Iran war: what the oil market may be underestimating

Why the impact of conflict on prices may be more important than the loss of barrels

Oil prices fell 10 percent on March 10 after Trump's ultimatum to Iran not to block the Strait of Hormuz / Photo: Facebook / US NAVY

For the first time in history, oil prices fluctuated in the range of $30 per day. Alexey Golubovich, analyst at Arbat Capital Advisory Services Limited (UK), and Alexander Orlov, managing director of Arbat Capital, consider possible scenarios for the oil market.

A war the market wasn't expecting

Until February 28, most investors in the world - apparently, except for insiders in understandable countries - were skeptical about an attack against Iran anytime soon. And this is not just the word of investment portfolio managers in the U.S. who I was able to talk to or read their comments on March 1. Had it been otherwise, the market would have bought oil in advance and sold off as stock indices of countries in the region - at a minimum. So Trump's unprecedented, even by the standards of US politics, decision came as a surprise to most professionals. Most believed, and apparently still believe, that Trump's foreign and domestic policies are logical and consistent because he wants low oil and gasoline prices. Does that mean he will take any available path to rather quell resistance or "de-escalate the conflict"?

Initially, investors assumed that the Iranian army would not be able to resist for long and effectively. Nor will Iran be able to close the Strait of Hormuz for long, as the U.S., Europe and the Gulf states still hope. We are not military experts, but the Iranian army is weak compared to the US and Israel who attacked it. Pentagon chief Hegseth said on March 4 that Iran's air defenses are just days away from being suppressed, after which the Israeli and U.S. Air Forces will begin striking at protected sites throughout the country.

In total, the operation, according to Hegseth, will last up to eight weeks. This coincides with the statements of serious Western military analysts that even with the will of the new Iranian leadership to resist, the U.S. can win - that is, "bomb everything" in two months or faster.

Iran's asymmetric response has been the main surprise of recent weeks. Already 3-4 days after the war began, discussions of its economic and investment implications were dominated by speculation that the Iranians would not surrender quickly in the event of a ground operation.

Risk of physical loss of production: scenario scenarios

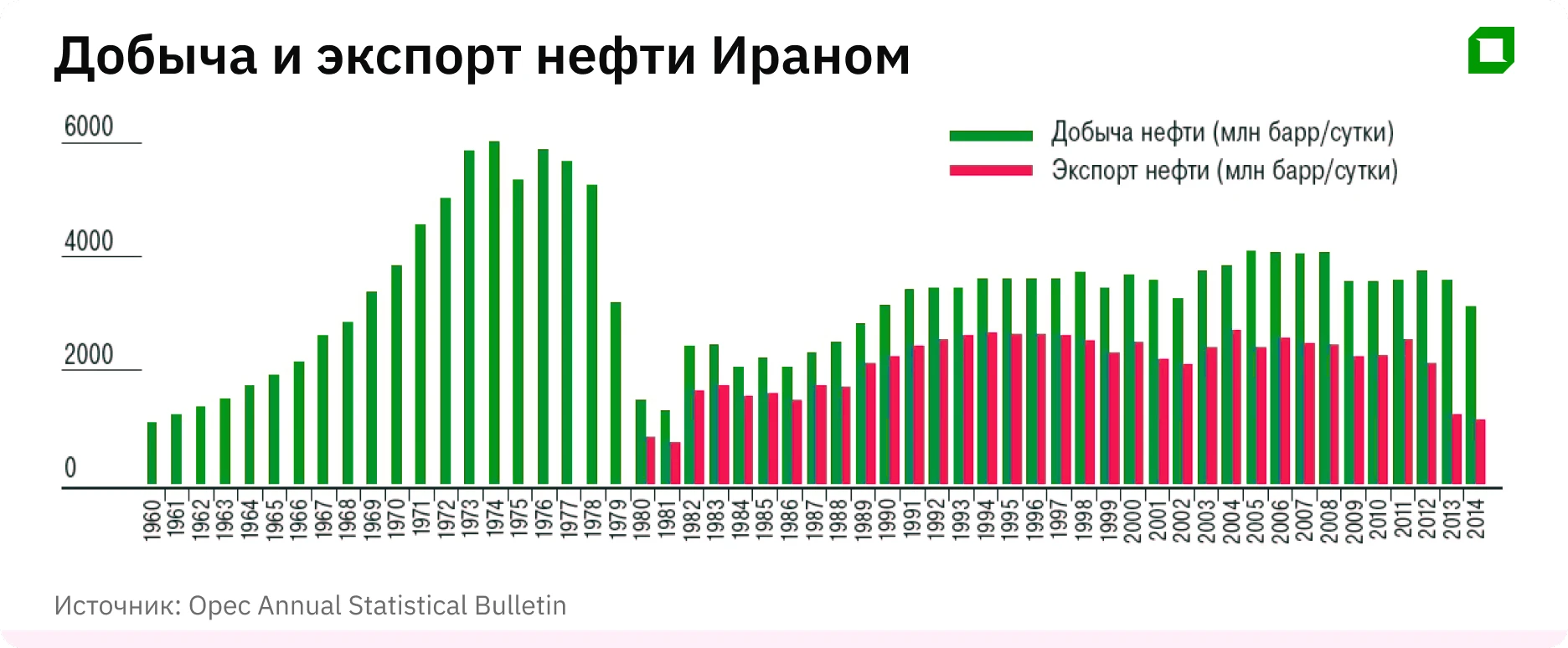

The risk of losing production capacity concerns both "hostile" Iranian countries and Iran itself, which produces 3 million barrels per day (mbd). The Islamic Republic exports 1-1.5 mbd. The market may lose this volume for several months or even years, as it did after the overthrow of the Gaddafi regime in Libya.

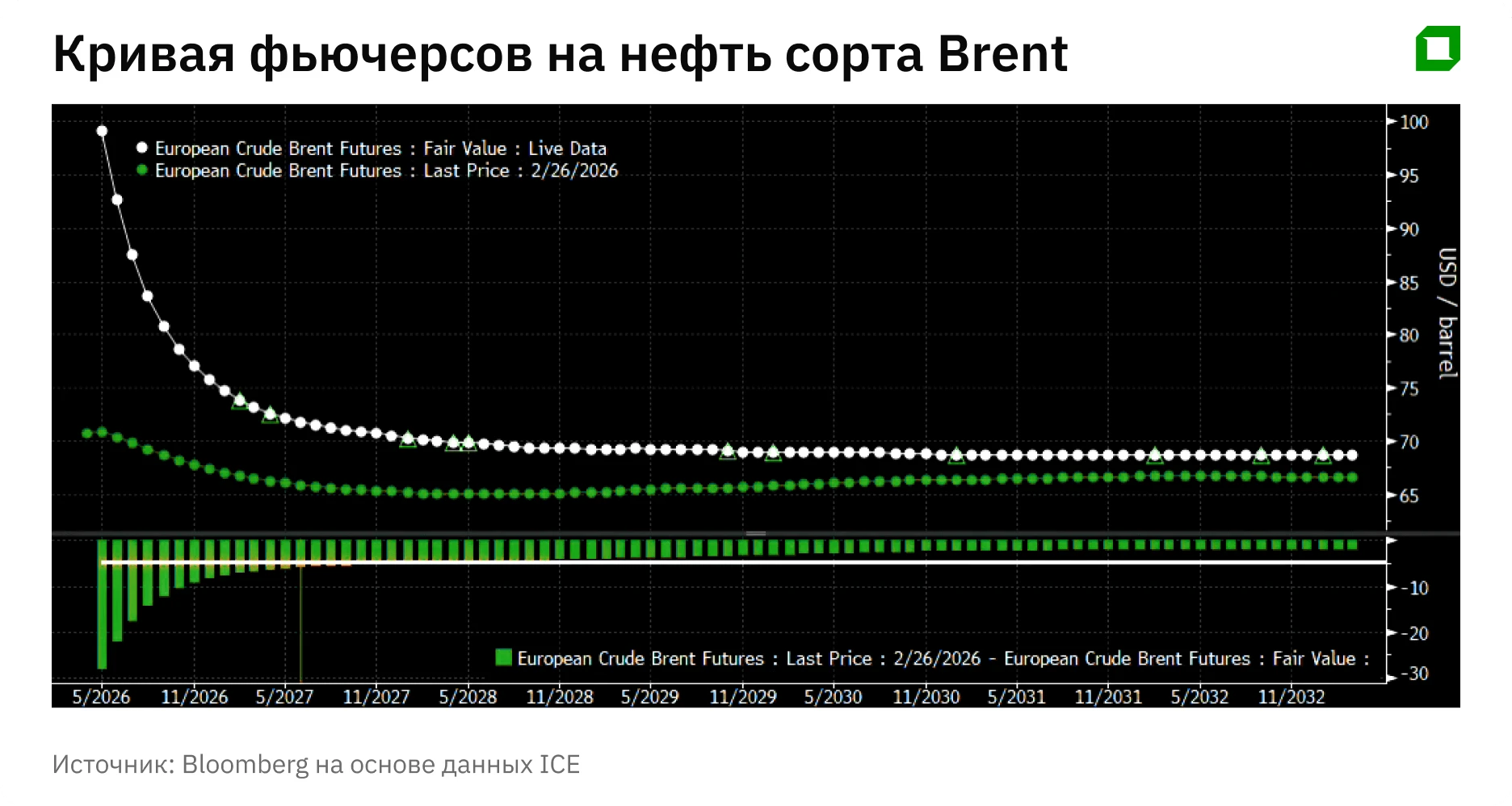

The Brent futures curve shows that the market is only laying down a short-term supply shock for now. Prices for long-distance supplies - in 2027-2030 - have barely risen since the start of hostilities. Only contracts for the May 2026-May 2027 period have risen in price by more than $5 per barrel. The annualized backwardation between these contracts is about 28%, indicating short-term fears of oil shortages rather than expectations of long-term supply destruction.

50% we are betting that production will be almost unaffected and only logistics infrastructure and oil storage will be destroyed, which will be compensated over time by OPEC+ production growth and falling demand due to higher oil prices.

In case of a radical change of power in Iran, sanctions may be eased under the "oil (discounted) in exchange for food" scheme - like Iraq in the '90s. If so, this is the most bearish scenario for oil. Not the destruction of a supplier, but instead additional barrels on the market. It would be an ideal scenario for Trump for the mid-term congressional elections (a repeat of the "Venezuelan blitzkrieg"), but we would not call it "basic" - the "quick victory war" has already failed. It is increasingly likely that the conflict will turn into a protracted confrontation, and some Middle Eastern oil will drop out of the global market for a long time.

Suffering neighbors

What do Iran's neighbors in the Persian Gulf, the "oil giants": Saudi Arabia and its satellites - Bahrain, Kuwait and the UAE, as well as Iraq, need? Definitely not the strengthening of Iran, especially under the "new American roof" and with the inevitable significant increase in oil exports. What is needed is an analysis of what will happen to oil production in neighboring countries when (if) Iran changes to a US-friendly regime. Between the two wars in Iraq, the US wanted guarantees that money from its oil exports would not be used for weapons. The scheme usually imposed through the UN - oil proceeds go to humanitarian needs (food, medicine - contracts with the West) could happen again. We are already seeing this with Venezuela and even without UN involvement. But if the US wants to lower oil prices and at the same time guarantee that the money will not be used for things unacceptable to the US, then Iran will want, at the very least, to manage the money itself.

The future of Iranian barrels

Which countries will be the main markets for Iranian oil? In the past few months, Iranian barrels have had a hard time finding buyers. Mostly exports went steadily to China, but China cannot buy everything, and with total sanctions and military risks, it does not want to. That's why "floating storage" rose in January - March, and this oil can quickly enter the market (potentially up to 100 million barrels in tanker storage).

If Iran surrenders and is allowed to sell oil, subject to controls on how the proceeds are used, traders such as Vitol and Trafigura will be able to monitor under U.S. supervision what the money is spent on.

Arguments for a bullish scenario for oil

Closing the strait instantly caused insurance and freight costs to rise many times over. "Opening" the strait by even completely destroying Iranian military bases and army missile units that could fire on ships does not mean that tanker insurance would immediately decrease.

In case of serious bombing of terminals and other infrastructure, it could take more than a year to restore production. It is also bullish for the far end of the Brent price curve, the probability of this is still 50%, but it is increasing with each new round of escalation.

Iran's retaliatory missile and drone strikes against the UAE, Qatar, Kuwait and Saudi Arabia would devastate industries, especially logistics and oil and gas, and hit aluminum, fertilizer producers and the financial sector.

We should separately note historical examples of the influence of Middle East conflicts on the oil price:

The 1973 oil embargo in response to the "Doomsday" war: a consolidated and aggressive economic response by the Arab/Islamic world led to a quadrupling of oil prices and a stagflationary shock in the developed world. The S&P 500 fell 40% from its peak - comparable to the collapse during the 2008 financial crisis. The result was a fundamental change in the entire oil market structure and even the global monetary system - the collapse of the Bretton Woods financial system and the transition to a "petrodollar" system was complete

The Iranian Revolution in 1979 and the war with Iraq in 1980: Iranian production collapsed threefold. Foreign companies left the country and their assets were nationalized by the new government. World oil prices reacted by doubling, but without such a global effect as in the early and mid-70s. Although the second wave of stagflation hit the U.S., Reaganomics, coupled with an aggressive JCP from Fed Chairman Paul Volcker, helped the U.S. to get out of the crisis quickly.

Iraq's invasion of Kuwait in 1990 and the US Operation Desert Storm: oil prices initially rose by 130%, but returned to their previous level after a few months, and by the mid-1990s had already fallen to three times their 1990 peak.

The second operation of the US and allies against Iraq in March-May 2003: a rare example of a "quick victorious war". Therefore, oil prices rose BEFORE the operation started, adding 50% in December-March, but collapsed AFTER the operation started to the initial level. And then the longer term trend continued as part of the "commodity price super-cycle" due to increased Chinese demand.

Arguments for a bearish scenario for oil

Low oil prices are important both within the US and on the international market. But there is an element of global competition here: the EU and Japanese industries will suffer more from rising oil and gas prices than the US, whose risk is only a rise in gasoline prices before the congressional elections.

The flow through Hormuz has been stopped for a while. But is "briefly" another 2 weeks or 2 months? And that's the big question if one had to bet that at most in 6 months all Iranian oil would be back.

Russia's exports are thought to be "weakening," but its discounts are helping prices, as are more than 135 million barrels in floating storage.

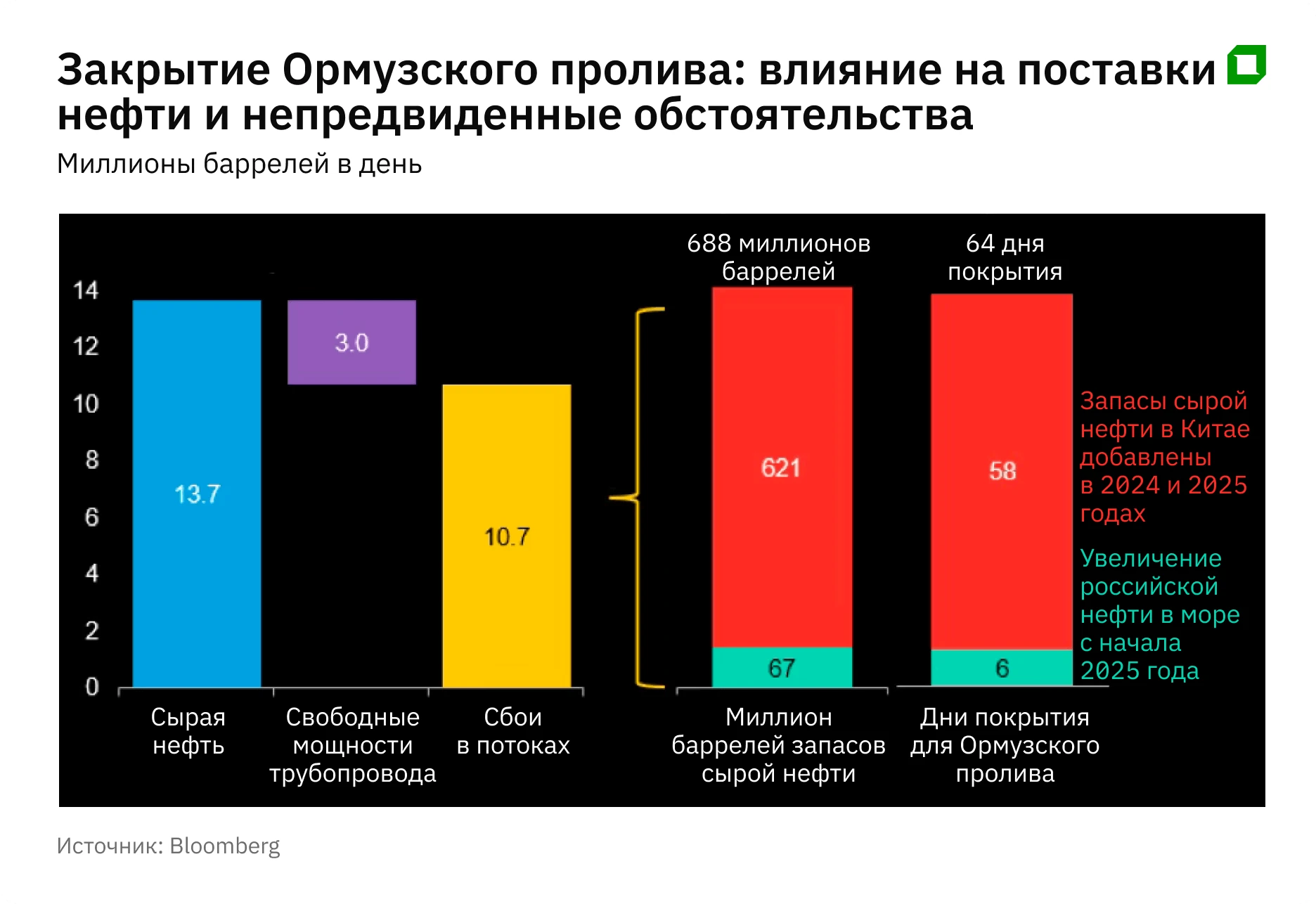

Even if the probability of a long-term lockout is low, the impact is still high. One can argue where the market will be when the conflict escalates. So far it is in the range of $85-100 (the top on historical precedents), but it could be much higher, as on the morning of March 9 in illiquid trading in Asia - up to $120. However, the volume of oil reserves in China (plus Russian floating storage facilities) makes it possible to survive up to 64 days of full closure of the Strait of Hormuz.

There is a huge call skew. What will all those who are long on calls do? Will they close their positions? If yes, oil may fall sharply - the standard market principle "buy on rumors - sell on facts" will work

The market remains well supplied in developed countries as well. There is plenty of supply, although not all in the right place, but tankers are getting there. Stocks in OECD countries were above the 5- and 10-year averages before the war, which in the long term best describes the dynamics of oil prices. There are already reports that the G7 countries are preparing to dump oil from their reserves on the market, and the US authorities are also calling for the same, but the Trump administration is still against it.

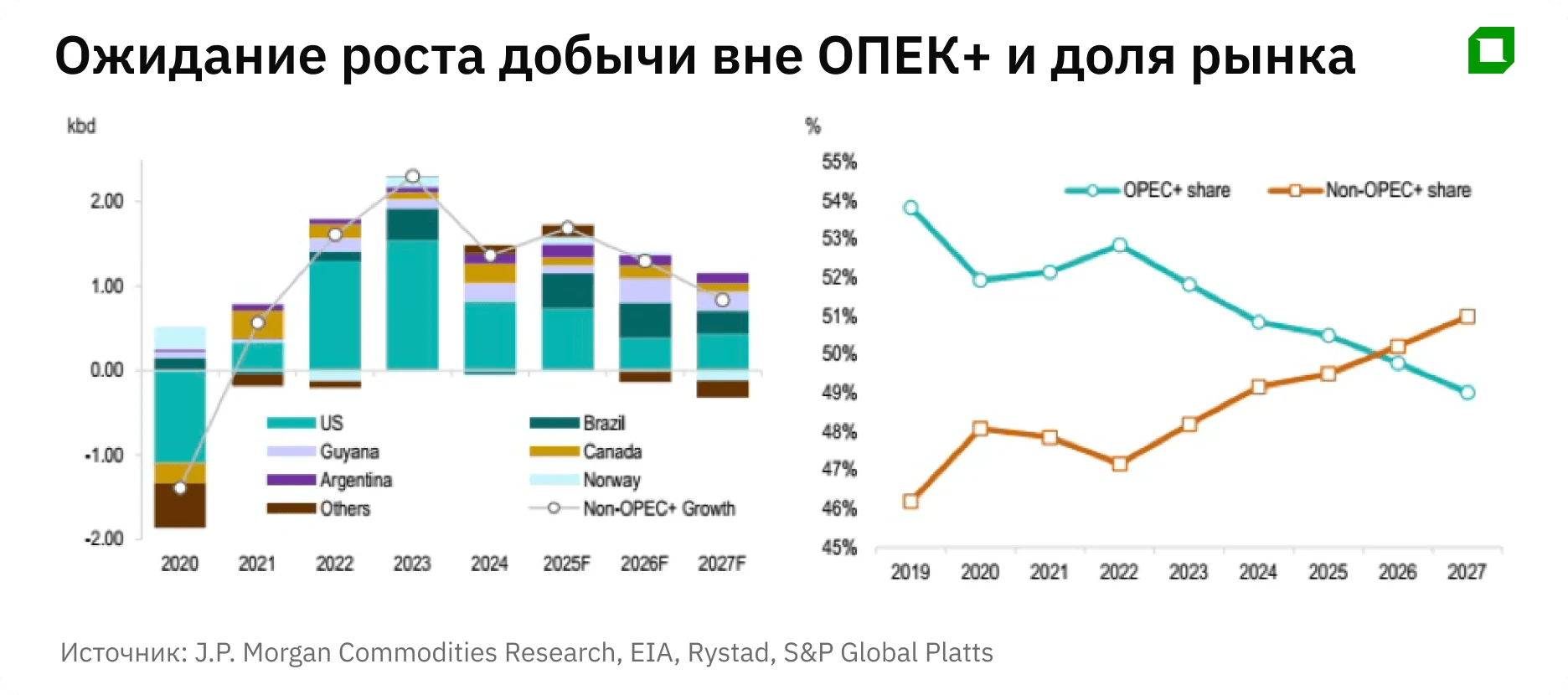

When the Russian "SWO" began, the market went much higher than could be expected - then the losses from Russian oil exports amounted to 3 million barrels per day, from exports of oil products - another 2-2.5 million barrels per day. Iran exports only 1.5 million barrels of oil. However, at that time, in 2022, OPEC's free capacity was at a lower level. Now the OPEC+ countries have announced that they will increase supplies by another 260 thousand barrels per day. That's not much, but it must be understood in context - since the beginning of last year, OPEC+ has returned more than 2 million bpd of real production to the market - more than 1 million by Saudi Arabia alone. And another 2.87 million bpd of "authorized production," meaning that de facto, there has been a de facto increase in production quotas by almost 3 million bpd.

The Middle East and OPEC are becoming less and less important - the main production growth is in other regions: the US, Canada, Brazil, Guyana and now Venezuela.

What it means for the investor

Thus, for the time being we can stick to the investment speculative strategy in oil based on two scenarios. Either the war will last at least a month and drive the price higher by at least 10%, but more likely by 15% or more to the current level of $120 as a probable ceiling.

In case Iran is able to deal a serious blow to the FEC of its competitors, the "bearish" scenario for oil - a quick return to the prices of the beginning of the year - is not realized before the second half of the year.

The negative consequences for the global economy and financial markets will depend on both the speed of the conflict's conclusion and the reaction of the authorities in the countries that have free oil reserves - from the partial lifting of sanctions on Russia to the sale of oil from the strategic reserves of OECD countries and China's oil interventions.

This article was AI-translated and verified by a human editor