Real estate vs. the stock market: what makes people richer?

There is a well-established axiom in the world of personal finance: rent your home and invest the difference in stocks. The authors of many economic bestsellers, including Nobel laureate Robert Shiller, assure that your own home is an asset with high risks and low returns. The famous American economist John Cochrane even called investments in housing for own residence "disastrous".

However, a major new academic study challenges this consensus. Economists from the United States and Hong Kong analyzed data for 16 developed countries from 1870 to 2020 and concluded: abandoning home buying in favor of renting and stocks is a mistake that costs investors capital loss and reduced quality of life.

My home is my investment.

The researchers compared two strategies for the same conditional household over a lifetime. The first - you rent a home for your entire life and invest all of your free cash flow in stocks. The second - you buy a property for your own residence with a mortgage and invest the balance.

The modeling results were unambiguous. Accumulated wealth - life cycle wealth - of homeowners by the end of their lives was on average 9.6% higher than that of tenants-investors. And in terms of growth of wealth - welfare - "homeowners" are ahead by 23% at once.

The study separates the concepts of "Wealth" and "Welfare". Life cycle wealth is an accounting total: how much money and assets a person has left at the end of his/her life. Welfare is the quality of the life cycle. The research model takes into account how stable a person's consumption was during their lifetime, how much risk they took, and whether they were able to build up an inheritance for their descendants. Housing works as a stabilizer: it reduces the maximum drawdowns of the family's aggregate portfolio by 10-13%. For a real person, the absence of sharp drops in living standards is more important than just the maximum amount in the account before death.

How did that happen?

Why does real estate win when stocks have historically shown higher nominal returns?

First, through enforced discipline. A strict schedule of mortgage payments turns the abstract desire to "save" into a mandatory regular action. By paying off the body of the loan, you are actually buying a share in your own asset every month.

Secondly, extremely favorable leverage compared to the stock exchange. No broker will give you a 1:4 or 1:5 loan for 30 years at a low interest rate without the risk of forced closing of the position in case of market price drawdown. A mortgage allows you to fix the value of an asset today and pay with depreciating money tomorrow.

Thirdly - psychology. The price of a house or an apartment does not change in the trading terminal every second. You don't see the value of your apartment drop 10% or more in a single day, and you don't feel tempted to "sell everything" like you do with stocks. Investors often lose out on returns due to bad timing, whereas real estate saves the investor from their own emotions.

Gap between owners and tenants

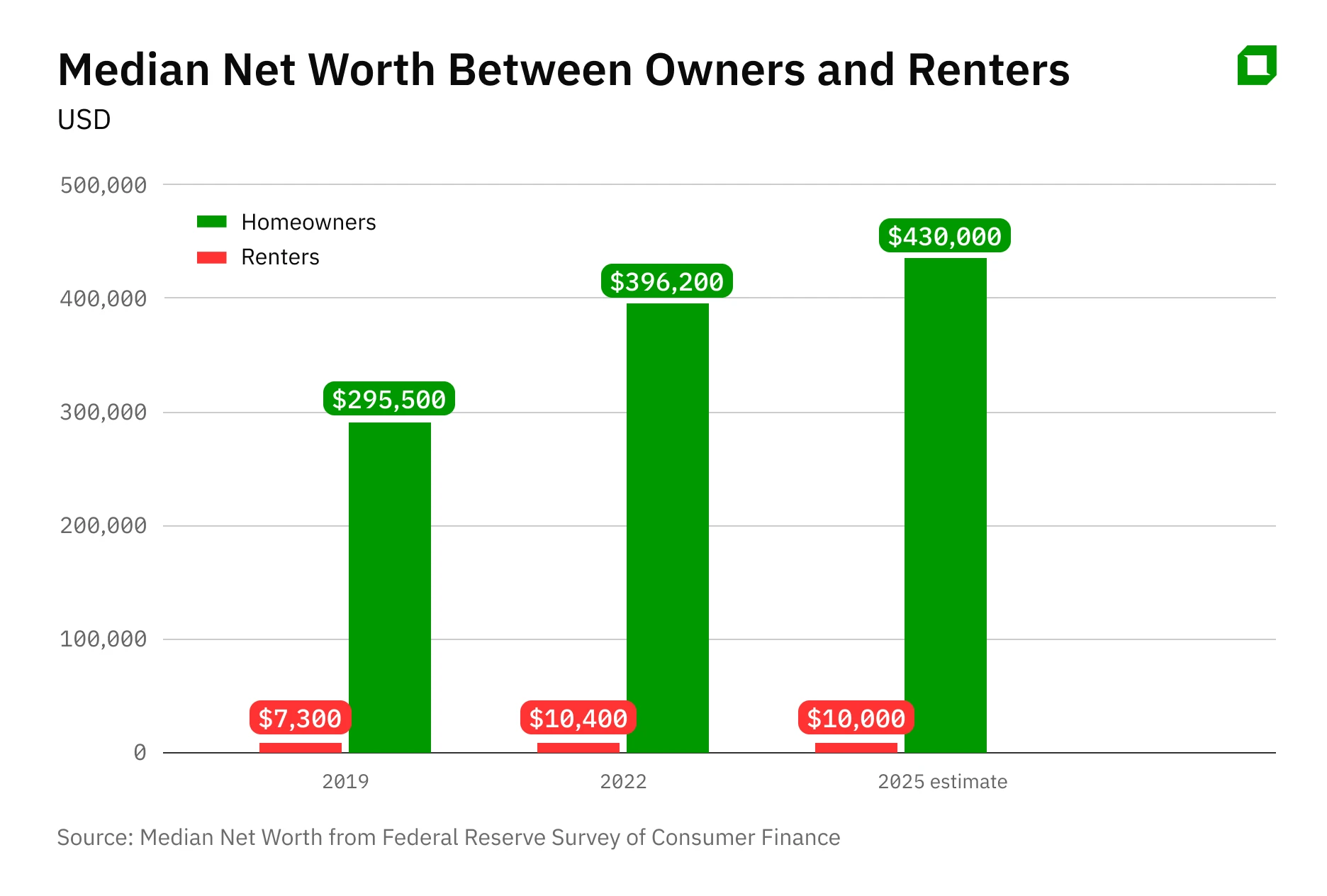

These theoretical conclusions are confirmed by real statistics. According to Federal Reserve calculations, the median wealth of a homeowner exceeds that of a renter by more than 40 times.

There is certainly a correlation effect here - the rich are more likely to buy houses, but the mechanism of "forced savings" through mortgages plays a key role in holding onto that wealth. It was housing equity that was the main driver of the post-pandemic jump in median American wealth.

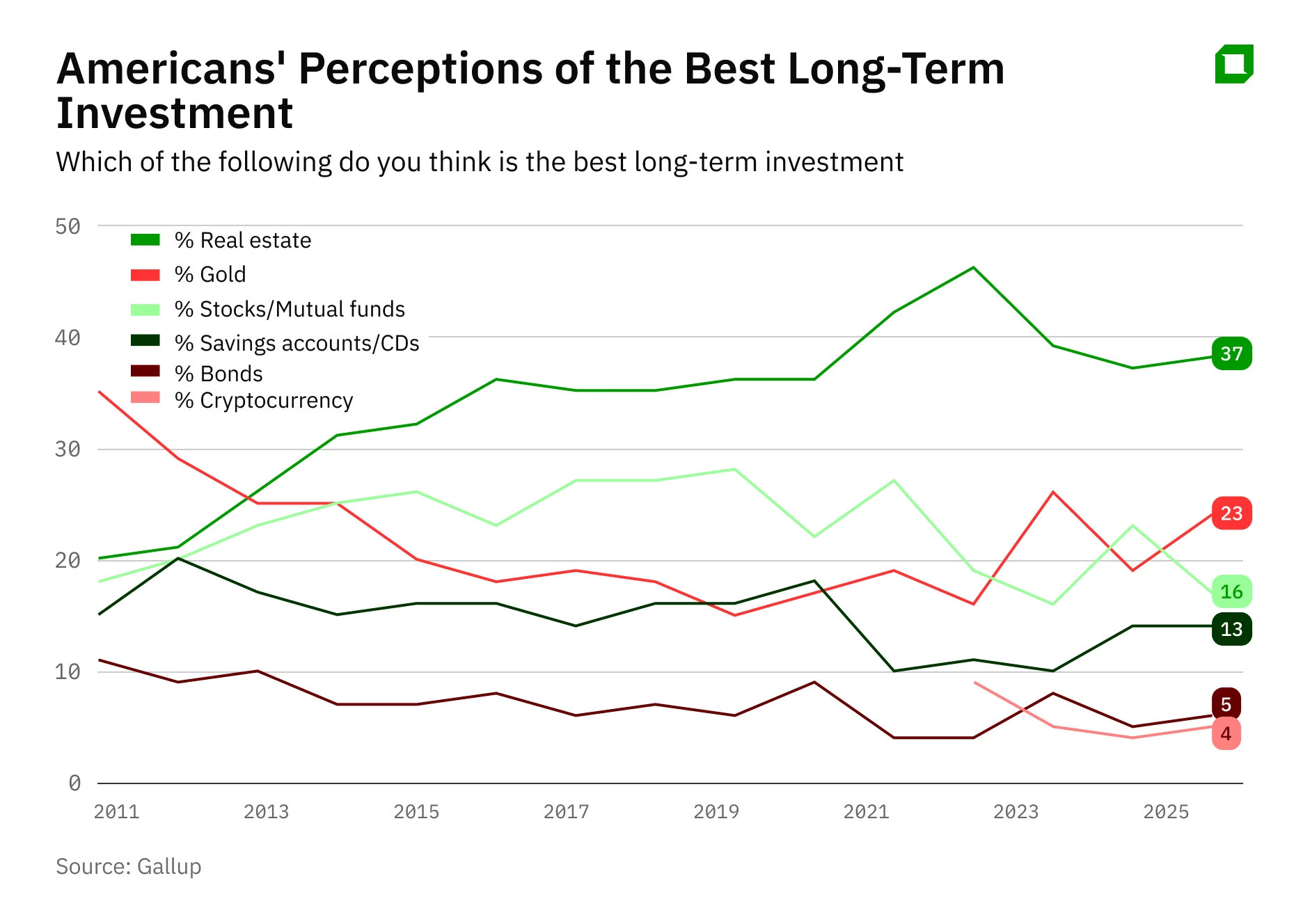

Interestingly, public opinion on this issue is in complete agreement with statistics. According to Gallup polls, Americans have been calling housing the best long-term investment for 12 years in a row. In the spring of 2025, 37% of respondents said so, while gold was chosen by 23% and stocks by 16%.

Playing down: your chances in the game against corporate landlords

To understand why the "forever rental" rate is so dangerous, you only need to look at the other side of the market - those who rent these homes.

A textbook example is Vonovia, the largest owner of residential real estate in Germany. The company manages hundreds of thousands of apartments. Its business model thrives on the same factor that makes life difficult for renters: the chronic shortage of housing.

In Europe, as in many developed markets, the rate of new construction lags disastrously behind population growth and migration. There is virtually no vacant housing - vacancy rate tends to zero. In such conditions, even with government regulation of rents, as in Berlin, market forces push prices up.

For a private investor, refusing to buy a condo means playing against giants like Vonovia. In effect, you are betting that your equity portfolio will grow faster than the appetites of corporate landlords in a supply-constrained environment.

Limitations that are important to keep in mind

It goes without saying that real estate could be stuck in a sideways trend for a long time or even fall in real terms, as happened in the US in the second half of the 'noughties' or in China and Germany after 2022. In addition, residential investments are characterized by reduced liquidity and risks of dangerous concentration: one expensive asset that depends on location and the local labor market.

And again - repairs, insurance, taxes and downtime when renting eat up some of the expected income. Finally, the price of entry is critical: overpayment in the "hot" market plus a high interest rate turns a mortgage into a heavy burden on the personal budget.

How do you put it all together into a personal investment strategy?

Including real estate in your personal investment portfolio is not a mistake or an "emotional purchase," but a mathematically sound decision. Housing reduces the volatility of your personal capital and works as an insurance against poverty in old age.

The choice of stocks or real estate is a false one. It should be a combination. But a diversified portfolio of stock assets, i.e. your personal bet on economic growth, works much better paired with an "anchor" in the form of your own home.

If you already own housing, and there is a lack of confidence in stocks and bonds, it is logical to add liquid real estate surrogates to your portfolio through publicly traded instruments. Residential and commercial REITs in developed countries offer a different risk profile and are less dependent on one specific location.

And most importantly, do not confuse a home for living and investment real estate. In the former, the goal is the quality and stability of your life. The second is profitability and liquidity, which are more likely to be higher with exchange-traded instruments.

This article was AI-translated and verified by a human editor