Ex-U.S. small-cap ETFs continue to outperform U.S. peers in 3Q, but comeback in sight

Investors continued to favor European and Asian small-cap stocks in the third quarter. International ETFs, which had been leading since the start of the year, maintained their advantage, while U.S. small-cap funds – previously lagging – regained momentum.

The Russell 2000 index, which tracks U.S. small- and mid-cap stocks, rose 12.4% for the quarter, outperforming the large-cap-tracking Russell 1000, which gained 8.0%.

Oninvest analyst Aldiyar Anuarbekov looks at which small-cap ETFs and which sectors performed best in the third quarter.

International small-cap ETFs lead

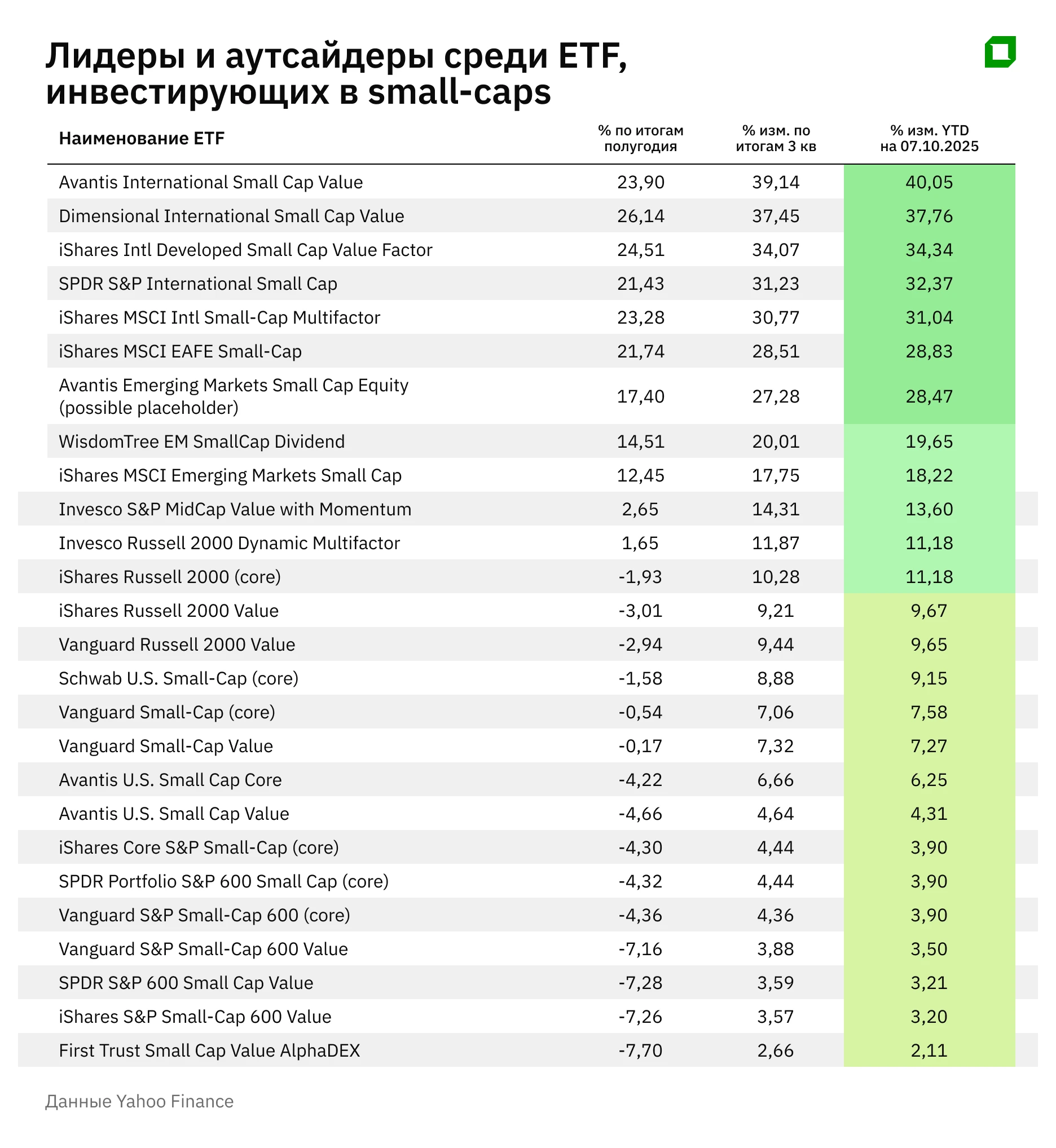

Funds investing in undervalued small-cap stocks in developed markets excluding the U.S. remained among the top performers. The Dimensional International Small Cap Value ETF (DISV) gained 37.5%, and the Avantis Emerging Markets Small Cap Equity ETF (AVEE) climbed about 40%.

A weaker dollar since midyear lifted returns on international assets in U.S. currency terms. In addition, foreign small caps were insulated from the wave of pessimism that swept the U.S. market earlier in the year.

The MSCI ACWI ex USA Small Cap Index – which captures small-cap stocks across 46 developed and emerging markets – advanced 26% in the third quarter. The gains were led by Japan, the UK, and India, where cyclical and industrial sectors benefited from both lower funding costs and rising commodity prices.

International ETFs focused on traditional value sectors such as industrials, financials, energy, and materials also profited from the continuing commodity upcycle. Gold prices surged nearly 43% year to date, reaching a record high, which has supported the shares of miners, both large and small – one of the main drivers of small-cap fund performance in non-U.S. markets.

Specialized international strategies focused on value also stood out, delivering unexpectedly high returns. The Dimensional International ETF and iShares International Developed Small Cap Value Factor ETF (ISVL) rose 38% and 34%, respectively, while Avantis International Small Cap Value (AVDV) led with gains approaching 40% in the third quarter.

Within the non-U.S. segment, performance varied sharply by region. Funds investing in developed markets – including DISV, ISVL, and AVDV – outperformed those focused on emerging markets. The Avantis Emerging ETF, for example, gained about 28% in the third quarter, a strong result yet below its developed-market peers.

The difference stems from index composition: India (20.3%), Taiwan (24.3%), South Korea (12.6%), and China (12.1%) account for more than two thirds of the fund’s benchmark. Its sector exposure is heavily skewed toward technology and industrials, which benefited less from the commodity and defense cycles that fueled ex-U.S. developed-market rallies.

Overall, international small caps have been key beneficiaries of the global rate-cutting cycle. Their cyclical business models positioned them to gain as the world economy reaccelerated and commodity prices climbed.

U.S. small-cap ETFs staging a comeback

U.S. small-cap companies also staged a comeback in the third quarter. While foreign ETFs had been rising steadily throughout the year, U.S. small-cap funds lagged until early summer. By July, many remained in the red for the year – particularly value strategies. The iShares Russell 2000 Value ETF (IWN) was down about 3% in the first half of the year, while the broader iShares Russell 2000 ETF (IWM) was off 2%.

Investors feared that tighter-than-expected Fed policy and the threat of recession would hit smaller companies with limited liquidity. By autumn, however, sentiment had shifted. At its September meeting, the Fed cut rates for the first time since 2024, delivering a reduction of 25 basis points to mark the start of a new easing cycle.

Markets began pricing in that move months in advance. Small caps, traditionally most sensitive to borrowing costs, started to recover even before the official decision. By the time the Fed announced the cut, the rally was well underway. The next day, the Russell 2000 reached a new all-time high, refreshing the previous one set 967 trading days before. Only once previously, in 2004, had the index gone so long without setting a new high, underscoring the scale of the prior underperformance and the significance of the current reversal.

During the third quarter, all 11 small-cap sectors posted gains, with cyclical industries outperforming defense. The resilience of the U.S. economy played a central role: consumer spending remained solid, and the labor market, while cooling, looked to be in good shape.

An additional tailwind was improved access to capital. Lower rates immediately eased debt burdens for Russell 2000 constituents, many of which rely on floating-rate loans. Operating margins and growth outlooks improved, prompting investors to take another look at their positions across the segment.

Outlook

Analysts at JPMorgan expect that Fed easing will remain a crucial tailwind but not the only one. The bank notes that small and mid-sized companies are already outperforming thanks to stronger fundamentals, including a higher share of profitable firms and still-attractive relative valuations.

JPMorgan forecasts that small and mid-caps in developed markets could outperform large-cap peers by 30-60% over the next three years, meaning the current cycle may be only in its early stages.

The AI translation of this story was reviewed by a human editor.