How to make money on small caps in the gaming sector

Video games remain one of the fastest growing categories in the entertainment industry. According to Bloomberg Intelligence estimates, total global sales of gaming companies exceeded $183 billion in 2024. Analysts expect the upward trend to continue amid structural technological shifts, including the development of cloud gaming, the use of AI tools in game development, and the emergence of new gaming platforms.

Cloud gaming is expanding particularly rapidly. Annual sales in the segment totaled about $6.5 billion in 2024, yet they could grow more than fivefold to $35 billion by 2034, according to a Bloomberg Intelligence forecast. Growth is supported by two key factors: the adoption of generative AI, which accelerates development cycles and expands content scope, and the proliferation of cloud services that allow high quality games to run on mobile devices, even in regions without widespread access to gaming consoles.

Together, these factors are creating a favorable investment backdrop for the gaming sector as a whole. The industry is becoming more global, more advanced in terms of technology, and more scalable, with smaller publishers gaining access to a worldwide audience.

Gaming small caps performance

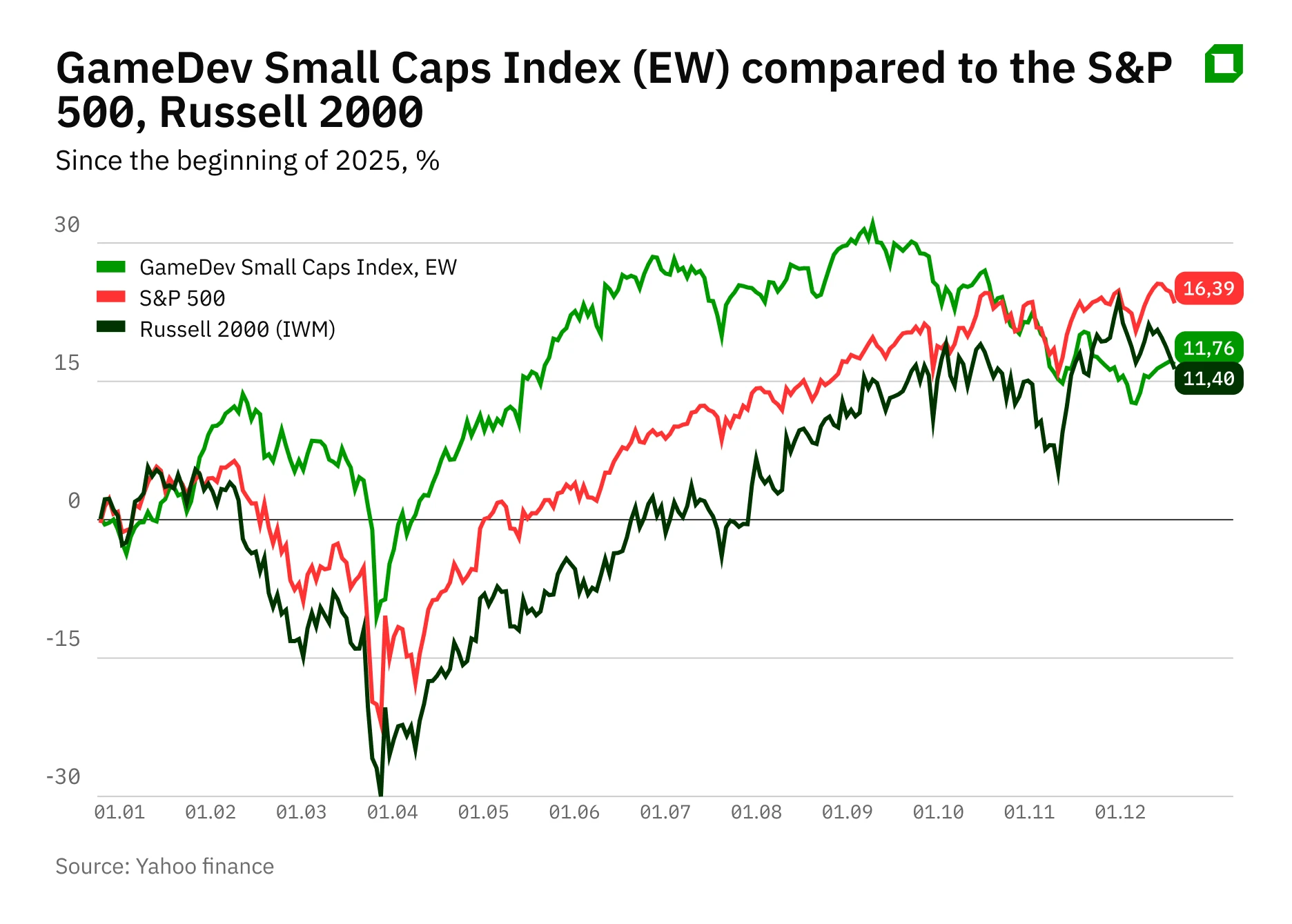

Analyst Aldiyar Anuarbekov calculated for Oninvest an equal-weight index of 80 small publicly traded game developers, the GameDev Small Caps Index. It rose 13% in 2025. For comparison, the broad smid-cap-tracking Russell 2000 gained 12% over the same period, while the large-cap S&P 500 advanced 16%.

At the same time, performance within the industry has been uneven. Growth has been driven primarily by Asian publishers. According to the October monthly report on the Chinese video game industry from Gamma Data, sales in China reached CNY31.4 billion ($4.4 billion) in October, rising 5.7% month over month and 7.8% year over year. The main drivers were in game promotions and the simultaneous release of projects on PC and mobile platforms, an approach that expands audiences and improves monetization.

At the opposite end of the spectrum are major Western studios. A prominent example is Ubisoft. Last year, the company’s shares fell 44% following delays to key releases and cautious revenue guidance. Analysts at UBS wrote in a report dated November 28 that one of the main factors weighing on the stock remains production delays for major titles and low visibility on the release calendar.

As a result, only 35 of the 80 companies in the GameDev Small Caps Index finished 2025 in positive territory. This underscores the highly fragmented and project specific nature of the gaming industry, where individual publishers’ results depend heavily on hit titles and sustained audience engagement. For investors, this implies the need for a targeted approach and careful selection of companies that can not only attract users but also retain them over the long term.

Sector ideas

For investors willing to track new game launches and closely evaluate studio financials, the sector continues to offer attractive opportunities, ranging from undervalued incumbents such as Ubisoft to fast growing developers operating in simulation, mobile, and indie gaming niches. Competition across the industry is intensifying, and release schedules, together with cash flow stability, are likely to drive future performance trends, Anuarbekov argues. He selected several companies investors should watch.

Frontier Developments

UK studio Frontier Developments (FDEV.L) specializes in games where you build things and manage them. Over the last 12 months, the company’s shares have risen more than 115%. Frontier successfully launched a new title in the Jurassic World franchise and confirmed development of a sequel to its best selling Planet Zoo. The company’s third Jurassic World game is scheduled for release before the end of fiscal 2026, which concludes in May 2026. In fiscal 2025, which ended May 31, 2025, Frontier reported a profit of GBP16.4 million ($20.5 million), versus a loss of GBP21.5 million ($26.9 million) a year earlier.

According to LSEG data, six of seven analysts rate the stock “buy” or “outperform,” while one analyst has a “hold” rating. The average target price is about 572.5 pence per share, implying roughly 22% upside versus current levels.

Ubisoft

France's Ubisoft (UBI) publishes hit franchises like Assassin’s Creed and Far Cry. Despite weak share performance over the last 12 months, during which the stock lost more than 40% of its value, the company reported stronger than expected sales in its latest earnings release. For the second fiscal quarter of 2025, ended September 30, net bookings reached EUR490.8 million ($540 million), up 39% year over year and above the management’s guidance of EUR450 million.

The management reaffirmed full-year revenue targets and announced plans to release several major titles in the coming months. Highly anticipated launches expected in early 2026 include a remake of Prince of Persia: The Sands of Time, a mobile version of Rainbow Six, and a new title set in The Division universe. The company also plans to release the Avatar: Frontiers of Pandora – From the Ashes expansion to coincide with the premiere of the new film.

While analysts remain cautious on the valuation, citing execution risks, the strategic value of Ubisoft’s portfolio remains substantial. With a market capitalization of about EUR840 million ($980 million), UBS estimates the company trades at roughly 0.5 times enterprise value/revenue and 0.6 times price/book value, versus historical levels in 2023 of about 2.0 and 2.7, respectively. Successful launches could help restore investor confidence. UBS analysts assigned a “hold” rating to the stock on November 28, cutting the target price to EUR7 per share from EUR10 per share. The revised target price now implies about 12.5% upside. The consensus analyst rating on Ubisoft shares remains “hold.”

Remedy Entertainment

Finnish studio Remedy Entertainment (REMEDY.HE) is preparing a remake of Max Payne 1 and Max Payne 2 in partnership with Rockstar Games. The project is in active production and, according to the management, could be released by the end of 2026. A weak launch, FBC: Firebreak, weighed on third quarter results and triggered a one-time write-down of EUR14.9 million ($16.4 million). In the third quarter of 2025, revenue fell 32% to EUR12.2 million ($13.4 million), while the operating loss widened to EUR16.4 million ($18.0 million), versus a profit of EUR2.4 million a year earlier. In October, Remedy made a management change and refocused its strategy on improving the commercial performance of its core franchises. Despite near term challenges, operating trends are stabilizing, supported by rising back catalog sales, including royalties from Alan Wake 2, and sustained demand for Control.

The stock is up about 16% over the last 12 months. The consensus analyst rating is “overweight.”

Shenzhen Bingchuan Network

China's Shenzhen Bingchuan Network (300533.SZ), which focuses on online and mobile games, was also among the strongest performers last year. The company’s shares have nearly doubled (up 94%) over the last 12 months. Bingchuan reported a profit of about CNY3.36 billion ($473 million) for the first half of 2025, versus a loss a year earlier, in line with the company’s guidance.

NHN Corp.

Another notable Asian player is South Korea’s NHN Corp. (181710.KS). Shares rose about 70% in 2025. In the third quarter, consolidated revenue reached KRW625.6 billion ($447 million), up 2.8% year over year, driven by growth in mobile games and payment services. Additional momentum came from the announcement of a new puzzle game, Oshi no Ko Match Star, based on the popular anime franchise Oshi no Ko and scheduled for release in 2026. Against this backdrop, analysts at Kiwoom Securities raised their target price to KRW37,000 per share and reiterated their “outperform” rating, implying roughly 20% upside.

This material does not constitute individualized investment advice.