Hedge funds are not running for cover: how they are preparing for the start of the business season

The S&P 500 index has been trading near its highs for almost two months now, with risks and uncertainty in the markets growing. But the top 50 American hedge funds are not running for cover. Igor Klyushnev, co-founder of Freedom Holding, analyzed their portfolios - what is worth paying attention to now and what trends we can expect when the active business season starts in September.

Changes in portfolio

The latest BofA survey found that most fund managers believe U.S. stocks are overvalued - 91%, the highest share ever observed since 2001, Bloomberg reported. The survey was conducted from July 31 to Aug. 7, and 169 funds with $413 billion in assets under management participated.

That said, paradoxically, nearly half of participants - 45% - are betting on growth in the shares of the "Magnificent Seven" - the biggest US tech giants Apple, Microsoft, Alphabet, Amazon, Meta, Tesla and Nvidia.

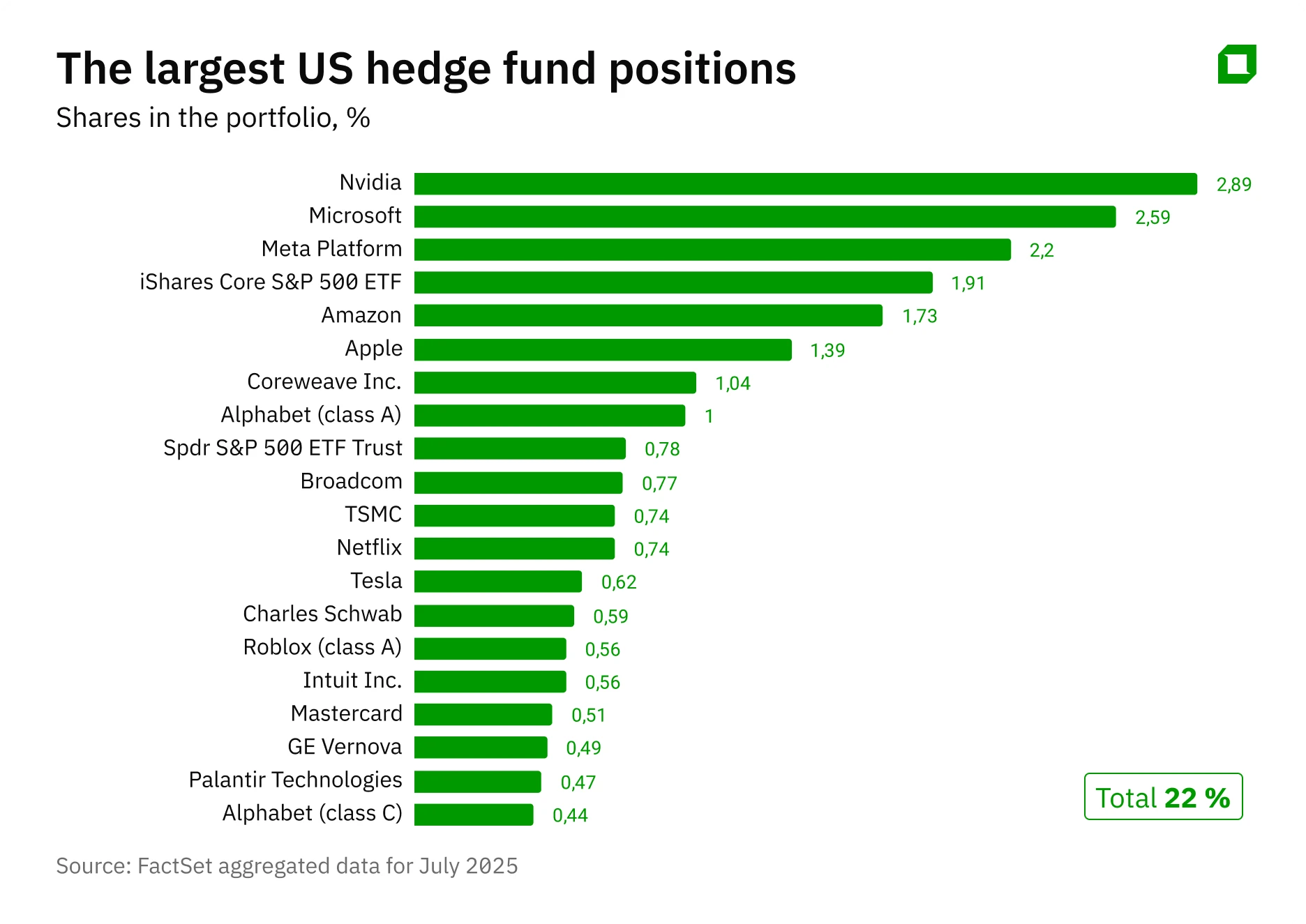

Fresh data from FactSet in July confirms it: the top 50 U.S. hedge funds aren't running for cover or exiting high-growth assets.

For example, 13 of them have the largest position with a weight of about 6% - it is Nvidia. In general, the focus of funds is still on the shares of the "Magnificent Seven". In the top 10 among the most purchased securities are Amazon, Meta, Microsoft, Apple and Amazon. Only Tesla is absent from the top 10, Broadcom securities close the top. Funds reduced positions in Nvidia, Boeing, Robinhood and bitcoin-ETF.

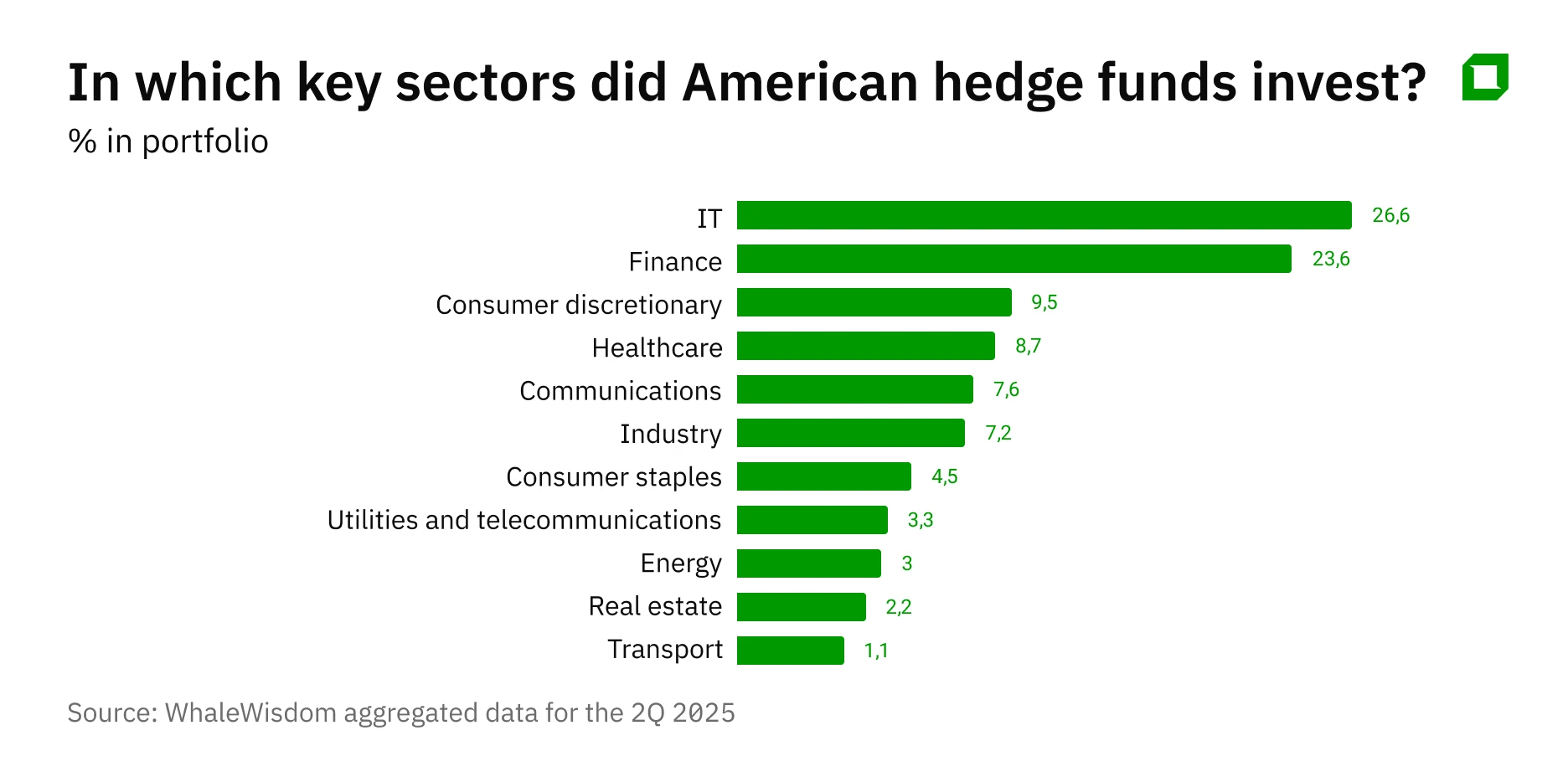

Overall, the aggregate statistics for Q2 2025 showed that U.S. hedge funds continued to shift their focus toward pro-cyclical sectors - they grow with the economy and do particularly well during upturns.

The share of financial stocks in portfolios rose to nearly 24% in the second quarter, up more than 1.5% from the previous quarter. And this is now, according to WhaleWisdom, the second most popular sector for hedge funds. At the same time positions in IT increased (up 2.4% to 26.6%), it is still in first place. At the same time, hedge funds sold securities of companies from the sectors of durable goods, healthcare and consumer staples.

The growth of the share of shares of financial companies in investment portfolios is understandable: the market lays down a positive scenario on deregulation of banks, revival in the lending market and normalization of the cost of risk. In IT there is a partial profit taking, but due to the growth of capitalization we see growth in the largest technology companies within the fund's portfolios.

What to expect in the near future

August has a bad reputation in financial markets and is traditionally characterized by increased volatility: over the past 10 years, the VIX fear index has averaged 18% growth in this month, with a median gain of about 6%. This year this is superimposed on a general background of uncertainty, so market fluctuations through the end of summer are very likely.

High valuations also contribute to increased volatility: the S&P 500 index trades at a forward P/E multiple of 22, which is noticeably higher than the five- and 10-year averages (20 and 19, respectively). The overbought market makes it vulnerable to any external negative - from deterioration of macroeconomic indicators to new geopolitical risks.

In this state, the market will approach September, the beginning of the business season. And in this environment, it is highly likely that funds will decide that it is strategically justified to bet on stable companies with high capitalization and premium quality, and market corrections should be used to form or average positions in strong assets - this will provide the best risk/return ratio over the distance.

The position of Freedom Broker analysts remains moderately pro-cyclical. In our model portfolio, the shares of stocks from the IT, communications, finance and healthcare sectors are noticeably higher than the weights of these industries in the S&P 500 index. And we bet on the largest capitalization companies from the top 10 of the index, which is justified in the context of increased uncertainty.

In the financial sector, we prioritize the largest diversified banks, but growth there is limited.

We see that investors have started shifting money from high-growth companies that are not yet profitable to companies that are already making money. This is understandable: the current high valuation of such non-profitable assets is already too high relative to the economic situation, interest rates and risks.

We prioritize companies with strong financial results, high margins and reasonable multiples: the "quality" factor is now the optimal combination of risk and return. We believe that we should limit the portfolio's exposure to energy, consumer staples and heavy industrial stocks, as they are sensitive to potential tariff risks. It makes sense to move out of the consumer staples sector into online retail stocks. A cautious approach should also be maintained when investing in heavy engineering, transportation and airline companies, as they are too dependent on the economic environment and may be affected by duties.

What to pick from the Magnificent Seven.

Of Freedom Broker's current investment ideas, I recommend paying attention to the following:

- Nvidia

The company reported strong results for the first quarter of fiscal 2026 in May of this year, beating market expectations for revenue and earnings. Revenue growth - up 69% year-over-year - was driven by the ongoing AI boom, a record pace of new Blackwell architecture-based solutions, and strong sales in the consumer graphics card segment. Separately, strong results in the networking equipment segment, which had been a concern in the previous quarter, were also noteworthy.

US restrictions on AI chip exports to China put significant pressure on revenues, but despite this, margins remained strong. Against the backdrop of US trade restrictions, Nvidia's outlook for Q2 2026 was slightly more conservative on revenue, but slightly better on profit.

Freedom Broker analysts raised their target price on Nvidia stock from $165 to $170 following the report. That's below current levels (trading closed at $180.45 on August 15), but I would continue to hold the stock in my portfolio. I wrote about the company's long-term prospects in June, and those points are still valid.

- Meta Platforms

The company's reporting for the second quarter of 2025(ended July 30) exceeded even optimistic market expectations on key metrics - revenue and EPS. The company reported strong growth in revenue (plus 22%), net income (up 36%) and EPS (plus 38%), driven by a recovery in ad pricing, increased user engagement and large-scale adoption of AI tools.

Operating margin increased from 38% to 43%, driven by revenue growth and cost control. Management raised its revenue guidance for the third quarter of 2025, as well as its full-year 2025 spending expectations, reaffirming its strategic focus on the development of its own AI infrastructure.

These investments are expected to lead to accelerated revenue growth in 2026, but will be accompanied by higher depreciation, amortization and compensation costs, which will constrain profitability growth. Another driver of future revenue growth should be the launch of the first advertising formats within WhatsApp.

Freedom Broker analysts raised Meta's target price from $680 to $800, which is about 1.9% higher than the closing price on August 15. At the same time, Freedom Broker downgraded the recommendation from "buy" to "hold"; nevertheless, the upside potential from the current levels remains.

- Alphabet

Google's parent company in late July also reported a better-than-Wall Street expectations for the second quarter of 2025, thanks to performance gains in search, YouTube and accelerating growth in the cloud segment.

Strong adoption of AI solutions in the company's products, including Gemini and Vertex AI, made a significant contribution. Profitability remained solid despite increased investment in infrastructure and hiring. Management raised its forecast for capital expenditure on data center development, confirming continued strong demand for cloud capacity.

Freedom Broker analysts maintained a "buy" recommendation on Alphabet shares and raised their target price from $210 to $225, up about 10% from the Aug. 15 level.

What to buy outside of the Magnificent Seven.

KKR & Co. - one of the world's leading investment companies, which aims to operate like a mini-Berkshire Hathaway, focusing on Warren Buffett's approach. The similarities aren't just in betting on undervalued companies. KKR, like Berkshire, invests heavily in private equity assets. The company buys them "literally forever" and aims to build a portfolio that will pay $1 billion in dividends. Unlike most investment companies that invest with borrowed money, KKR uses its own balance sheet, including insurance assets, as a sustainable source of capital, which is very similar to Berkshire Hathaway's model.

The most powerful catalyst for the company was U.S. President Donald Trump's August 7, 2025 executive order to "democratize access to alternative assets." This is the same document that actually allows pension money to be invested in cryptocurrency and private assets.

This gives KKR potential access to a market of more than $12 trillion, which could become a long-term driver of significant capital inflows into the company's funds and fundamentally change the structure of its assets under management.

Pension funds are unlikely to invest more than a fraction of a percent in cryptocurrency, because the industry is not yet completely white-hot. The main part will go to understandable large businesses that can provide liquidity and digest pension money - these are just large private equity funds. And this is historically the key direction for KKR. Such funds will be competing for investors' money with large venture capital companies, which invest in projects with already established businesses at a late stage.

A "buy" recommendation from Freedom Broker analysts was issued in early August, with a target price of $156 on a two-month horizon. This is 9.6% higher than the price at the close of trading on August 15.

This article was AI-translated and verified by a human editor