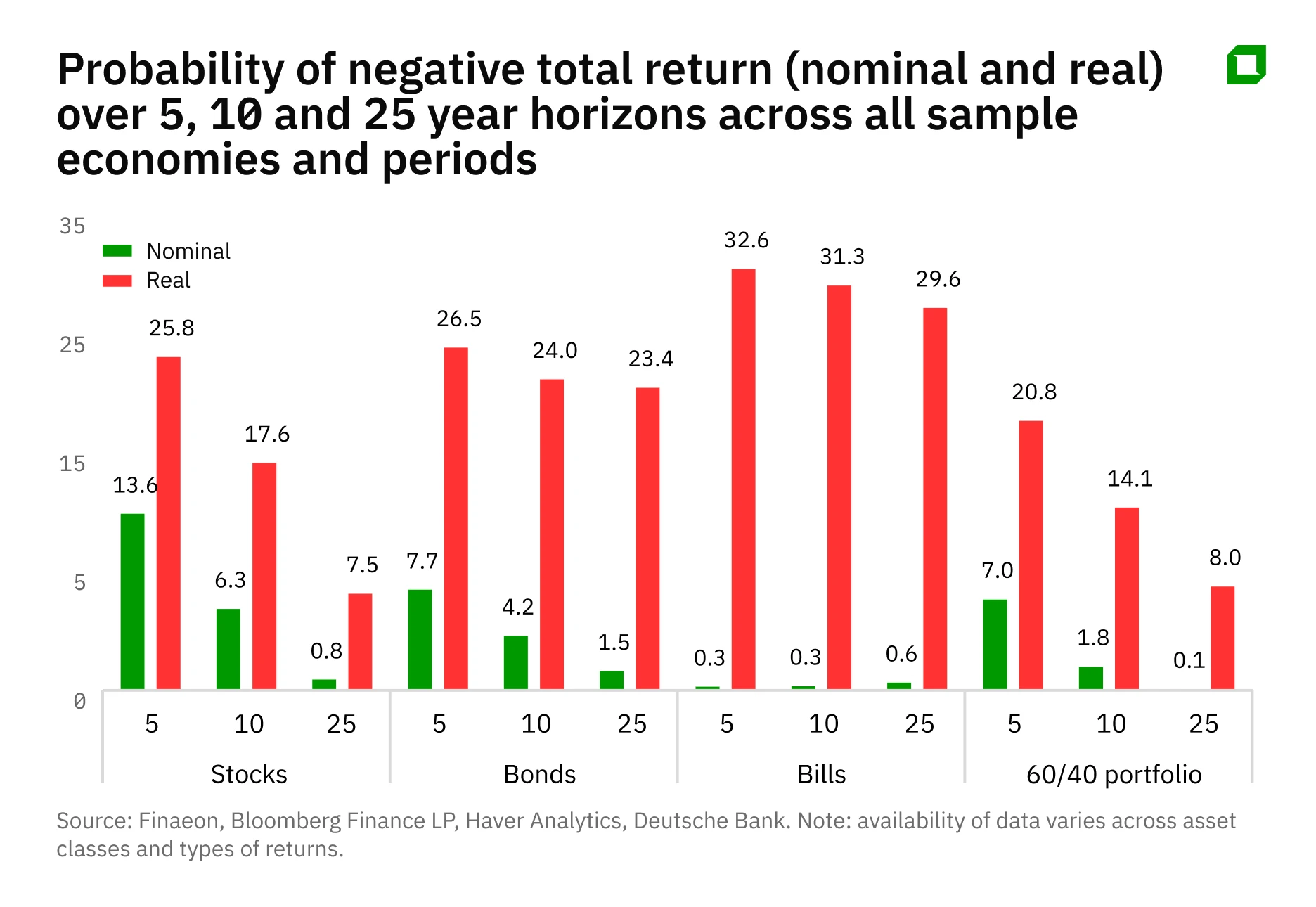

Pitfall #1: Time is on your side, but it does not guarantee success.

Deutsche Bank introduces a practical metric: the probability that real returns will be negative. Over a five-year horizon, stocks underperform inflation in 25.8% of cases. Over a 25-year horizon, this risk falls to 7.5%, but still does not disappear completely. A mixed portfolio — 60% stocks / 40% bonds — has historically performed better: in the short term, the risk of losing to inflation is lower than for a portfolio consisting of 100% stocks, but over a 25-year horizon, this advantage of the 60/40 strategy evaporates.

The moral is simple: if your goals are closer to the 5-7 year horizon, the "stocks always go up" strategy may prove unprofitable in a quarter of cases.

Pitfall #2: "Better deals" does not mean "any deal is better."

Long-term index data almost always looks good. The problem is that the index is built from survivors and winners, while real investors often choose individual stocks. And these are not always the companies that drive the entire market upward.

Hendrik Bessembinder's work paints a sobering picture of the US: over the past 100 years, most individual stocks have yielded lower returns than short-term Treasury bonds.

The practical conclusion here is boring but salutary: unless you are building a career as a professional stock analyst, broad diversification and index solutions are often much more productive than presumptuous stock picking.

Pitfall #3: You're not buying the market, you're buying the price

The popular idea of "just buy the index" also has its drawbacks. A study by Deutsche Bank clearly shows how important current price levels are when building long-term portfolios. Markets with low starting ratios (P/E) yielded an average annual return of 20.2%, while "expensive" markets yielded only 11.4%. The gap is enormous.

Campbell and Schiller'swork complements this conclusion: valuation multiples and dividend yields are an excellent tool for forecasting over a decade, but completely useless for timing the "here and now." If you enter the market at peak valuations—as is currently the case in the US based on the CAPE ratio—be prepared for a very likely long period of near-zero real returns.

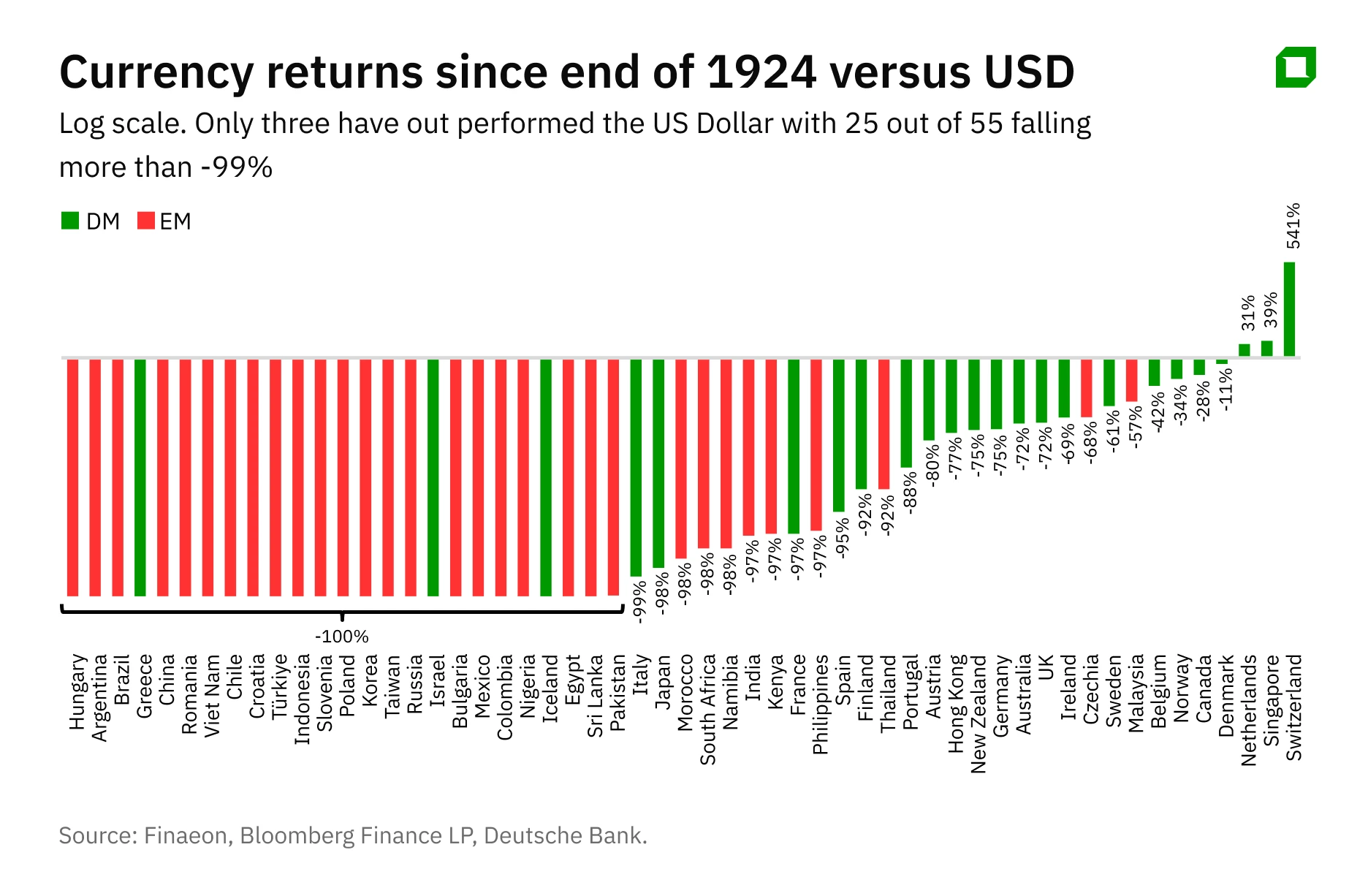

Pitfall #4: Currency—the invisible killer of capital

Growth in your portfolio is beneficial. However, what if the currency in which your portfolio is denominated declines? The same Deutsche Bank study clearly demonstrates how the past century became a graveyard for national currency ambitions. Of the 55 currencies analyzed, only three—the Swiss franc, the Singapore dollar, and the Dutch guilder/euro—appreciated against the US dollar. At the same time, 25 of the 55 currencies depreciated by more than 99%. This is a key argument in favor of global diversification: local market success in national currency often turns out to be nothing more than a beautiful illusion masking the collapse of purchasing power.

Golden non-standard

As for gold, Deutsche Bank's data for the last 200 years looks like a death sentence: just +0.4% above inflation. But if we look only at the period after 2000, gold shows phenomenal results: 7.45% per annum compared to 5.8% for the S&P 500.

Unfortunately, this is not a reason to rush to turn your portfolio into Fort Knox. Rather, it is a reminder that even "eternal rules" live in cycles. Sometimes defensive assets dominate for decades, especially in the context of inflationary surprises and escalating geopolitical conflicts.

To avoid romanticizing gold, it is useful to keep in mind a study by Irish economists Dirk Baur and Brian Lucy, in which they argue that gold's "protective" properties are usually short-lived, mainly occurring after extreme shocks.

Real estate: returns like stocks

The situation is different with real estate. Another well-known study analyzing the historical dynamics of various assets in 16 developed countries shows that since the late 19th century, housing has yielded real returns comparable to those of stocks—about 7% per year. The secret to this result lies in the structure of returns: price growth for the properties themselves often only slightly outpaces inflation, while the rest is the result of growth in rental income, which historically has a direct correlation with growth in consumer prices and wages. However, this 7% does not take into account taxes, repair costs, and the lower liquidity of real estate compared to stocks.

Go to cache

And a few words about cash. A logical conclusion can be drawn from the Deutsche Bank study that it makes no sense to keep money in a bank account or even at home in a safe. But even this can be viewed from a different angle, because if you are expecting a market correction, cash effectively becomes an option to buy cheap assets in the future, with a fee for this option of 2% per year. If you are prepared to accept such losses in order to wait for a better entry point, then there is no problem.

This article was AI-translated and verified by a human editor