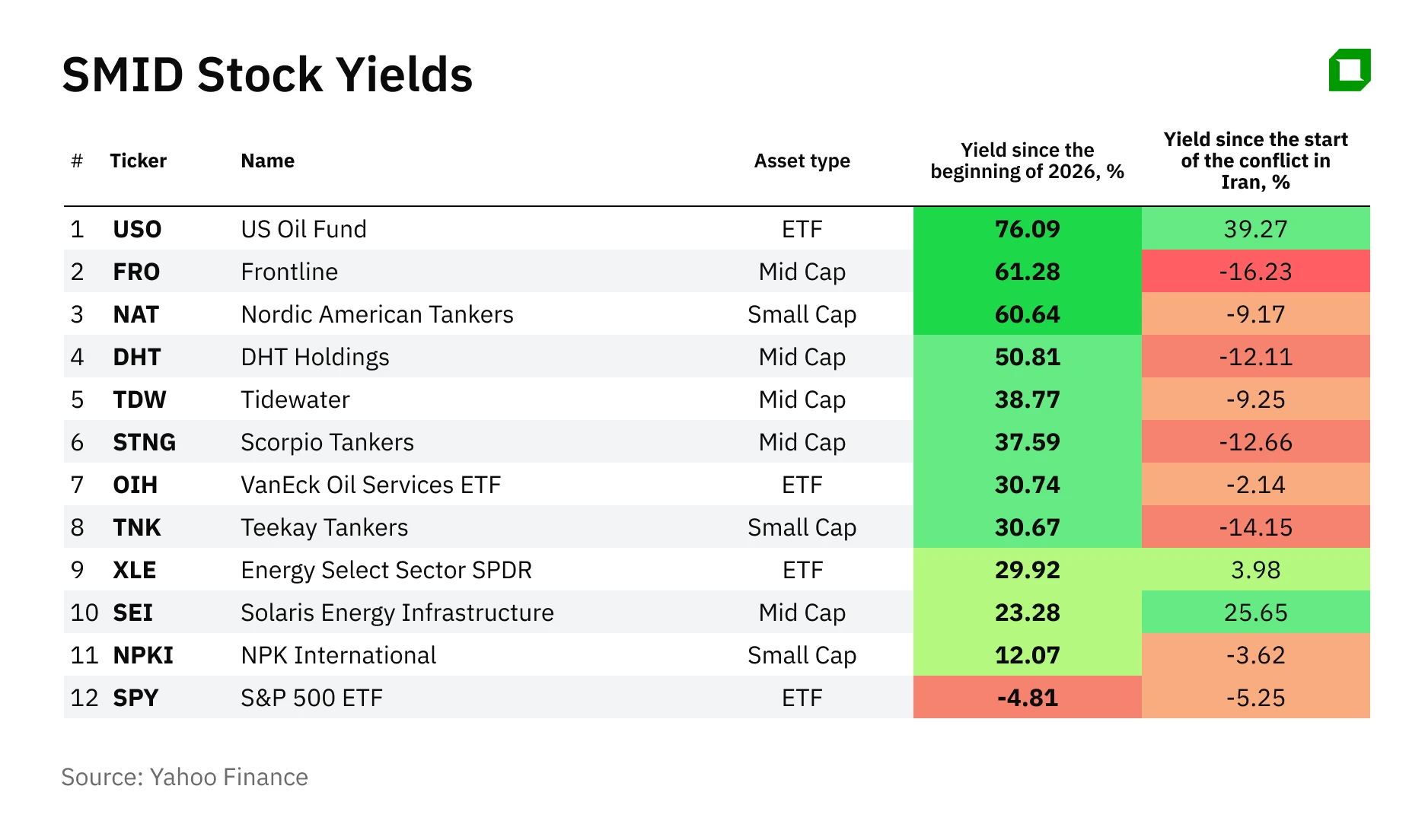

Tankers and oilfield services: Eight stocks and one ETF being buoyed by the oil shock

Amid the escalating conflict in the Middle East, the oil shipping sector is experiencing one of its strongest periods in recent years, with freight rates up 30-40% / Photo: Shutterstock.com

The conflict between the U.S. and Israel and Iran has sharply reshaped the global oil market over the past three weeks. The Strait of Hormuz, through which around a fifth of global oil supply transits, has been effectively closed. Prices have reacted quickly: oil is up about 50% and gas 55% versus the end of February. Brent crude has stabilized around $100 per barrel, having briefly jumped to $119, while regional benchmarks Dubai crude and Oman crude are above $150 per barrel, with Dubai having rising as high as $166. Against this backdrop, seaborne oil transport, as a sector, is experiencing one of its strongest periods in recent years – longer routes are boosting ton-mile demand, and freight rates have risen 30-40% depending on the region.

Winners from the oil shock

We have selected eight stocks and one fund that share a high sensitivity to geopolitics and oil prices. Tanker operators benefit from longer routes and higher freight rates, while oil services companies gain from increased drilling.

The consensus on these stocks remains cautious: many target prices set before the war are significantly below current levels. This suggests the market is now either pricing in a prolonged crisis or could correct quickly at the first signs of stabilization. Such stocks are suited to investors with a high risk tolerance and the ability to react quickly to news.

Frontline

Frontline (FRO) is one of the world’s largest operators of large crude tankers, including VLCC and Suezmax vessels. In the fourth quarter, Frontline’s net income surged 240% year over year to $228 million ($1.02 per share), while revenue rose 46.7% to $624.5 million. Average time charter equivalent rates reached $74,200 per day for VLCCs (up 116% quarter over quarter) and $53,800 for Suezmax (up 53%). The company said that for the first quarter of 2026, VLCC rates are booked at $107,100 per day and Suezmax at $76,700.

As Frontline CEO Lars Barstad noted, “periods of volatility tend to create opportunities.” Since the start of the year, Frontline shares have gained 47.43%. Evercore on March 2 reiterated an “outperform” rating on the stock and raised its target price from $42 per share to $46 per share. This is one of the highest targets on Wall Street, implying upside of nearly 36% versus the Monday close. According to MarketWatch data, 10 analysts rate the stock “buy,” three “hold,” and one “sell.” The average target price is $37.70 per share.

Nordic American Tankers

Nordic American Tankers (NAT), a Bermuda-based company with a fleet of 20 Suezmax tankers, operates vessels suited for routes such as the Suez Canal. In the fourth quarter, net income totaled $11.7 million versus $1.3 million a year earlier. EBITDA rose 57% to $34.7 million, while average rates increased 25% quarter over quarter to $35,000 per day.

In late February, the company signed a one-year contract with a major oil company at a rate above $50,000 per day, and earlier announced a deal to build two new tankers at $86 million each, with delivery scheduled for 2028.

Since the start of 2026, Nordic American Tankers shares have gained more than 52%. B. Riley assigned a “buy” rating with a $7.50 target price, implying upside of 42.8%. The company has three ratings, a “buy,” a “hold,” and a “sell,” according to MarketWatch data. The average target is $6 per share.

DHT Holdings

DHT Holdings (DHT) describes itself as an independent operator of a fleet of VLCC tankers, with offices in Monaco, Norway, Singapore, and India. Each vessel can carry about 2 million barrels of crude oil. In the fourth quarter, net income rose 20.8% year over year to $66.1 million, while shipping revenue increased 10% to $143.8 million. The company estimates that 76% of spot days for the first quarter of 2026 are booked at $78,900. In January, it took delivery of the first of four new VLCC tankers.

Since the start of the year, DHT Holdings shares have gained more than 40%. Analysts at Evercore and Fearnley Securities in early March upgraded the stock to “buy” and “outperform,” respectively. Evercore’s $23 target price implies upside of 29.4%, while Fearnley sees the stock rising to $21, or 18.2% above current levels. According to MarketWatch data, the company has six “buy” ratings versus three “hold” ratings. The average target is $19.14 per share.

Scorpio Tankers

Scorpio Tankers (STNG) is the largest operator of tankers transporting refined products such as gasoline and diesel. Over the past five years, the company has significantly strengthened its balance sheet: net debt fell from $3.1 billion at the end of 2021 to a net cash position of $309 million as of February 2026.

In the fourth quarter, net income rose 87% year over year to $128.1 million, while adjusted EBITDA increased 44% to $152 million. Vessel operating revenue rose nearly 24% to $252.7 million, and liquidity exceeds $1.7 billion. The company has ordered 10 new tankers and continues to renew its fleet by selling older vessels. At the same time, there is a risk: about 54% of LR2 tankers are currently used to transport crude oil, which could intensify competition if the market normalizes.

Evercore in early March maintained its “outperform” rating on Scorpio Tankers and raised its target price from $83 per share to $90 per share, implying upside of 27.3%. Fearnley Securities also upgraded the stock to “buy” at a $79 target price, for upside of 11.7%.

Teekay Tankers

Teekay Tankers (TNK) operates about 56 mid-size tankers, with offices in eight countries. In the fourth quarter, net income rose 46% year over year to $120 million ($3.47 per share). Free cash flow totaled $112 million. Cash increased to $853 million, with no debt outstanding after the company repaid its last obligations in March 2024.

Shares of Teekay Tankers have risen 30% since the start of the year. On March 17, Fearnley Securities upgraded the stock from “hold” to “buy” with a $83 per share target price, for about 23% upside. Four analysts rate the stock “buy,” while one recommends “hold” and one “sell.” The average target is $79.50 per share.

Tidewater

Tidewater (TDW) is a major operator of offshore support vessels with a 70-year history. The company services oil production by transporting personnel and equipment, as well as providing towing and anchoring support. When oil prices are high, demand for such services increases alongside drilling activity.

In 2025, revenue rose 0.5% year over year to $1.35 billion. Net income increased 85% to $334.7 million ($6.64 per share), although a significant portion of the growth was driven by a one-off tax effect of $201.5 million. Free cash flow rose 29% year over year to a record $426 million. Tidewater forecasts 2026 revenue in the range of $1.43 billion to $1.48 billion, partly supported by the $500 million acquisition of Wilson Sons Ultratug Offshore. CEO Quintin Kneen said the deal would expand the fleet in Brazil from six to 28 vessels and add about $220 million in annual revenue with a 58% gross margin.

Tidewater shares have gained nearly 50% year to date. Most analysts rate the stock “hold,” while three recommend “buy” and one “sell.” The average target price is $85.70 per share, implying about 13% upside. Clarkson Securities reiterated its “buy” rating with a $100 target price per share on a six-month horizon, one of the highest targets on Wall Street for the stock.

NPK International

NPK International (NPKI), a small-cap company based in Texas founded in 1932, produces and rents composite matting used for access to drilling sites, pipelines, and energy infrastructure. In the fourth quarter, earnings per share came in at $0.17 versus a consensus estimate of $0.10. Revenue in 2025 rose 27% year over year to $277 million. In 2026, the company expects revenue in a range of $305-325 million.

Shares of NPK International have gained nearly 20% since the start of the year. Following the annual report, B. Riley raised its target price to $19 per share from $16 per share and reiterated its “buy” call. According to MarketWatch data, five analysts cover the stock, all of whom rate it “buy.” The average target is $18.80 per share, nearly one-third above current levels.

Solaris Energy Infrastructure

Solaris Energy Infrastructure (SEI) provides mobile and scalable distributed power generation solutions, working with oil and gas companies and data centers.

Revenue nearly doubled in 2025 to $622 million. The company is rapidly expanding capacity: in October, it raised $650 million in a convertible notes deal, and in March it acquired about 900 MW of turbine capacity. The management plans to increase total capacity to 3,100 MW by 2029.

According to MarketWatch data, 13 analysts rate the stock “buy,” with an average target price of $69.77 per share. Last Thursday, Wells Fargo initiated coverage with an “equal weight” rating and a $71 target price per share, implying upside of 16.6%.

VanEck Oil Services ETF

The OIH ETF, which is intended to track the overall performance of U.S.-listed companies involved in oil services to the upstream oil sector, has gained about 42% since the start of 2026, making it one of the best-performing sector ETFs. Its top holdings include SLB (18%), Baker Hughes (12%), Halliburton (7%), TechnipFMC (6%), and Transocean (5%). Assets under management exceed $2 billion, with a total expense ratio of 0.35%.

The fund offers diversified exposure to the sector without the need to pick individual stocks. Jeff Krimmel of Krimmel Strategy Group believes the oil services segment is now clawing back nearly 20 years of return underperformance versus the tech sector.

This material does not constitute individualized investment advice.