Three AI small caps that look ready to extend gains as investors grow more selective

Absci Biotech uses generative AI to develop new drugs / Photo: X / Absci

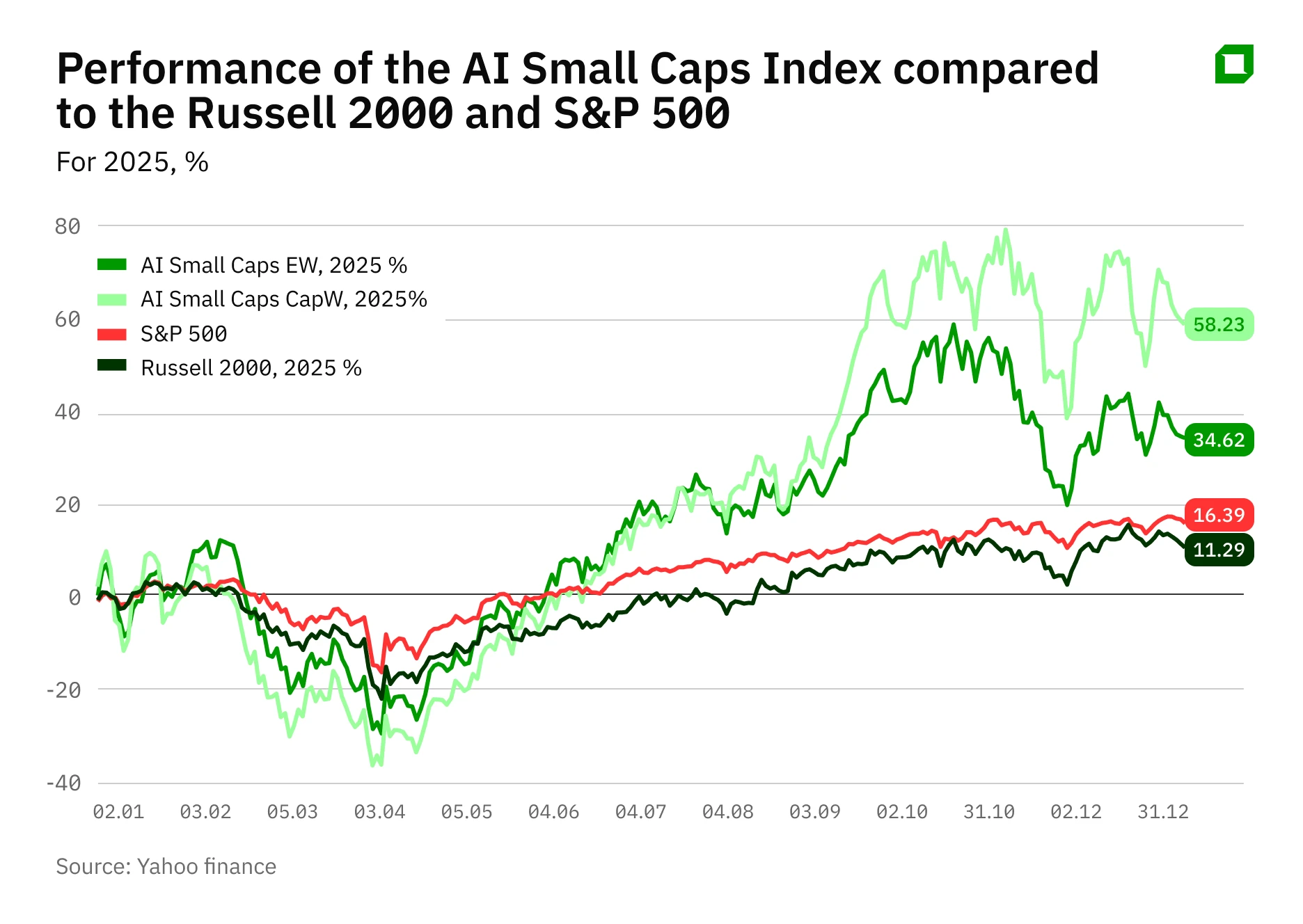

The AI Small Cap Index, assembled for Oninvest by analyst Aldiyar Anuarbekov, delivered a strong gain in 2025. The index includes 43 small caps whose businesses are linked to AI infrastructure, sensing technologies, robotics, and quantum computing. For 2025, the equal-weight index climbed 34.6%, while the cap-weight index rose 58.2%. For comparison, the broad-market S&P 500 gained 16.3%, while the Russell 2000, which tracks smid-cap companies, advanced 11.3% over the same period.

However, the picture shifted at the start of 2026. The EW index has fallen 8.8%, while the CW index remains in positive territory, up 8.6%. The divergence suggests that the bulk of the gains is being driven by only a handful of larger companies, while most smaller constituents are lagging.

The results for 2025 illustrate the same pattern. Of the index’s 43 names, only 23 finished the year higher, while 20 ended the year with losses. The index's leaders, which drove the headline gain in 2025, were companies operating in AI infrastructure and applied segments: Lumentum Holdings, which produces optical components for networks and data centers; Applied Digital, which provides data center capacity for high-performance computing; Kratos Defense & Security Solutions, focused on defense technologies and unmanned systems; Aeva Technologies, which develops lidar and sensor systems for autonomous platforms; and Pagaya Technologies, an AI-based credit scoring and lending platform.

Notably, roughly a third of companies in the AI Small Cap Index ended 2025 with a net loss. Among them was Applied Digital, whose stock surged 214%, one of the strongest performances in the index, as well as SoundHound AI, whose shares fell about 50% last year.

Investors getting more selective

Even as markets expect the AI boom to continue, investors are becoming noticeably more selective in 2026. Strategists at UBS said in a February global strategy report that growth in AI is likely to persist, but not every company will benefit. UBS warns that businesses with weak financial metrics and heavy debt burdens are particularly vulnerable as spending on AI adoption and debt servicing rises. Credit markets could see a wave of defaults worth tens of billions of dollars – primarily among heavily leveraged tech companies – if their business models begin to lose ground in the AI era. In other words, any potential deflation of the AI bubble would likely hit the weakest borrowers first.

Capital is increasingly flowing to companies where demand for AI is backed by real contracts and investment, strategists at Wells Fargo said in an equity strategy report from February. For small caps, balance sheet strength and cost discipline have become decisive factors. Large cash reserves and narrowing losses now play a critical role. More broadly, this reflects a wider shift in markets. In 2025, investors were willing to back almost any AI-related project. In 2026, the focus is moving toward tangible returns from the technology – real contracts, infrastructure, and financial resilience rather than speculative growth.

In many ways, 2026 could become a stress test for small-cap AI companies. On the one hand, demand remains enormous. Capex by Big Tech on AI, according to estimates by RBC Wealth Management analysts, rose 61% in 2025 and continues to increase in 2026. On the other hand, only those small caps that can demonstrate the viability of their technology and withstand a period of tougher competition and more expensive capital will be able to capitalize on that growth.

Three small-cap AI ideas

Against this backdrop, several companies in the AI Small Cap Index stand out, and they include Absci, Mitek Systems, and Evolv Technology.

Absci

Absci (ABSI) is a biotechnology company that uses generative AI to develop new medicines. The company works with Merck, pharmaceutical manufacturer Almirall, and AI biotech firm Owkin, which underscores industry interest in Absci’s technology. At the end of 2025, clinical trials began for the company’s flagship candidate ABS-201 – an antibody designed to treat hair loss. The management says it is focusing on the most promising indications – particularly alopecia and endometriosis – in order to maximize return on investment.

Financial results reflect a transitional stage in the company’s development. Absci’s revenue in the third quarter of 2025 totaled just $380,000 versus $1.7 million a year earlier, falling short of market expectations. At the same time, the adjusted net loss of $0.20 per share was in line with analyst forecasts and an improvement on the loss of $0.24 per share a year earlier. In summer 2025, the company raised $64 million in additional capital, bringing total cash to $117 million. According to the company’s own estimates, that is sufficient to fund operations at least into the first half of 2028. Such reserves allow investors to view Absci as a long-term opportunity.

Analysts at Morgan Stanley say Absci has shifted its focus toward the riskier but potentially more significant asset ABS-201. This means the investment case in the coming years will depend heavily on early clinical data for the drug. Morgan Stanley assigned Absci shares an “equal weight” rating at a target price of $4.30 per share, implying roughly 80% upside versus the closing price on Monday. According to MarketWatch data, eight analysts recommend “buy,” while two advise “hold.” The average target price is $8.05 per share, implying the stock could rise nearly 3.4 times.

Mitek Systems

Mitek Systems (MITK) is a U.S. developer of digital identity verification and fraud-prevention solutions. The company specializes in verifying identities and documents using AI. Fiscal 2025, ended September 30, was a record year for revenue. Sales rose 4% year over year to $179.7 million, while revenue from subscription and service products, including cloud solutions, climbed 21% to $77 million. Net income under GAAP totaled $8.8 million versus $3.3 million a year earlier. Mitek also raised its revenue outlook for fiscal 2026 to $187-197 million, reported the repayment of $155.3 million in convertible bonds, and announced a $50 million share buyback.

Analysts at Craig-Hallum Capital Group say the expansion of the subscription model and a strong balance sheet – roughly $196 million in cash at the end of 2025 – create favorable conditions for further business growth. In January 2026, the bank reiterated its “buy” rating on the stock and raised its target price to $17 per share. According to MarketWatch data, five Wall Street analysts rate the stock a "buy," with an average target price of $14.75 per share, roughly in line with current levels.

Evolv Technology

Evolv Technology (EVLV) develops AI-powered contactless weapon-detection systems. Such solutions are gaining traction as attention to security in public spaces increases. In the third quarter of 2025, Evolv’s revenue jumped 57% year over year to $42.9 million. The adjusted loss narrowed to $0.02 per share, while analysts had expected a loss of $0.03 per share. The company also reported positive EBITDA for the first time – $5.1 million, with a margin of about 12%, compared with negative $3.0 million a year earlier. Annual recurring revenue (ARR) rose 25% year over year to $117 million.

The company raised its guidance for 2025, forecasting revenue of $142-145 million, implying growth of 37-40%, up from a previous estimate of 27-30%. The EBITDA margin outlook was also improved, with the company now expecting high single-digit levels. The management also said it expects to generate positive free cash flow as early as the fourth quarter of 2025, which would bring the business closer to break even.

Analysts at Craig-Hallum Capital Group previously said Evolv had settled claims from the U.S. Federal Trade Commission related to marketing statements about the accuracy of its scanners, with none of the company’s major customers terminating their contracts. In January, Craig-Hallum reiterated its “buy” rating on Evolv shares and raised its target price to $10 per share.

Analysts at Lake Street Capital Markets and Needham & Company also estimate the company’s fair value at $9-10 per share. They cite strong revenue growth, Evolv’s gradual path to profitability, and the market’s potential. Overall, the stock carries four “buy” ratings from Wall Street analysts, according to MarketWatch data. The average target price is $9.88 per share, implying the stock could nearly double.

This material does not constitute individualized investment advice.