Mind the Gap: why funds win over the investors who invest in them

In 2024, when the S&P 500 added 25%, the average investor received only 16.5%, according to a study by the financial-analytical company DALBAR. Over the long haul, the difference in returns is more modest, but the direction is the same: year after year, the "behavioral" downside eats up about 1% of the lost returns. It is not the commission or the quality of the strategy - it is a behavioral gap: the instrument is chosen correctly, but the moment is not. Economist Denis Elakhovsky wrote about the chronic problem of index funds and how a retail investor can avoid getting into trouble.

Entering "failure."

The magnitude of the problem is helped by Morningstar's Mind the Gap report. The company annually compares two values: the return of market funds, as if you invested a single amount at the beginning of the period and did not touch anything else, and the return of investors in these funds, where all real capital inflows and outflows are taken into account. The difference between these values is the "gap" - the behavioral gap.

According to the latest report, the average return to investors in the U.S. for the decade ending December 31, 2024 was below the return of the funds themselves over the same period by about 1.2% per year. That's not a random margin of error. The report shows that the gap is wider in funds where strategies are narrower and more volatile, and where cash flows within the fund change direction more frequently, from an influx of clients to a noticeable exodus. In mixed portfolios, the gap is minimal, while in sectoral and thematic portfolios it is maximum.

Why guessing the "perfect moment" is almost always more expensive

The 2024 Mind the Gap report mentions another important detail. The yield gap between index mutual funds - mutual funds - and their clients is close to zero, while in the case of index ETFs it is noticeably larger. The explanation for this discrepancy is simple: if a client wants to sell a unit in a mutual fund, he has to wait for the provider to calculate its price at the end of the trading session, while ETFs can be sold in the market by anyone at any time, and under the influence of emotions, this moment can easily be chosen poorly.

Classic studies of investor behavior show the same pattern: the more actively one trades, the lower one's outcome relative to the passive alternative.

The famous work of Brad Barber and Terence Odean, based on data from tens of thousands of private investor accounts, captures a consistent penalty for active trading: the more frequent the trades, the lower the bottom line. In addition, investors are often inclined to move money into funds that have shown high returns in the recent past and withdraw money from those whose past performance has been below market, according to the study by Andrea Frazzini and Owen Lamont. That is a direct contradiction to the age-old investment disclaimer: "past returns do not guarantee future performance."

Professional managers are a little better at "market timing", i.e. the ability to consistently guess the ideal moments for entering and exiting the market. The work of Hendrickson and Murton, who tested the ability of fund managers to predict quote movements, did not reveal such a skill, and what looks like skill often turns out to be simple luck.

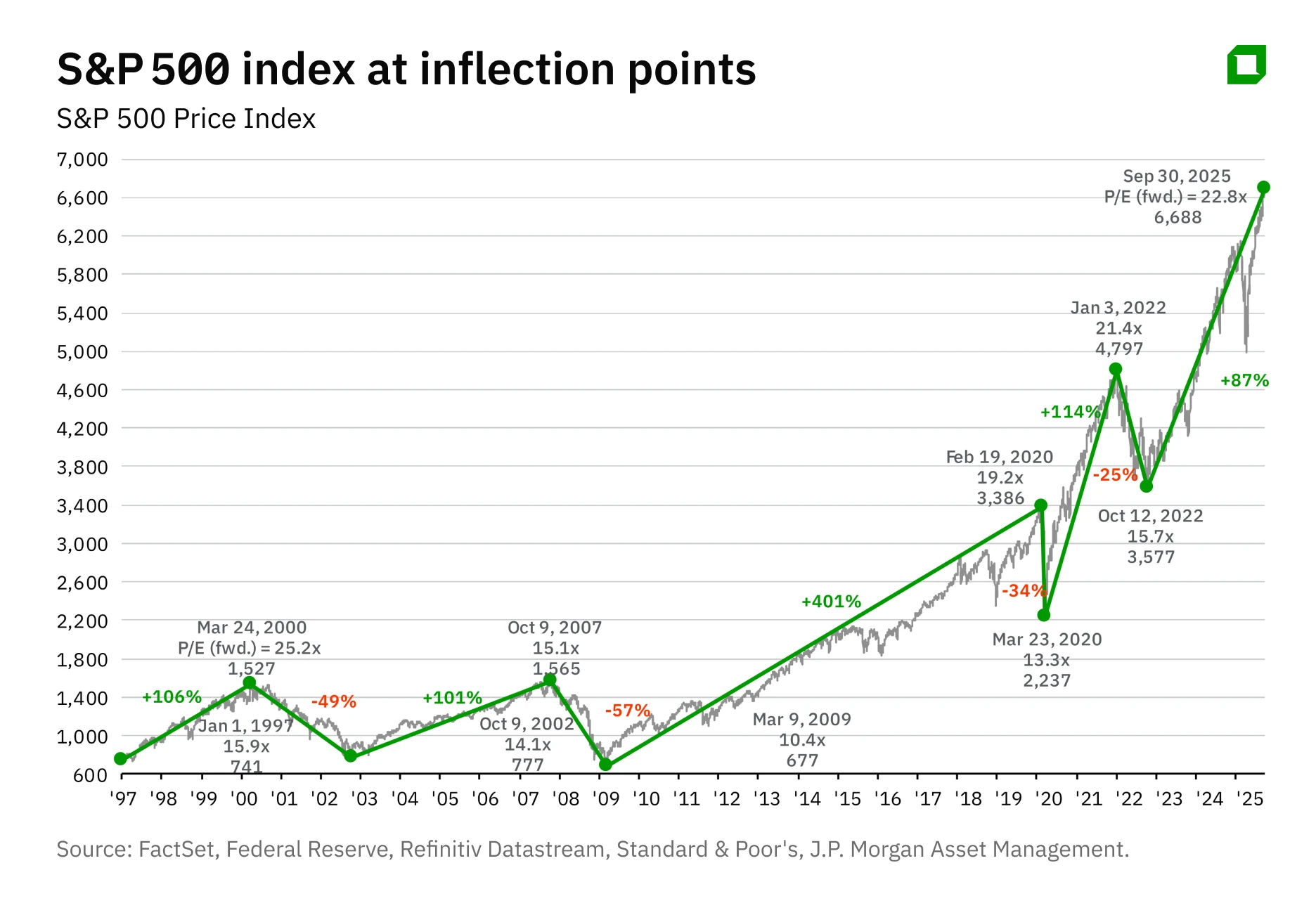

The effect is amplified when the attention of a large number of investors is focused on bright topics and one or two sectors. There emotions are more than usual, and decisions are made more often. Plus the simple arithmetic of the best and worst days on the market works. The days of the fastest growth are often next to the most painful falls. An attempt to wait out the storm "on the fence" and return in time can easily turn into missing a few of the best days, which account for the lion's share of the final profit.

How to close the "behavioral gap"

Auto replenishment and scheduled rebalancing. The most reliable way to bring the investor's return closer to the fund's return is to remove unnecessary "manual" decisions from the process. Fix the day of replenishment, fix the rebalancing rule, do not go overboard with the frequency. Regularity is more important than guesswork. Methodologically, this is exactly what the Mind the Gap report recommends Morningstar do to narrow the gap.

Simple portfolio base. Broad indices and mixed solutions - as the main dish, narrow topics - as pepper and salt, according to taste. The share of "spices" should be such that even in a drawdown the basic strategy does not break down. This reduces the risk of a "big idea mistake".

Fewer triggers to action. If you catch yourself reaching for the "buy" or "sell" button, remove the triggers. Turn off unnecessary notifications, reduce the amount of time you spend in the brokerage application, make a "rule of silence" on days of high volatility.

Instruments to suit your personality. If the ETF format pushes for intraday decisions, move the underlying share to mutual funds with the same index, and leave ETFs for clear tactical tasks. If, on the contrary, discipline is enough, use ETFs, but with predetermined rules.

This article was AI-translated and verified by a human editor