Foreign, cheap, cyclical: Which small-cap ETFs led gains in 2025?

In 2025, while U.S. tech megacaps continued to push to new highs, exchange-traded funds focused on small caps – particularly outside of the U.S. – delivered standout returns. According to BofA, global equities outperformed U.S. peers by more than 15 percentage points – the widest gap in 30 years. Much of that outperformance came from ETFs tracking small caps outside of the U.S.

The move reflected a rare alignment of macro drivers. A global pivot in monetary policy coincided with the early stages of a new commodity cycle. The Fed shifted to easing, while the dollar weakened sharply. In the first half of 2025, the dollar index posted its steepest decline in nearly four decades. The lower borrowing costs and weaker dollar created favorable conditions for risk-taking, prompting investors to rotate into undervalued foreign markets, particularly small caps.

Rising demand for raw materials and energy added momentum. After the pandemic-driven downturn, resource exporters and related industries – traditional pillars of value investing – began to recover. At the same time, the global economy proved more resilient than expected, and central banks in countries from Latin America to Asia cut rates, supporting business activity.

Leading small-cap ETFs in 2025

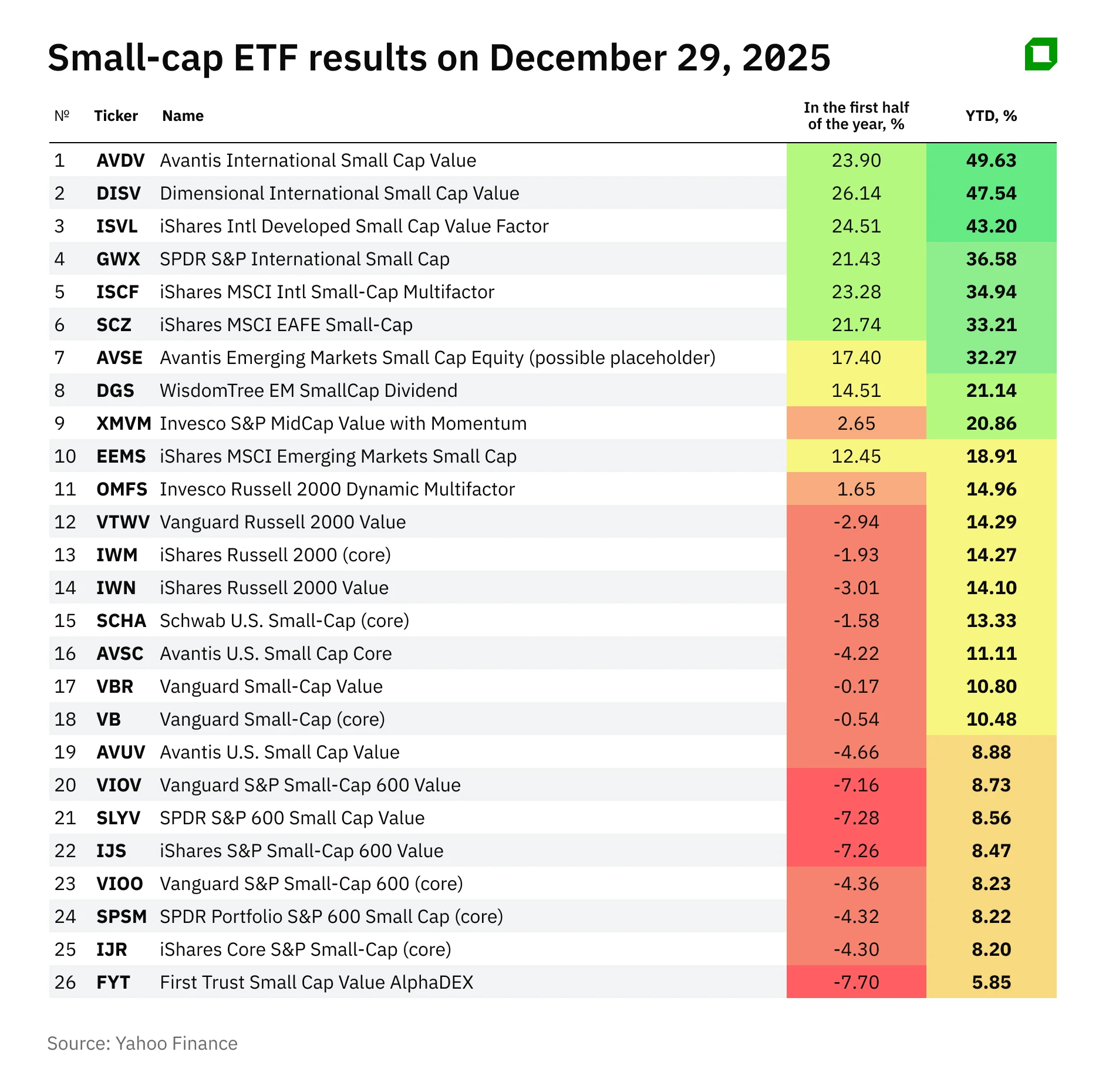

International small-cap value ETFs led performance. The Avantis International Small Cap Value ETF (AVDV) returned about 50% for the year, the Dimensional International Small Cap Value ETF (DISV) 48%, and the iShares International Developed Small Cap Value ETF (ISVL) 43%. All three focus on markets outside of the U.S. and have value-based strategies, targeting companies trading at depressed valuations in traditional industries.

AVDV relies on fundamental analysis, selecting companies with stable profits and low valuation multiples based on free cash flow, revenue trends, expenses, and price-to-book ratios. DISV uses a systematic framework to identify undervalued small caps globally. ISVL tracks an index designed to capture value-oriented segments in developed markets.

Sector allocations across the funds are broadly similar. Industrial and financial stocks dominate, alongside meaningful exposure to raw materials. DISV allocates about 21% to materials, roughly 19% to financials, and about 18% to industrials, while IT accounts for just over 4%. AVDV shows a comparable profile, with financials and industry together accounting for about 40% of assets, supplemented by health care and consumer cyclical stocks. ISVL is likewise concentrated in industry and finance, which together account for more than 45% of the portfolio.

This structure is typical of value strategies in the small-cap universe. Cyclical and capital-intensive industries tend to offer a higher concentration of companies with stable operating profits and attractive multiples. Unlike the U.S. market, exposure to tech and communications is limited, giving these funds a materially different profile. That positioning allowed them to benefit from the global value recovery.

Ex-U.S. rally in 2025

The rally was not limited to explicitly value strategies. The broader international small-cap universe also posted strong gains. The SPDR S&P International Small Cap ETF (GWX) rose about 37%, while iShares ETFs covering developed-market small caps more broadly – ISCF and SCZ – gained 35% and 33%, respectively.

These funds track diversified indexes spanning a wide range of sectors, from European manufacturers to Asian service companies. While their strategies resemble classic index exposure rather than targeted sector bets, they benefited from the broad recovery in foreign equity markets.

Value-oriented strategies nevertheless stood out, delivering an additional premium due to their sector mix. In practice, they offered a more concentrated way to participate in the global small-cap rally.

What unites the leading funds is geography and approach. All focus on developed markets outside of the U.S., including Europe, the UK, Japan, and Australia. BofA analysts note that international value stocks have generated positive returns for several years, a trend that became particularly visible in 2025. Undervalued small companies in developed markets matched the returns of U.S. tech leaders, while showing lower volatility and far more modest valuations. BofA Global Research has included global small-cap value stocks among its key investment ideas for the year.

Sector exposure played a decisive role. Manufacturing, finance, extractive industries, and broader industrials dominate these portfolios – classic real economy sectors. Minimal exposure to tech stocks worked in their favor as cyclical industries led gains amid recovering global demand and accelerating infrastructure investment. Dollar weakness provided an additional tailwind, lifting returns for funds exposed to the euro, yen, pound, and the Australian dollar.

Interest rates were another key factor. Small companies are particularly sensitive to financing costs, and the sharp decline in yields toward year end eased funding conditions. In the fourth quarter, the Russell 2000 outperformed the S&P 500 for four consecutive weeks for the first time in two years. While investors favored megacaps for much of 2025, the year ended with a clear resurgence of interest in small caps. The common thread among the year’s leaders was consistent: foreign, cheap, and cyclical.

Outlook for 2026

The outlook for 2026 remains broadly constructive. In a November report, BofA described the global backdrop as friendly. Markets are pricing in three Fed rate cuts under a new chair, the dollar continues to weaken, and most major central banks have shifted toward easing.

BofA advises investors not to abandon geographic diversification, with a focus on international value stocks. Related ideas include high-dividend emerging-market equities, with yields above 4%, and EM sovereign bonds, which typically benefit from falling rates.

Expectations for small caps are also improving. In the U.S., the segment has begun to recover after years in the shadow of megacaps. BofA forecasts that small-company profits will grow by 17% in 2026, versus about 14% for large-cap stocks. Drivers include margin improvement, a more favorable trade backdrop following partial tariff reductions, and capital rotation out of overheated megacaps into undervalued assets.

JPMorgan is even more upbeat: the bank’s strategists argue that 2026 could be the year of small- and mid-cap stocks and recommend increasing exposure, particularly in the U.S., where upside is seen as especially compelling.

In Latin America, meanwhile, the rally may continue amid accommodative monetary policy and accelerating nearshoring trends. In Japan, momentum is being driven by record returns on equity and corporate reforms encouraging companies to share profits more actively with shareholders. Even in Europe, where economic growth expectations remain subdued, low valuations and a focus on domestic demand provide a degree of downside protection – particularly if the region manages to avoid a deep recession.

Risks remain. Part of the 2025 rally was driven by expectations that have yet to materialize. Industrial manufacturing has not fully recovered: the ISM manufacturing PMI continues to indicate declining activity, and small industrial stocks are effectively pricing in a rebound that has not yet arrived. If manufacturing fails to revive in 2026, momentum in small caps could fade.

Monetary policy remains a key variable. Further rate cuts would be supportive, but renewed inflation pressures or financial shocks could tighten lending conditions. Geopolitics also remains a risk. Trade disputes, sanctions, and new conflicts tend to hit small companies harder, given their sensitivity to costs and supply-chain disruptions.

This material does not constitute individualized investment advice.