From romanticism to pragmatism: how to become an investor in space companies

Only 10 years ago, talk of the space economy seemed to be the domain of futurists and science fiction authors. Today, however, this is one of the most dynamic and promising segments of the global market, which has ceased to be the arena of "dreamers" and is increasingly attracting pragmatic investors. Evgeny Shatov, partner of Capital Lab investment company, tells us how to make money on it and what "red flags" should be avoided.

From "space romanticism" to financial statements

According to the Space Foundation, the global space economy will reach $613 billion in 2024. Forecasts for the sector look ambitious: McKinsey expects it to grow to $1.8 trillion by 2035, growing at about 9% per year for the next 10 years. That's faster than the average global GDP growth rate. Even more conservative scenarios suggest that the space services market will grow to at least $800 billion by 2034.

The space industry in 2025 has moved far away from its former "space romanticism" and is now a rapidly maturing sector of the economy where success is measured mainly by lines in financial reports.

What is driving the space industry upward? Development of reusable rockets (this is something Elon Musk is actively engaged in, for example), miniaturization of satellites.

Other drivers include new Direct-to-Device communication formats, where a satellite signal is fed directly to a smartphone, and rising defense budgets. Space government budgets, including those of the US, EU, China and India, are expected to grow by 15% in 2024. Finally, the last factor on the list is commercial orbital development. More than 70% of the space industry's revenues are already generated by satellite services such as the Internet, IoT, navigation and geodata.

Private capital has shunned space projects over the past four years, but is now gradually returning to this market. Investments from funds in the sector have collapsed three times since 2021 - from $18 billion to $5.9 billion in 2024.

Four years ago, a venture capital bubble inflated in the market thanks to the era of ultra-cheap money: low interest rates, excess liquidity and a high willingness of funds to take risks led to massive investments in startups in the space, biotech and fintech sectors with distant investment horizons.

The companies themselves were going public at the same time with the SPAC merger - they had dizzying plans for space tourism, asteroid mining and private orbital station construction, but no revenue. After a string of failures and falling stock prices, SPAC projects became synonymous with opacity and overvaluation. This undermined investor confidence.

Everything ended in 2022: against the backdrop of a sharp increase in Fed rates and the crisis in the market of technology stocks, investors switched to fast-paying projects, and large funds actually took a wait-and-see attitude. The space industry, where payback periods are calculated in decades, was among the first victims.

A signal of revival now is the cautious resuscitation of the IPO market for space projects. Mature companies with a proven business model, stable revenue and contracts with NASA or defense agencies are coming to the stock exchange.

The success of Voyager Technologies, whose shares closed on the first day of trading on June 11 this year at more than 80% above the IPO price, showed that investors are willing to pay for reliability and predictability. As is often the case, the company's shares have fallen in price since going public, but now they are worth about the same as at the IPO. Also in February this year, Karman Holdings went public (traded at more than twice the IPO price), and in August - Firefly Aerospace (its quotations are now at about the level of the public offering).

While in 2020-2021 the capital of large funds massively flowed into "distant dream" projects, today their priority has shifted to companies with projects that have commercial applications - in satellite communications, navigation, geo-analytics and integration with AI.

Major investment funds, including Fidelity, BlackRock and Vanguard, maintain space investments in their portfolios at 2-4% of their combined portfolios, indicating their cautious optimism about the sector.

Metrics that can't be ignored

Analyzing investments in space should be approached with caution.

There are more and more breakthrough technologies in the sector, and they reach the stage of commercial applicability faster. This is a key point for investors: the space market is no longer living at the stage of "experiments", but is increasingly demonstrating practical returns - the cost of projects is decreasing, while revenues and scalability are growing. State support and steadily growing demand for orbital data, satellite communications and Earth observation services also serve as a significant advantage.

At the same time, the industry requires huge investments, and therefore companies in it often operate with a high debt load and long payback periods.

In addition, the number of satellites in orbit is growing. The number of vehicles in orbit has increased 3.4 times in four years, while the industry's revenues in 2024 grew by only 4%. That is, this sector is gradually becoming saturated.

Another problem is supply chain disruptions. Many components for space projects are produced by a limited number of suppliers. This creates a bottle-neck effect: demand for launches, satellites and infrastructure is growing faster than the capacity to produce rockets, solar panels or attitude control systems. In addition, spacecraft require radiation-resistant microchips. Their production is concentrated in a few companies in the US, Japan and Taiwan.

When selecting projects, investors should first of all pay attention to the Technology Readiness Level (TRL) of the company. This is a system for assessing the level of technology maturity at various stages of development, from idea to mass production. As a rule, TRL is rated on a scale of 1 to 9 points. For mature players, it should be at the level of 8-9 points, which corresponds to the presence of serial samples and successful tests.

But this is no guarantee of success. In the spring of 2023, Richard Branson's satellite launch company Virgin Orbit announced a shutdown and filed for bankruptcy. Its TRL was 8, but the model of launching satellites from an airplane proved too expensive; in addition, the company had poor financial discipline and management problems.

The financial stability of the company is also critically important, which depends to a large extent on the presence of an "anchor" customer (be it a government or a corporation). Also important for investors is the factor of a successful market niche. The Direct-to-Device segment, which may reach $6.5 billion a year by 2027, is a good example. Elon Musk's Starlink has already started working in this niche, together with T-Mobile.

Finally, we should not discount the methods of comparative valuation of companies, which are classic for corporate finance.

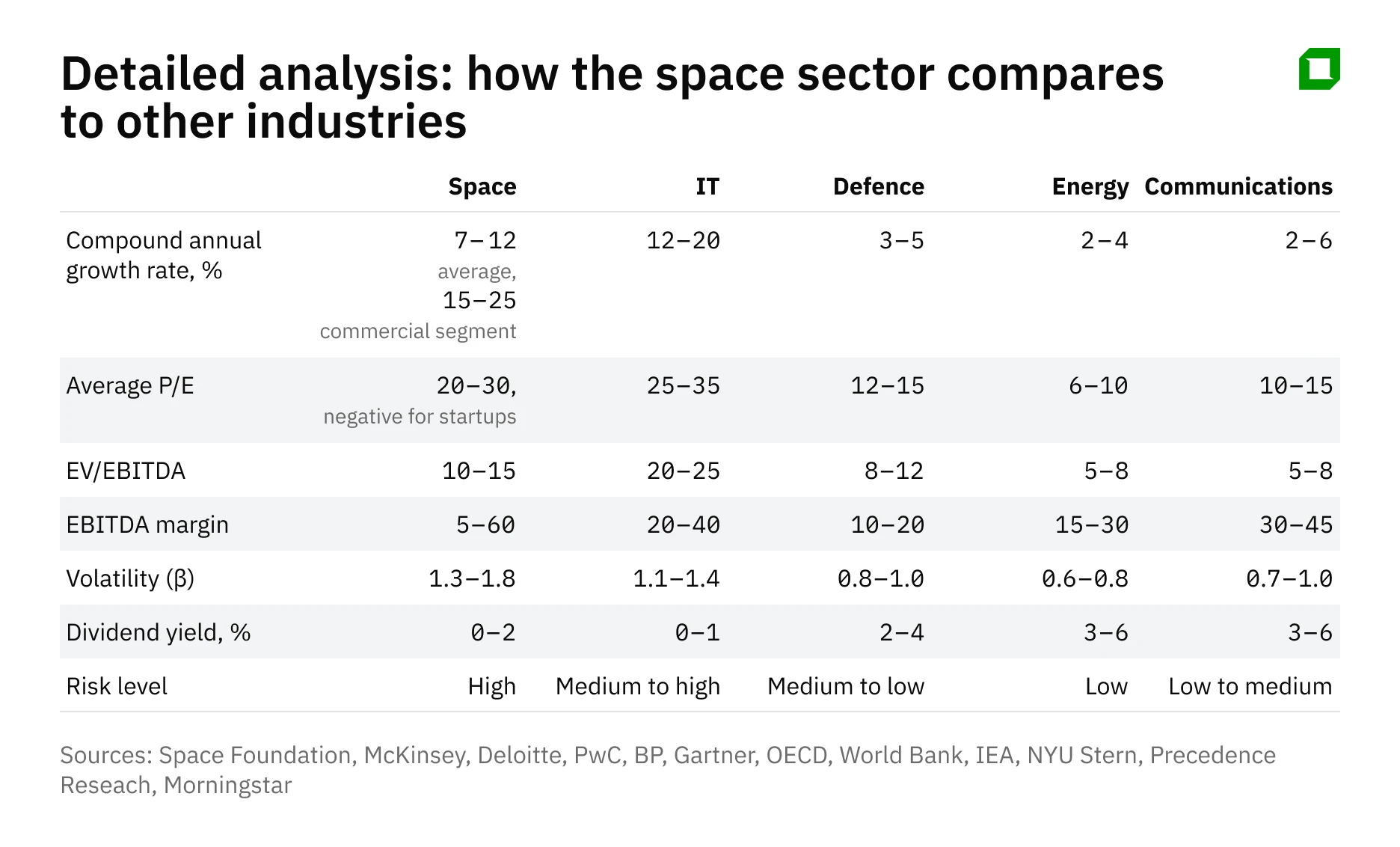

Among traditional multiples, P/E (price to earnings ratio) is the best for the space industry - it is an indicator of company maturity, which is often absent for startups, but close to 20-30 for large contractors in the space sector.

Another is EV/EBITDA, which averages 10-15 for space companies. If it is above 30, it means that investors are ready to pay for the company ten times more than its current operating cash flow. This is a signal of heightened market expectations and significant risks, and a reason to ask questions: how realistic are revenue forecasts, is there diversification of the customer base, and will the company not be "hostage" to one technology or one major customer. The P/S (price to revenue) ratio in the space sector should not exceed 15 with negative EBITDA.

"Red flags" for the investor

The main red flag for an investor is the lack of prospects for commercialization of the business in the near term: usually we are talking about utopian projects related to asteroid mining or lunar tourism, which often remain concepts without clear payback periods. The general recommendation is to stay away from overvalued companies with no operating base (P/S greater than 15) and negative EBITDA with no certified technology or unfulfilled launch schedule.

In addition, investors should avoid companies that depend on a single client, especially if it is a government customer that can change the project budget at any time. Yes, at the early (venture) stages, space projects may have one customer - a government agency, but mature companies usually have dozens of them. For example, Rocket Lab has a portfolio of contracts distributed among NASA, ESA, private telecommunications firms and research institutes.

The statistics are ruthless: 70% of space failures are due to lack of funding for research and development, and the rest are due to technical failures. This data illustrates the paradox of the space industry: the main reason for failure here is not that the technology doesn't work, but that the money runs out before the technology can pay for itself. This is why government contracts, grants and access to long-term funding are fundamental to the survival of space companies.

Finally, companies that ignore sustainability should not be invested in, as the lack of a space debris strategy and non-compliance with the Space Sustainability Rating increases regulatory risks. The main threat here is loss of market access and funding sources, as well as increased insurance and operational costs. For an investor, the lack of a space debris strategy is an indicator that a company may lose key licenses or contracts and its business model may be at risk.

Where to look for space companies?

Although the sector is high-risk, there are a number of low-risk public companies in the sector.

These include satellite manufacturers, including Iridium Communications and Lockheed Martin, and space infrastructure manufacturers, such as Rocket Lab.

In addition, interesting investment ideas in the industry include AST SpaceMobile, Intuitive Machines, Firefly Aerospace, Virgin Galactic, Redwire, Planet Labs, Voyager Technologies and Joby Aviation.

More cautious investors can choose space-focused ETFs. These include the Procure Space ETF (UFO), as well as ARKX and XAR, which are more diversified funds covering the defense and technology sectors in addition to aerospace.

It is reasonable for an investor to limit the share of investments in the segment to a reasonable 5% of the total portfolio volume. After all, in space, as in the market, the winner is not the one who took off first, but the one who managed to get into orbit reliably.

This article was AI-translated and verified by a human editor