How Trump's policies will affect the US economy: three scenarios

In the next four years of Donald Trump's presidency, the U.S. economy will grow between 2.1- 2.2%, Freedom Broker forecasts in its base case scenario. Even the optimistic scenario does not promise a breakthrough for the economy. Vadim Merkulov, head of Freedom Broker's analytical department, explains why.

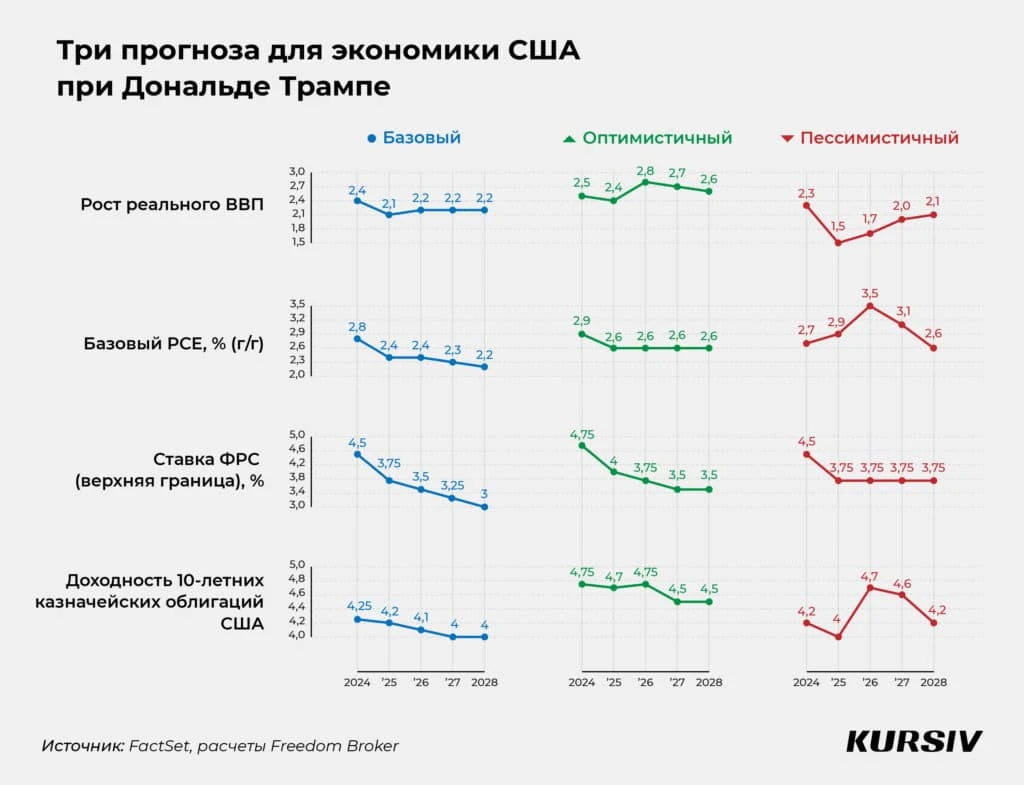

For the US economy, we have created three scenarios: baseline, optimistic and pessimistic. The baseline and pessimistic scenarios assume that the U.S. economy will slow down in the coming year. The difference between the two forecasts is the depth of the decline and the speed of recovery. In the baseline scenario, by the end of 2024, the US GDP will grow by 2.4%, this year the economy will slow to 2.1%, and then, until the end of the new presidential term of Donald Trump, the growth rate will be 2.2% per year. The pessimistic scenario assumes 2.3% growth by the end of 2024, followed by a slowdown to 1.5% and a further recovery to 2.1%. The optimistic scenario assumes a wave-like development - by the end of 2024 the economy will grow by 2.5%, in the coming year the growth rate will slow down to 2.4%, then GDP is expected to grow to 2.8% with further slowdown to 2.6%.

There is now no doubt in anyone's mind that the implementation of most of Trump's initiatives, as they are currently being discussed, could have a noticeable effect on the trajectory of U.S. macro indicators. But there is still a lot of uncertainty about which initiatives will be implemented and in what form.

Even before his election victory, Trump said that if he became US president, he would impose duties of 60% on goods from China and 10-20% on all other imports. He also promised to impose duties of 25% on all goods from Mexico and Canada. Also among his proposals are reducing corporate tax from 21% to 15% and exempting social security payments from the tax. In addition, he proposed to make key provisions of his own 2017 tax reform indefinite, except for the $10,000 deduction for state and local taxes. Some of the reduced tax rates will expire in 2026. Other Trump initiatives, such as ending double taxation of Americans living abroad, closing the Department of Education, and cutting government spending, will have little impact on economic development, in our view.

Three forks

The baseline scenario means gradual implementation of most of Trump's initiatives - both positive and negative for the economy. In the pessimistic scenario, part of Trump's initiatives to cut taxes and expand deductions will be implemented, but together with a full-scale increase in duties, which will have a stronger negative effect on GDP dynamics. The optimistic scenario assumes the implementation of a significant part of Trump's initiatives to cut taxes and expand deductions, but this scenario does not imply a sharp increase in duties.

Under the optimistic scenario, we expect the US authorities to increase import duties slightly, which will have a small negative effect (compared to the main scenario) on the dynamics of the core price index (PCE, excluding food and energy prices). The actual inflation figures will depend to a large extent on how much duties are set. At the same time, there are no conditions in any scenario for a sustained decline in the yield on 10-year US government bonds below the 4% mark.

The acceleration of inflation, if we take into account the optimistic scenario, will probably lead to a more significant growth of the S&P 500 - up to 6943 points at the end of 2025. For comparison, on the last day of 2024, December 31, it closed at 5881.63 points.

Short-term and long-term effects

Overall, the effects of Trump's fiscal and tariff policies can be broken down into two parts: short-term, over the next 1-3 years, and medium-term, looking out over the next 3-7 years.

On the short horizon, the implementation of Trump's proposals will have a predominantly positive effect on the consumer, the economy and the stock market. After all, thanks to the tax cuts, consumer spending and net corporate profits will grow.

In the long run, the effect will be diametrically opposite - because of the increased burden on the budget.

Even the baseline scenario for Trump's initiatives assumes that debt-to-GDP will rise to 144% by 2034, with a pre-2019 ratio of 79%. This would cause the share of interest expense to total budget spending to reach its highest level since 1962 to 20% as early as 2026. That is, one out of every five budget dollars could go to debt service.

This article was AI-translated and verified by a human editor