Morning in New York: Middle East in the spotlight

The foreign policy agenda remains the key pressure on global markets / Photo: AustralianCamera / Shutterstock

Daily review and forecast of events on the U.S. stock market from Mikhail Denislamov, Deputy Director of Capital Markets Research, Freedom Broker.

We expect

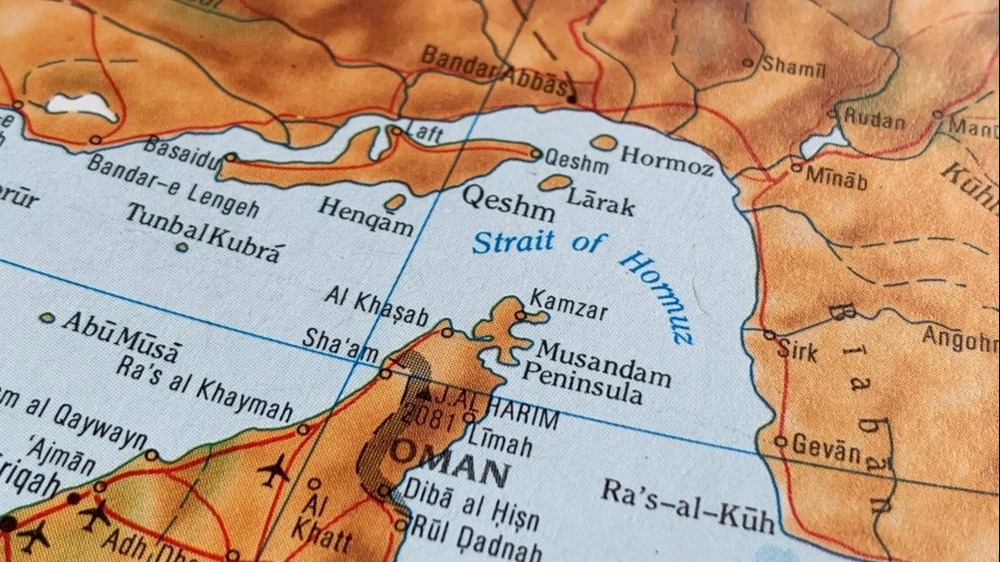

The foreign policy agenda remains the key pressure on global markets. Tensions around Iran and the Strait of Hormuz persist after reports of attacks on ships in the region and a port in the UAE. Also contributing to the escalation was U.S. President Donald Trump's statement that Iran would be "wiped off the face of the earth" in the event of attacks on U.S. ships providing security for shipping in the strait. At the same time, Washington continues to call on allies to join in securing maritime transportation in the region. Against this background, WTI crude oil is trading near $104 per barrel.

In the macroeconomic calendar this Tuesday, the most significant release will be the final assessment of the business activity index (PMI) in the service sector from S&P Global and ISM for April (consensus: 51.3 and 53.7 points, respectively). The forecast of Freedom Broker analysts assumes stability of the situation in the service segment and preservation of the index at the March level of 54 points.

JOLTS open job openings data for March (consensus: 6850k, February: 6882k) will also be released. Freedom Broker's benchmark is around 6870k, as the indicator has remained near average levels in recent months without a clear trend.

The speeches of Fed officials Michael Bowman and Michael Barr will be of interest to traders. In conditions of high oil prices and stable macro statistics, any signals of a tougher stance of the regulator may increase pressure on stock exchanges.

Pfizer (PFE), Shopify (SHOP), Eaton (ETN), PayPal (PYPL), Marathon Petroleum (MPC), KKR (KKR) and TransDigm Group (TDG ) will report before the main session opens. AMD (AMD), Lumentum Holdings (LITE), Strategy (MSTR), Arista Networks (ANET), Occidental Petroleum (OXY), Astera Labs (ALAB) and Super Micro Computer (SMCI ) will report quarterly results after the close of trading.

Futures on American stock indices demonstrate positive dynamics. We assess the balance of risks for the upcoming session as neutral with increased volatility against the backdrop of persisting geopolitical uncertainty.

The main thing on the pre-market

- Shares of Palantir (PLTR) are down about 3%, although adjusted EPS came in at $0.33 versus consensus of $0.28, and revenue reached $1.63 billion with an average guidance of around $1.54 billion. Given the strong demand for AI solutions, the company raised its 2026 revenue guideline to $7.65-7.66 billion with an average market guidance of $7.27 billion. The current correction is likely due to the high base of expectations after the stock's strong gains in previous quarters.

- Pinterest (PINS) stock soared about 16% after posting strong reporting and guiding revenue for the current quarter in the range of $1.13-1.15 billion with consensus around $1.11 billion. The company's Q1 revenue rose 18% YoY to $1.01 billion.

- Duolingo's (DUOL) quarterly revenue rose 27% YoY to $292 million and its paid subscriber base expanded 21%, but the company's stock fell nearly 13% amid a conservative booking volume forecast. Management's comments about shifting focus to expanding user base and engagement instead of accelerating monetization also put pressure on the stock.

- The announcement of the partnership with Anthropic caused Fidelity National Information Services (FIS) quotes to rise 5%. The companies are developing an AI solution for the banking sector that will be used to detect financial crime, including fraudulent transactions and suspicious transactions.

- Strong quarterly reporting and an increase in full-year guidance sent Sterling Infrastructure (STRL) shares jumping about 21%. The company's Q1 revenue increased 92% YoY to $825.7 million, and adjusted EPS was $3.59 with a consensus of $2.28.

- GeneDx (WGS) shares collapsed nearly 42% after the company lowered its 2026 revenue guidance from $540-555 million to $475-490 million from $540-555 million and released quarterly results that were weaker than market expectations.

- Shares of ON Semiconductor (ON) are down nearly 4% following the report, although the second-quarter earnings guidance was more optimistic than average market expectations and management noted signs of a gradual recovery in demand and the semiconductor sector emerging from a cyclical downturn.

The market on the eve of

Ma 4 trading on U.S. stock exchanges ended in the negative. Pressure on quotes was exerted by the new escalation of tensions around Iran and rising yields of U.S. Treasury bonds. S&P 500 lost 0.41%, Nasdaq 100 fell by 0.21%, Dow Jones fell by 1.13%, Russell 2000 fell by 0.6%.

The dynamics by sectors was mixed. The energy sector (XLE: +0.92%) was the leader of growth due to a sharp increase in oil prices. Materials producers (XLB: -1.36%) were the outsiders due to lower metal prices and worsening sentiment in cyclical segments.

The shares of the "Magnificent Seven" ended the trading mixed. Amazon (AMZN: +1.41% at the close of trading on May 4) looked much better than the market after the news of the launch of its logistics and supply chain management service for businesses. At the same time, Apple shares (AAPL: -1.18%) came under pressure: the starting price of Mac Mini was raised amid continued high demand for AI devices and current restrictions on component supply.

The key factor of pressure on the market were fears about the escalation of the conflict in the Middle East and the continued blockage of the Strait of Hormuz. Against this background, WTI quotes rose by 4.4%, and the yield on 30-year U.S. Treasury bonds exceeded 5%, returning to the maximum since July 2025. Negative impact on investor sentiment was also caused by the revision of expectations regarding the dynamics of the Fed's rates: the market again began to lay the probability of additional tightening of monetary policy before the end of the year.

Macroeconomic statistics turned out to be moderately positive. Orders of US industrial enterprises in March increased by 1.5% m/m with a consensus of 0.5%. FRB New York President John Williams noted that inflation expectations remain under control. At the same time, the U.S. Ministry of Finance raised its borrowing plan for the current quarter from $109 bln to $189 bln, which increased pressure on the government bond market.

Company News

-Global Business Travel Group (GBTG: +57.5% at the close of trading on May 4) will be acquired by investment firm Long Lake Management. The transaction involves a cash payment of $9.5 per share, which implies a valuation of the entire Global Business Travel Group at about $6.3 billion and corresponds to a premium of about 60% to the previous closing price.

-Celcuity (CELC: +15.4%) reported successful results from its Phase III trial of VIKTORIA-1. The company reported achieving the study's primary endpoint in patients with PIK3CA-mutated breast cancer, recording an improvement in progression-free survival.

-Coinbase (COIN: +6.1%) reported that it has reached a compromise on a key provision of the CLARITY Act related to the Stablecoin rewards mechanism.

-Norwegian Cruise Line (NCLH: -8.6%) lowered its earnings guidance for the current year due to higher fuel costs and weaker demand due to military action in the Middle East. In addition, management noted that bookings remain below the optimal range.

-FedEx (FDX: -9.1%) reacted negatively to Amazon's (AMZN) announcement that it will launch its Amazon Supply Chain Services platform for third-party companies. The new service combines freight, storage, full-field and delivery solutions. Against this backdrop, investors are wary of increased competition in the logistics sector.

This article was AI-translated and verified by a human editor