Make Emerging Markets Great Again: How Trump Launched an Emerging Markets Rally

Wanting to reduce the U.S. trade deficit and U.S. dependence on foreign capital, Trump has delivered big gains for emerging markets

Donald Trump seeks to put America "first", to return it to its former greatness, and to ignore the interests of other countries: let them think of themselves. Trump claimed that his duties would enrich the U.S., while investors feared that the reduction of exports to the U.S. would hit emerging markets. But Trump ended up weakening the dollar and making 2025 a record year for emerging markets. Boris Grozovsky on how Donald Trump's protectionism has made emergency markets great

EM's longest rally in 20 years: capital went after returns

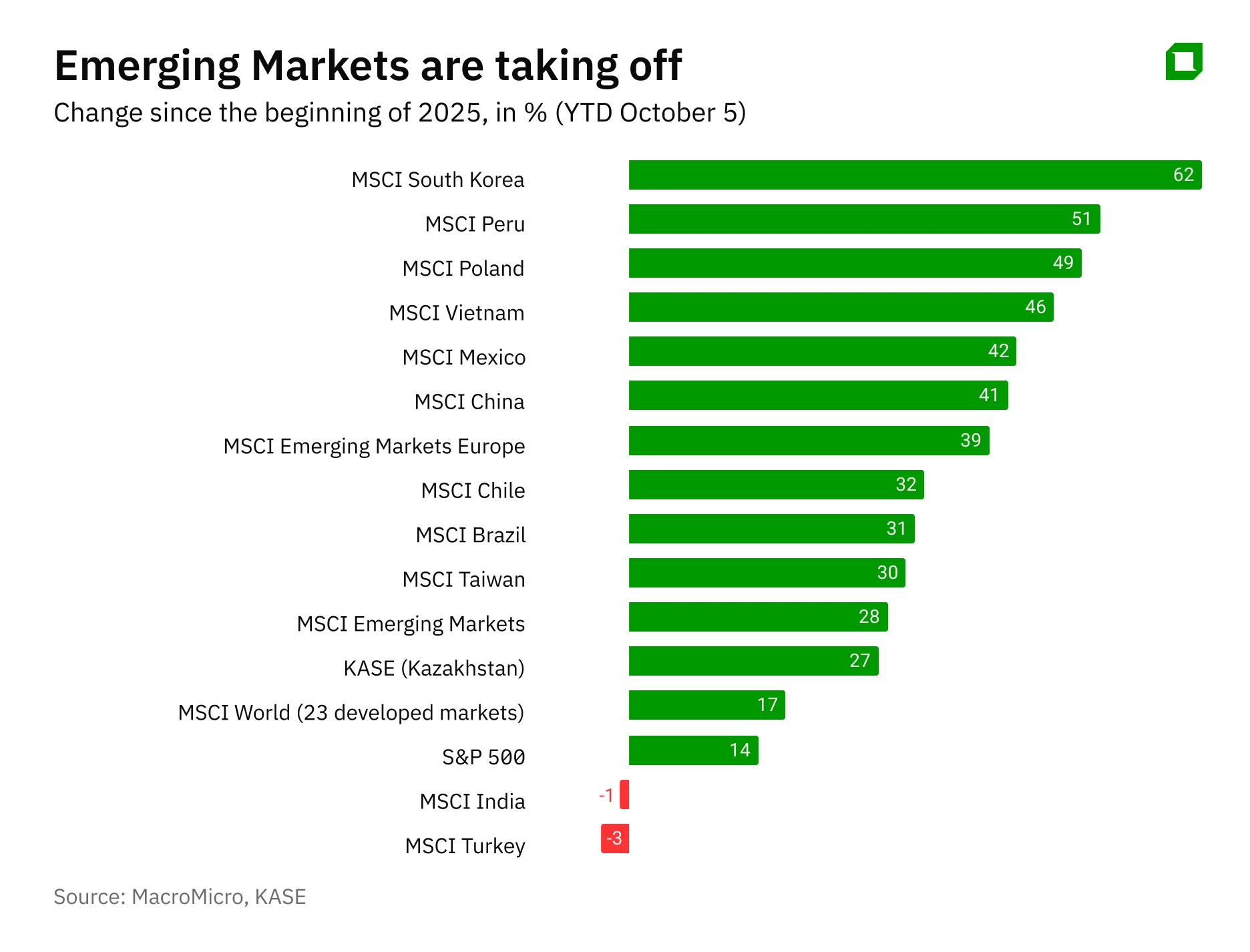

Since the beginning of the year, the yield on emerging market bonds has more than doubled compared to the yield on U.S. bonds (10% vs. 4.5%). The MSCI Emergency Markets index has also grown twice as much as the S&P500 - stocks have added 28% vs. 14% (data as of October 5). The market has not seen such a difference in favor of the Emergency Market (EM) in many years. Trump's policies have helped emerging markets: as I predicted, they have dropped the dollar, boosted emerging market currencies, and encouraged investors to diversify despite the continued rise in the U.S. equity market.

Imagine yourself in the shoes of, say, an investor from Germany, Canada, Denmark or India. Your country's relationship with the US has deteriorated: solidarity within NATO is declining, Canada is being urged to become the 51st state, Denmark is at risk of losing Greenland, India has been hit with duties - the US under Trump is unfriendly to allies. Investors are thinking about reducing the share of U.S. risks in the portfolio. Together with the Fed's key rate cut, this led to a 9.75% depreciation of the dollar against a basket of major trading partners.

EM currencies joined this rally. According to Deutsche Bank estimates cited by the Financial Times, these are the best three quarters since 2010: 12.7% growth against the dollar. Only a few EM currencies fell against the dollar in January-September: Argentine peso - by 25%, Turkish lira - by 15%, rupiahs of India and Indonesia - by 3-4%. The vast majority of EM currencies appreciated against the dollar, including the Chinese, Chilean, Malaysian, Colombian and Brazilian currencies. This increases EM yields for dollar investors and increases the flow of funds into them, states Jean Boivant of Blackrock Investment Institute.

We see opportunities to lock in local currency bond yields in Hungary, Czech Republic, South Africa, Brazil, Ma and Colombia.

There are other pleasant effects as well. In Mexico, the appreciation of the peso helped to bring down inflation, and the National Bank lowered the interest rate from 10% to 7.5%, boosting the economy and stocks. As a result, they are up 42% since the beginning of the year despite the 25% US duties. A similar mechanism works in other countries.

The yuan rose 2.5% against the dollar despite Trump's 50% tariffs against Chinese exports. China's inflation has fallen, the National Bank has lowered its interest rate, and stocks are rising fast. For investors looking to reduce U.S. exposure in their portfolios, Chinese stocks are the No. 1 option, writes CFR expert and Vanguard independent director Rebecca Patterson:

Trump has made emerging markets great again

Chinese stocks rise helped by some de-escalation of Trump tariffs (after escalation). Korean and Taiwanese stocks are rising on the rise of IT - production of chips and AI. Vietnamese, Mexican, Brazilian stocks are helped by successful attempts by local companies to partially replace Chinese companies in global chains. Poland has a growing IT sector. Chile and Peru benefit from demand for metals needed for energy transition.

Emerging markets have been rising for 9 months now, the longest rally in 20 years. Last year the growth rate was three times lower: 8.7%. Asian technology giants are growing especially fast. In Q3, according to JPMorgan's estimates, EM stocks added 11%, while developed-country stocks added 1.5 times less, 7.4%. Among the"champions"of Q3 in terms of profitability are shares of China, Taiwan, Korea, Egypt, Peru, South Africa. JPMorgan warns about the risk of inflation and advises investors to reduce the share of U.S. securities and technology companies.

Enemy, rival, beneficiary: how Trump has made China stronger

China, hit hardest by Trump's duties, has become one of the main beneficiaries, analysts at DWS, which manages funds worth 1 trillion euros, say. China was rescued by a drop in the share of exports to the US to less than 20% of GDP; the EU has 36%. The dependence of developing countries on exports to developed countries over the past 30 years has fallen from 75% to about half - now developing countries account for almost as much as developed countries.

So Trump's duties have affected EM less than they could have. And the influx of funds thanks to a weaker dollar gives EM investment and helps narrow its gap with developed economies. Since 2018, when Trump imposed his first anti-China duties, China's share of global exports has risen from 13% to 18%. A collapse in global trade is not expected: the US market is large, but Trump's duties have only affected 8% of global exports.

Losers

There are also exceptions to the growth of EM equities - for example, India and Turkey. Despite the rapid growth of the economy, the Indian market is slowing down: investors are worried about uncertainty with the trade war started by Trump - against India imposed duties of 50% and 100% on exports of pharmaceutical products. Corporate profits are low; domestic consumption is growing weakly and the rupee-dollar exchange rate has declined for the fifth consecutive month. On top of that, India will be hit hard by Trump's visa fee. Looking at all this, foreign investors are withdrawing funds from the Indian market.

The Turkish economy is also growing nicely in 2025, but stocks are not concerned. Reasons: political unrest - Erdogan's strongest rival was arrested at the beginning of the year, and a volatile lira/dollar exchange rate - Erdogan likes to intervene in monetary policy. In April 2025, interest rates in Turkey were rising as high as 46%. The lira's volatility and frequent devaluations limit the inflow of foreign funds. On a stock price to earnings ratio basis, Turkish stocks are trading at a 45% discount to emerging markets.

Second Breath

Rising yields are driving inflows into equity funds, and they have reached record highs. And after all, fund flows are arguably the main driver of stock prices. "As long as the music is playing, you have to dance," then Citibank CEO Charles Prince said of financial institutions' lending policies in July 2007, on the eve of the financial meltdown. Being out of the market and not making a profit is scarier for financiers than "sitting out" of the market and making a loss.

The EM debt market is still growing slower than developed markets. The global debt market has surpassed a record $337.7 trillion thanks to low interest rates and a weakening dollar - adding $21 trillion in January-June 2025. The size of the debt is about three times higher than global GDP. Global debt growth accelerated in 2025, especially compared to 2022-23, when it was around $300 trillion.

According to the International Institute of Finance (IIF), the debt of the largest borrowers - the USA, China, Germany, France, Great Britain and Japan - has reached a record level. The debt-to-GDP ratio - an indicator of a country's ability to repay its debt - has grown strongly in Canada, China, Saudi Arabia, Poland and Chile. IIF assumes that soon, due to the deterioration of indicators, some investors will start to sell debts of Japan, Germany and France. The debt of developing countries increased by $3.4 trillion to $109 trillion, which is 2.36 times their GDP. The debt-to-GDP ratio of developing countries is lower than that of developed countries, which also contributes to the inflow of investors.

Emerging market equities have room to grow. They account for 41% of global GDP and only 21% of market capitalization. However, GDP growth has little correlation with stock returns. But emerging market returns are highly correlated with the effective dollar exchange rate (with the opposite sign): a rising dollar weakens emerging currencies and pulls money out of their markets. The duties imposed by Trump weakened the dollar and provided EM capital inflows.

Emerging markets have room to grow: the previous 17 years have been bad for them. Invested in early 2008, before the crisis in the S&P 500 index £100 would now turn into £440, and in a basket of EM stocks - would remain the same £100, calculated Tom Stevenson of Fidelity International. After booming in the mid-2000s (up 7 times in 3.5 years), emerging markets have been "going nowhere" for a long time. Trump seems to have succeeded in rocking them. This was impossible in a world where the US operated as the global vacuum cleaner of capital. But now the vacuum cleaner has been put on pause for at least a few years, which has opened up great prospects for emerging markets.

This article was AI-translated and verified by a human editor