Small-cap ETF outperformers and underperformers in 1H25: Non-U.S. DMs ascendant

The first half of 2025 proved to be a roller coaster for small-cap investors. Exchange-traded funds investing in European and Asian small caps delivered strong returns, while U.S.-focused peers largely hovered around flat performance or slipped into the red.

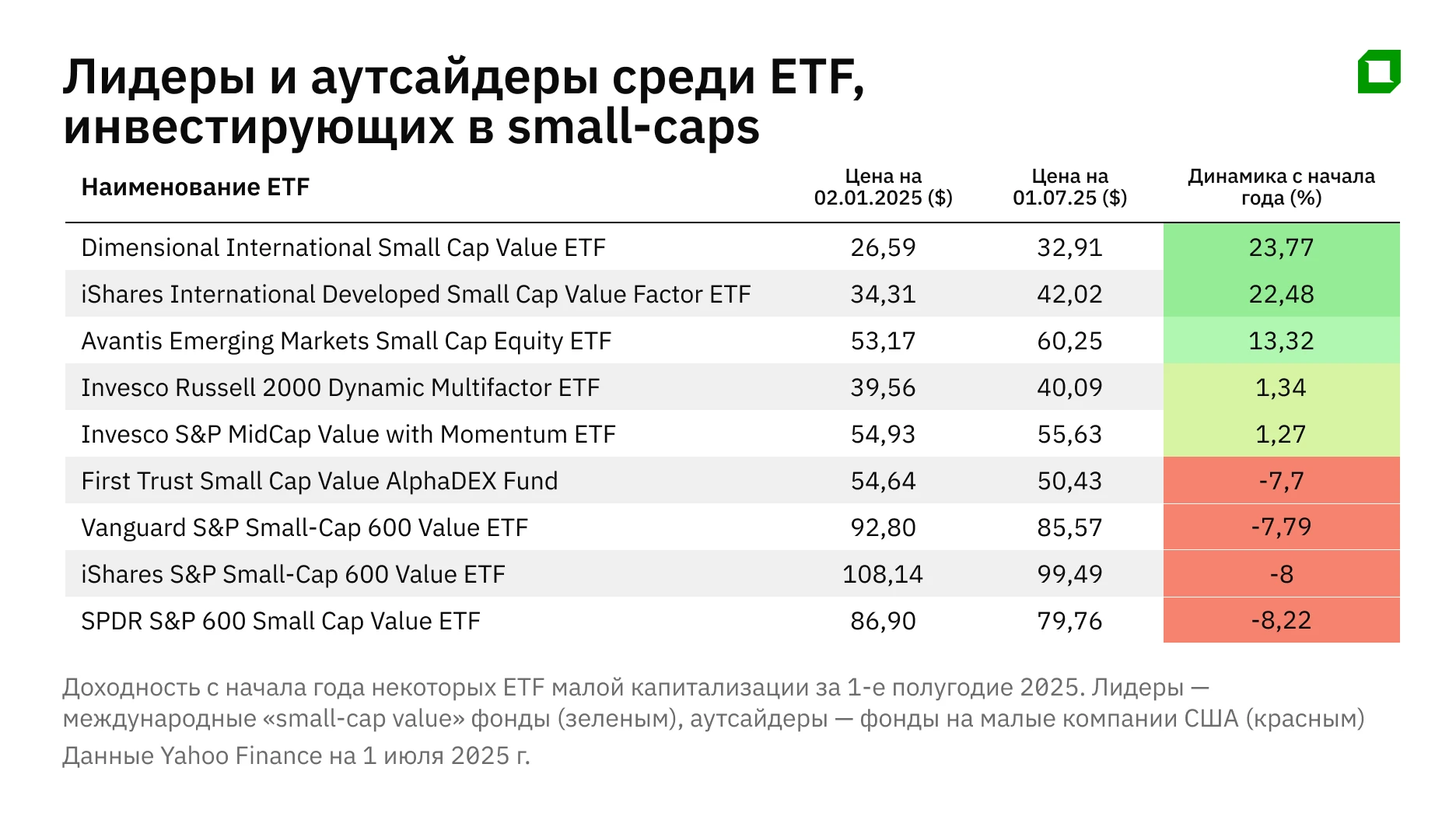

Analyst Aldiyar Anuarbekov examined which funds outperformed and which underperformed, and the reasons driving those outcomes.

Outperformers

Funds targeting undervalued small caps in developed markets outside the U.S. led performance in the first half. The Dimensional International Small Cap Value ETF (DISV) is up 23.8% year to date through July 1, while the iShares International Developed Small Cap Value Factor ETF (ISVL) has gained roughly 22.5%. Their returns significantly outpaced both peer funds and broader market indexes.

By comparison, the MSCI World Index rose 9.04% during the same period, and the S&P 500 advanced 5.72%. Hong Kong’s Hang Seng rallied nearly 22%, while European markets also posted strong gains, with Germany’s DAX up 16.4%. Canada’s TSX gaining 7.9%.

The best-performing small-cap funds maintained broad diversification across developed markets but excluded the U.S. For instance, DISV has notable exposure to Japan (23%), the UK (13%), and Canada (10%), along with positions in Australia, Switzerland, and Germany. These markets were viewed as particularly attractive in 2025. Japanese equities have benefited from ongoing corporate governance reforms and a stable policy stance from the BoJ. European stocks, many of which remain undervalued, drew interest amid Germany’s proposed loosening of its "debt brake" to fund higher defense and infrastructure spending. Canada, meanwhile, was supported by strength in commodity markets.

DISV and ISVL have concentrated exposure to traditional value sectors such as industrials, financials, energy, and raw materials, rather than growth stocks. Financials are key: Banks and other financial institutions make up a significant portion of both portfolios. Among the largest holdings are several European regional banks, including Italy’s Banca Mediolanum, Denmark’s Sydbank, and Swiss online brokerage Swissquote.

Information technology and other tech sectors account for less than 10% of assets in either ETF. That allocation strategy has worked in 2025 as investor enthusiasm for big tech has cooled, and the absence of the so-called Magnificent Seven in the portfolios proved to be a tailwind rather than a liability. As those overvalued U.S. names lost momentum, value-oriented international small-cap funds, long overlooked, finally had their moment.

Another standout in the first half was the Avantis Emerging Markets Small Cap Equity ETF (AVEE), which returned approximately 13.3% in January-June. It benefited from a strong rally in developing markets early in the year. By April, the MSCI Emerging Markets Index had already risen 5-6%, accelerating to a 15.4% rise by the end of the second quarter.

However, performance across regions was far from uniform. Eastern European markets surged, with Poland gaining 56.98%, Greece 51.54%, and Hungary 22.19%. Latin American equities were also strong, up 27.02%, while India posted a more modest 4.27% gain. In contrast, many Asian markets lagged: Thailand declined 12%, and China, while avoiding a collapse, has clearly lost its former momentum. As of March 31, 2025, AVEE’s top holdings included Chinese fintech Qifu Technology, toy manufacturer Pop Mart (known for its Labubu brand), and Brazilian aircraft maker Embraer. All were still categorized as small caps at the time of inclusion.

Underperformers

ETFs focused on U.S. small caps, particularly those tilted toward value stocks, were among the weakest performers in the first half. The SPDR S&P 600 Small Cap Value ETF (SLYV) fell 8.2% year to date, while the iShares S&P SmallCap 600 Value ETF (IJS) declined about 8.0%. More diversified strategies also struggled: Vanguard Small Cap Value (VBR) dropped 1.3%, and both the iShares Morningstar Small Cap Value ETF (ISCV) and the JPMorgan Active Small Cap Value ETF (JPSV) lost roughly 2.7%.

Only select niche strategies managed avoid the red ink. Multifactor strategies, including the Invesco Russell 2000 Dynamic Multifactor ETF and Momentum MidCap Value ETF, posted slight gains.

Still, some analysts believe U.S. small caps may be primed for a rebound. Valuations have fallen to multi-year lows relative to large-cap peers. In a recent market overview, Royce Investment Partners noted that if inflation continues to ease and the Fed begins cutting rates, small caps could outperform. For now, however, U.S. small caps remain laggards, having solidly underperformed their global peers in the first half of 2025.

Drivers: Weak dollar, rallying gold, rising defense spending

Small-cap funds benefited from a sharp weakening of the U.S. dollar. By the end of June, the greenback had declined more than 10%, marking its steepest first-half drop since the collapse of the Bretton Woods system, which had tied global currencies to the dollar and gold. The dollar’s slide boosted dollar-denominated returns on foreign small-cap ETFs and stimulated inflows into global equities.

A historic rally in gold further supported performance. The precious metal has surged 25% year to date, its strongest first-half gain since the 1970s, which lifted shares of gold producers. Canadian miner Kinross Gold, for example, has risen more than 60% since the beginning of the year. The company is the largest holding in ISVL, accounting for 2.6% of the fund’s portfolio.

Canadian energy companies were strong, supported by continued high oil and gas prices. Stable commodity revenues helped lift small-cap mining and energy firms, which make up between 10% and 20% of the ISVL and DISV portfolios.

In Europe, defense and industrial stocks surged amid rising military budgets. The STOXX Europe Aerospace & Defense Index, which tracks leading European defense firms, jumped nearly 70% in the first half of the year. That rally provided a broader tailwind for European equities overall.

Even at the start of 2025, analysts were anticipating a rebound in value stocks and a rotation into peripheral markets. According to a forecast by Cambridge Associates, emerging-market and non-U.S. developed-market equities were expected to perform on par with, or better than, the U.S., largely due to more attractive valuations. Small caps were viewed as prime beneficiaries of a shift away from overbought tech giants. Those predictions have largely played out. As Wall Street digested the aftermath of last year’s tech-driven surge, investors rotated toward more cyclical, "grounded" sectors. Undervalued areas, particularly small stocks from Europe, Japan, and Canada, have moved to the forefront.

The AI translation of this story was reviewed by a human editor.