From euphoria to calculation: which small-caps can win the AI race in 2026

Absci Biotech uses generative AI to develop new drugs / Photo: X / Absci

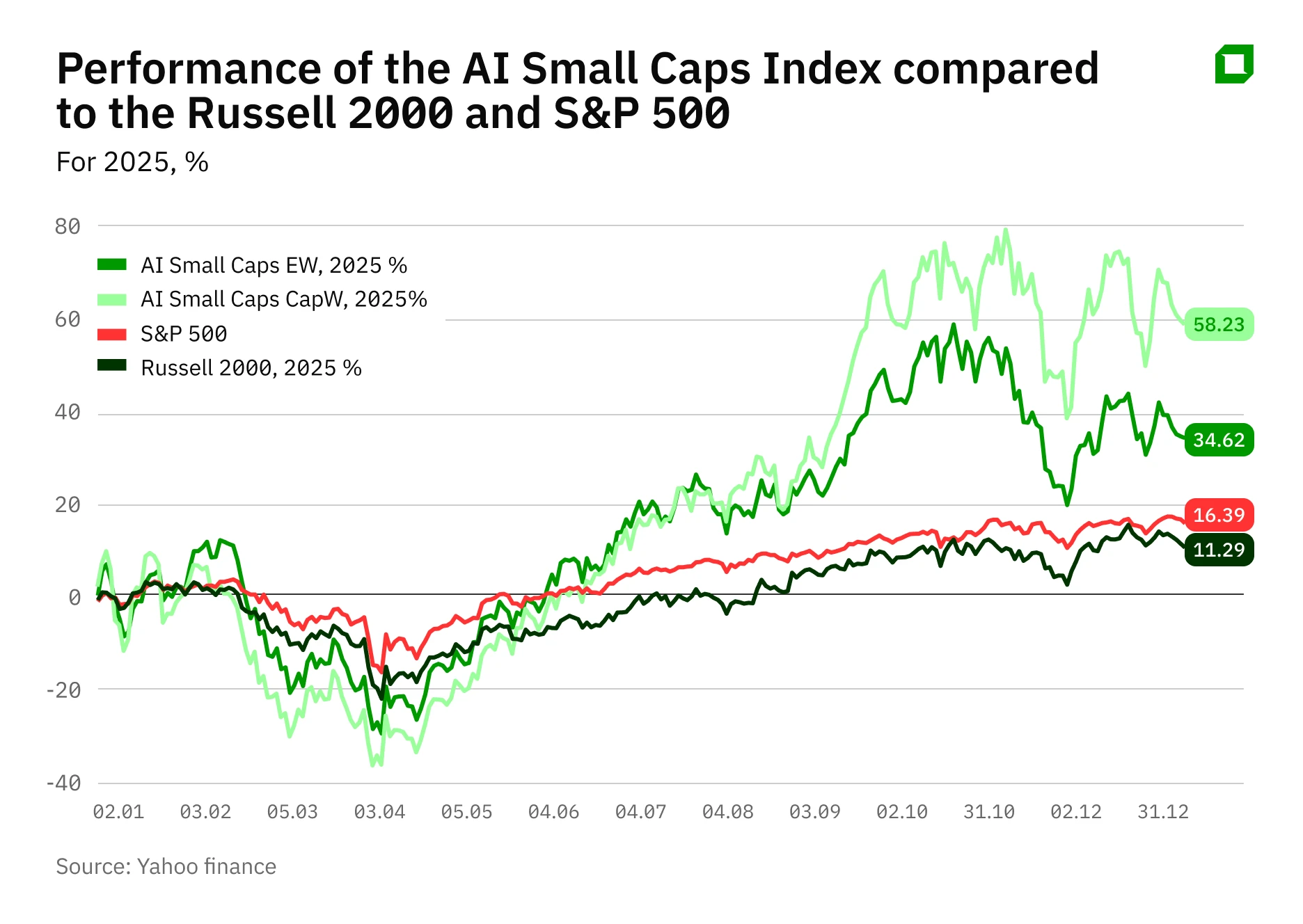

AI Small Cap Index, calculated specially for Oninvest by analyst Aldiyar Anuarbekov, showed impressive growth in 2025. The index includes 43 small-cap companies whose activities are related to AI infrastructure, sensorics, robotics and quantum computing. At year-end 2025, the equal-weighted AI Small Cap EW Index is up 34.6%, while the AI Small Cap Cap EW Index, calculated by capitalization size, is up 58.2%. By comparison, the S&P 500 Broad Market Index rose 16.3%, while the Russell 2000, which includes small and mid-cap stocks, added 11.3% over the same period.

However, at the beginning of 2026, the picture has changed: the AI Small Cap EW Index has gone negative by 8.8%, while the version calculated on the basis of capitalization is still in the plus by 8.6%. This gap shows that only a few large companies are driving the main growth, while most of the smaller index participants are lagging behind.

This is also evident from the results of 2025: only 23 out of 43 companies of the index were in the plus in 2025, while 20 ended the year with a decline. In fact, the entire dynamics of the index was "pulled" by a few strongest players. The leaders in 2025 were companies from the infrastructure and application segments of AI: Lumentum (optical components for networks and data centers), Applied Digital (data center capacity for high-performance computing), Kratos Defense (defense technologies and unmanned systems), Aeva (lidars and sensors for autonomous systems), and Pagaya (AI-based scoring and lending fintech platform).

Notably, about a third of AI Small Cap Index companies ended 2025 with a net loss. Among them are Applied Digital, whose shares grew by 214% and showed one of the best results in the index, and SoundHound AI, whose securities fell by about 50% over the same period.

Investors are becoming more discerning

Although the market expects the AI boom to continue, in 2026 investors are becoming noticeably more selective in their approach. UBS strategists noted in their February 2026 Global Strategy review that growth in AI will continue, but not all companies will benefit. UBS warns that businesses with weak financial performance and high debt loads are particularly vulnerable to the rising costs of AI deployment and debt servicing. A wave of defaults worth tens of billions of dollars is possible in the credit markets - primarily among leveraged IT companies - if their business models start losing competition in the AI era. In other words, the possible "deflation" of the bubble in the AI sector will primarily hit the weakest borrowers.

Capital is increasingly being deployed where the demand for AI is supported by real contracts and investments, Wells Fargo strategists agree (Equity Strategy review February 09, 2026). For small-cap companies, balance sheet strength and cost control are becoming key factors. Having significant cash reserves and reducing losses are now critical. Overall, this reflects a broader shift in the market: while in 2025 investors were willing to back almost any AI project, in 2026 the focus is shifting to practical returns from technology - real contracts, infrastructure and financial sustainability - rather than speculative growth.

In many ways, 2026 could be a test of sorts for small AI companies. On the one hand, there is still a huge demand: Big Tech's capital investments in artificial intelligence, according to RBC analysts' estimates, grew by 61% in 2025 and will continue to increase in 2026. On the other hand, only those small-caps that manage to prove the viability of their technologies and withstand a period of tougher competition and expensive capital will be able to take advantage of this growth.

Biotech, anti-fraud, security: three promising stocks from the AI Small Cap Index

Against the backdrop of the new market conditions, several companies from the AI Small Cap Index stand out as showing steady progress. We selected three of them - Absci, Mitek Systems and Evolv Technology.

Absci Corporation (ABSI)

Absci is a biotech company that uses generative AI to develop new drugs. The company has collaborations with Merck, pharma manufacturer Almirall and AI biotech Owkin, which confirms the industry's interest in Absci's technology. Clinical trials of its flagship candidate ABS-201, an antibody for the treatment of alopecia areata, began in late 2025, and management emphasizes that it is focusing on the most promising areas - primarily alopecia and endometriosis - to maximize return on investment.

The financial results reflect a transitional stage of development. Absci's revenue in the third quarter of 2025 was just $380,000 versus $1.7 million a year earlier, falling short of market expectations. Meanwhile, adjusted net loss per share was 20 cents versus a loss of 24 cents a year earlier, a result in line with analysts' forecast. In the summer of 2025, the company raised $64 million in additional capital, bringing total cash to $117 million. According to the company's own estimates, this is enough to fund operations through at least the first half of 2028. Such a liquidity reserve allows investors to consider Absci in the long term.

Morgan Stanley analysts in a review of Absci note that the company has shifted its focus to the riskier but potentially more significant asset ABS-201. This means that the investment case in the coming years will largely depend on the drug's early clinical data. Morgan Stanley has given Absci's shares an Equal Weight rating and a target price of $4.3; it implies a price target of about 80% upside to the closing price on March 9. According to MarketWatch, the company's shares are advised to buy by eight analysts (Buy rating), while two more advise holding them (Hold). The average target is $8.05, which means the securities can grow almost 3.4 times.

Mitek Systems (MITK)

Mitek Systems is an American developer of digital identity and fraud prevention solutions. The company specializes in AI-based identity and document authentication.

The company's fiscal 2025 (ended Sept. 30) was a record year for revenue, up 4% year-over-year to $179.7 million, with revenue from subscription and service products, including cloud solutions, up 21% to $77 million. GAAP net income was $8.8 million, compared to $3.3 million a year earlier. Mitek raised its fiscal 2026 revenue guidance to $187 million-$197 million, announced the redemption of $155.3 million in convertible notes and announced a $50 million share repurchase program.

According to analysts at Craig-Hallum Capital Group, the subscription model growth and strong balance sheet (about $196 million in cash at the end of 2025) create a good environment for further business expansion. In January 2026, the bank reiterated a Buy recommendation on the company's shares and raised its target price to $17. According to MarketWatch, five Wall Street analysts advise buying the company's shares, with an average target of $14.75, which is close to its current value.

Evolv Technology (EVLV)

Evolv Technology - develops AI-based non-contact weapon detection systems. Such solutions are especially in demand amid growing attention to security in public places. In the third quarter of 2025, Evolv's revenue increased 57% year-over-year to $42.9 million. Adjusted loss per share narrowed to 2 cents, while analysts expected 3 cents per share. Moreover, the company reported positive EBITDA for the first time at $5.1 million (a margin of about 12%) versus negative EBITDA of $3 million a year earlier. Annual recurring revenue (ARR) added 25% year-over-year to $117 million.

The company raised its forecast for 2025: expected revenue is $142 mln-$145 mln, which implies growth of 37-40% (previously expected 27-30%). The EBITDA margin forecast has also been improved - the company now expects high single digits. In addition, the management announced plans to reach positive free cash flow as early as in the fourth quarter of 2025, which will bring the business closer to self-sufficiency.

Craig-Hallum analysts noted that Evolv Technology was able to settle Federal Trade Commission (FTC) claims over marketing claims about the scanners' accuracy. As a result, no major customers have canceled their contracts with the company. Craig-Hallum reiterated a Buy rating on shares of Evolv in January 2026 and raised the target price to $10, reiterating a Buy rating. Analysts at Lake Street Capital Markets and Needham & Company also estimate the fair value of the company in the range of $9-10 per share. They attribute this to strong revenue growth, Evolv's gradual emergence to profitability, and the market's potential. The stock has a total of four Buy ratings from Wall Street analysts, MarketWatch shows. The average target of $9.88 implies a nearly doubling of the stock price.

Does not constitute individualized investment advice.