A breakdown of "The Magnificent Seven": what are its weaknesses and strengths

The influence of the Magnificent Seven on major US indices has reached unprecedented levels. As of August 2025, the combined market capitalization of Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia and Tesla is approaching $20 trillion - equivalent to the stock markets of the UK, Canada and Japan combined. Such concentration is a double-edged sword: it provides a powerful boost during rallies, but creates significant systemic risk during downturns. Vadim Merkulov, director of the analytical department at Freedom Finance Global, analyzed whether there is reason for alarm

Pyramid: The Magnificent Seven at the top.

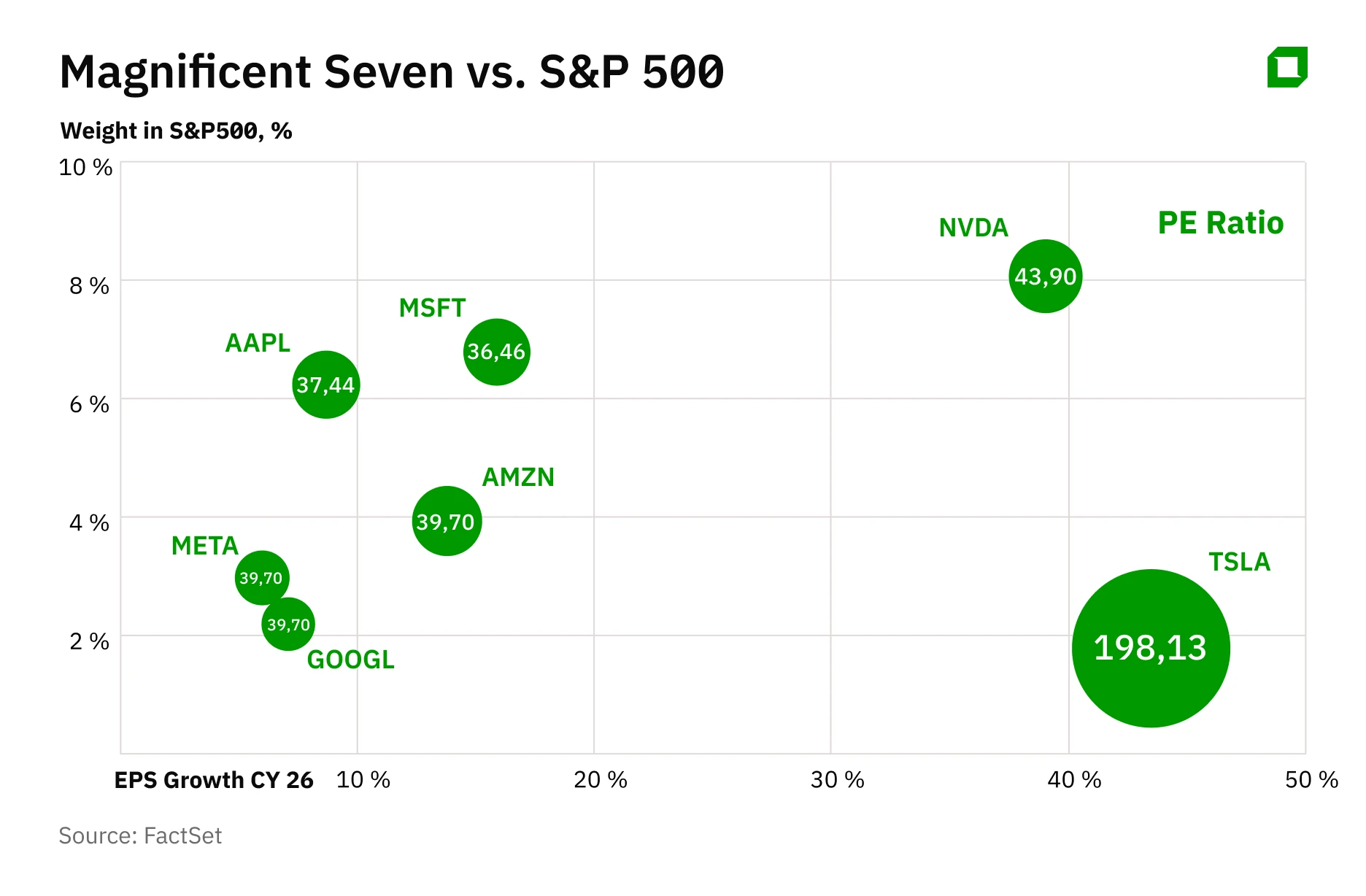

The term "Magnificent Seven" is not yet two years old - it was first used by Bank of America analyst Michael Harnett in 2023. In 2015, seven companies accounted for 12.3% of the S&P 500; in August 2025, they will account for 34%. The concentration is even more pronounced in the Nasdaq 100 technology index, where the "Magnificent Seven" account for about 62% of the index's performance. In fact, the movements of seven companies can have a huge impact on the systematic risk of the entire market and this risk should be on investors' radar.

The group trades at 28 times forecast earnings at a premium of about 20% to the S&P 500. That's within the range: average EPS growth (expected earnings per share growth) from 2026 for the Magnificent Seven is 19% versus 13% for the S&P 500. Within the cohort, valuations differ markedly. Nvidia, Alphabet, Apple, Microsoft, Amazon, Amazon, and Meta have forecast P/Es clustered roughly in the ~20-34× range, which is perfectly normal given revenue and earnings growth. The Magnificent Seven have margins of over 28%, but if you exclude the two outsiders the average rises to 36.5%. The outsiders in terms of margin are Amazon (over 9%) and Tesla (over 7%), which is also natural - selling goods and cars is not the most profitable endeavor. However, in the case of Amazon, this is expected, where 40% of revenue is the low-margin business of selling nearly $250 billion worth of goods, and the company's high-margin cloud business makes up less than 17% of revenue. In Tesla's case, the situation is more complicated: a high projected P/E of about 160 - meaning investors are paying as if they are willing to wait almost more than a hundred and fifty years for Musk's company to earn its share price from earnings . Low margins, slowing revenue amid competition with China signal that the company's entire valuation is built around the company's non-functioning businesses (self-driving taxis/cars and robots).

Musk's company looks much worse against the backdrop of the rest of the Magnificent Seven's great business, so much so that even some investors have started talking about replacing Tesla in the Magnificent Seven lineup with Broadcom, which has no such problems and already overtakes the automaker in terms of weighting in the S&P500 - 2.55% vs. 1.79%. As part of our analysis, we will fixate on the current Magnificent Seven lineup.

AI as a risk factor

If estimates, margins and revenue growth rates are justified, then where is the risk? The risk is in the concentration and forecast revisions themselves. Nvidia's data center products have been the driver of earnings revisions at the index level - when it gives weakness, the market feels it. In the latest quarter, the company reported revenue of $46.7 billion (+56% YoY) and Q3 guidance of $54 billion, the company beat expectations by a wide margin. But in case there is pressure on revenue, the whole story around the premium valuation of the company will disappear and the consequences will be felt not only by the company's investors but also by passive owners of the broad index. The story is similar for the other major companies in the index - their future financial results are highly correlated with the AI factor.

Deploying AI infrastructure is not only a risk, but an opportunity for institutional portfolios. Hyperscalers' budgets for AI infrastructure are growing rapidly:

- Alphabet has raised its 2025 capital expenditure (CapEx) guidance to ~$85 billion

- Microsoft planned more than $30 billion in just one quarter, a record in the company's history

- Meta raised CapEx for 2025 to $66 - 72 billion from $64 - 72 billion

Combined capex of Amazon, Microsoft, Alphabet and Meta is approaching $364bn in 2025 - that's over 20% of total S&P 500 investment vs ~4% adecade ago. The main focus is GPU procurement and data center construction, which creates short-term pressure on margins while monetization remains uncertain; the "tails" of depreciation and free cash flow pressures have the potential to trim long-term profitability if revenue lags - this is the cornerstone of the entire premium of the largest companies. High capital intensity exacerbates the issue of return on invested capital (ROIC). AWS, Microsoft Azure and Google Cloud are showing strong growth in AI segments (>30%). However, all is not so great in the tech industry: an MIT study found that 95% of business attempts to integrate generative AI do not result in tangible impact or P&L outcomes, and only 5% of organizations successfully scale AI tools to real industrial use. This could be a major stopping factor in continuing similar growth rates in AI infrastructure capex.

On the edge: between regulation and growth

Since Trump's election, fighting monopoly enforcement has gone by the wayside, because this administration is pro-business. However, antitrust enforcement is a significant near-term catalyst that the market may be underestimating. The US DOJ's case against Google over its advertising business recorded a victory for the government; the EU has already fined Apple (€500m) and Meta (€200m) under the Digital Markets Act (DMA) and can impose periodic fines - the commission has the power to levy up to 10% of annual turnover for non-compliance). Apple tried to overturn the US DOJ's iPhone monopolization lawsuit but failed, raising the risk of measures on the app store, payments and default settings. The DOJ had two cases against Alphabet for dominance in search and advertising, and potential measures include forced divisions of Chrome (browser) or Android (operating system) assets. On August 2, the U.S. government lost both cases. Microsoft has been under scrutiny from the Federal Trade Commission (FTC) because of cloud service bundling practices reminiscent of the 1990s cases. On regulatory oversight of tech platforms, Democrats and Republicans have complete consensus. New FTC Chairman Andrew Ferguson has explicitly prioritized "holding Big Tech accountable."

The new U.S. tariff measures seem settled, but under Trump, any changes could happen very quickly. And if the new administration's trade policy is too aggressive, businesses of major companies may feel regulatory pressure in these jurisdictions.

Are the Magnificent Seven left with only risks with no potential drivers? Absolutely not, the strength of these companies' earnings and earnings growth is still being felt. According to FactSet, the S&P's elevated forward P/E is largely due to the resilience of earnings expectations. If AI does lift margins and improve the revenue mix - Copilot, AI search/advertising, generative advertising, recommendation systems, multiples to persist at current levels.

Alphabet, Microsoft, Meta and Amazon promise another year of record capex in data centers for learning/inference, supporting upstream vendors (GPUs, networks, power) and giving a base for downstream monetization in advertising, cloud AI and enterprise productivity. Despite the volatile outlook, the investment pipeline remains strong through at least 2026.

Drivers such as AI-PC upgrades (i.e., the end of Windows 10 support) and AI-assisted devices are shaping a multi-year replacement wave that benefits the Microsoft and Apple ecosystems. HP has noted steady demand for AI-PCs, IDC expects a resumption of shipment growth in 2025.

Hedge the tails

For the Magnificent Seven portfolios, this is a complex, risk/return ratio that requires nuanced work rather than binary allocation decisions:

Consider the benchmark. When one-third of the capitalization is concentrated in seven names, a neutral position in the index becomes a big bet. Investors should limit the proportion of individual securities and consider equally weighted funds. Concentration is already failing: February 2025 saw the first outflows from U.S. equity ETFs in nearly two years

Keep drivers, hedge tails (unlikely risks). By keeping a large exposure the investor can diversify through indirect allocation - assets closely related to AI, e.g. computing, networks, utilities/energy companies. For hedging, put options can be used periodically for downside protection.

Track key metrics (ARPU growth, ad revenue, cloud gross margin) along with capex rate. Management comments and updated benchmarks indicate continued spending and the need to show revenue per watt and dollar.

It is best to look at the Magnificent Seven companies separately rather than as a single basket. For example, Alphabet is interesting due to its relatively low valuation and diverse sources of income, which makes it more balanced in terms of risk and return. Microsoft and Apple are more expensive than the market, so it makes sense to hold their stocks selectively - only where there are clear growth drivers. Meta benefits from the introduction of AI in advertising technology and effectively controls costs, which allows it to remain attractive despite regulatory pressure. Nvidia, on the other hand, needs to be assessed particularly cautiously: its results are highly dependent on its desire to continue to ramp up investment in AI infrastructure, I don't see medium-term risks to this, but the world is changing very quickly and it will need to be prepared for this. Tesla's fundametal case loses badly to the rest of the Seven companies - the main valuation is centered on future expectations without any confirmation of facts in the present (the first unmanned cab tests don't count). If there is faith in Elon Musk, it is worth considering another miracle from this entrepreneur.

This article was AI-translated and verified by a human editor