Oninvest looks at the top AI small caps in 1H26

An equal-weight index of AI small caps, calculated by Oninvest and comprising more than 40 companies, soared 26.5% in the first half of the year / Photo: Shutterstock.com

In the first half of the year, the AI rally extended well beyond the technology giants. Some of the biggest beneficiaries were small-cap companies operating across the AI infrastructure ecosystem.

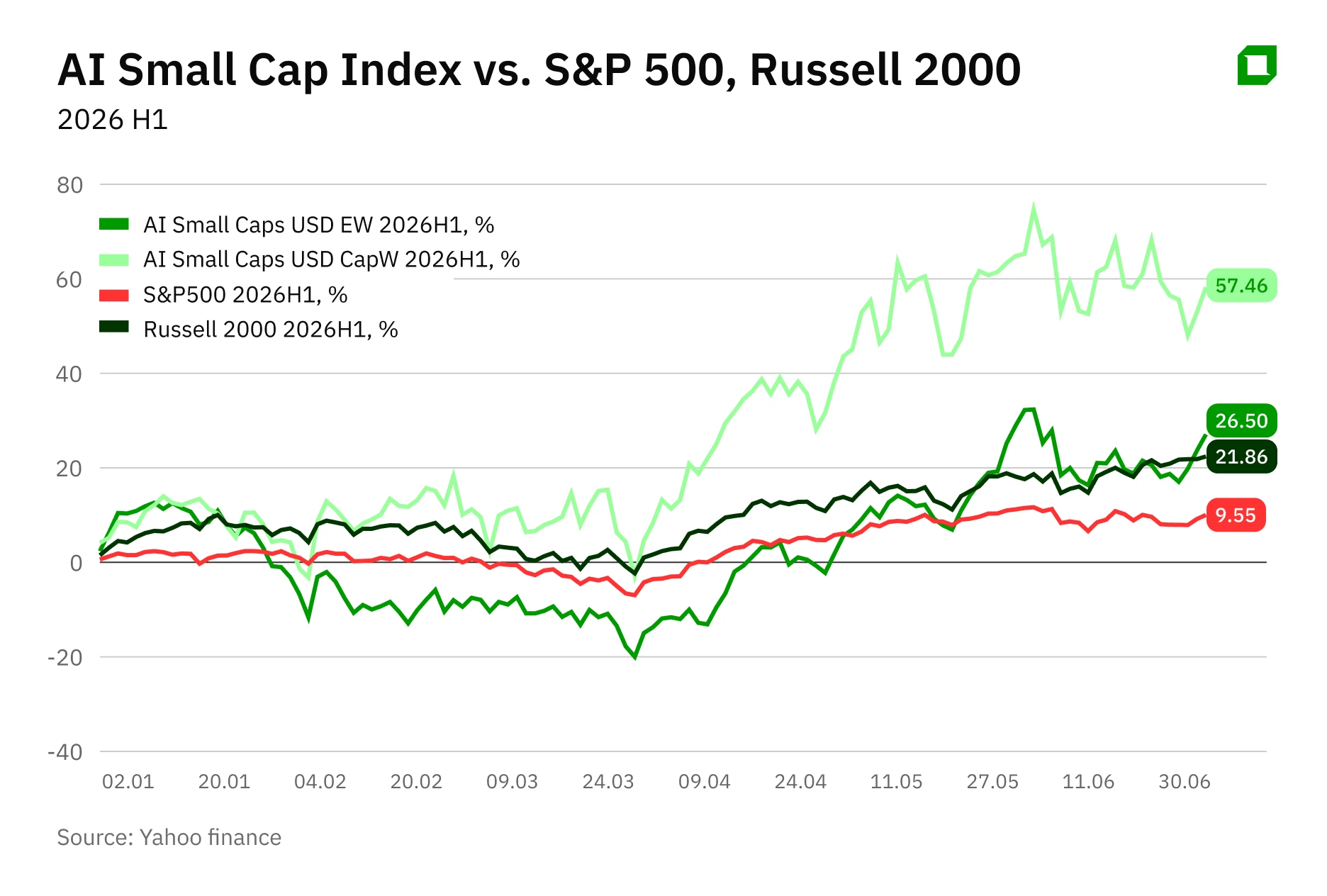

Oninvest has compiled equal-weight and cap-weight indexes tracking more than 40 AI-focused small caps. The equal-weight version gained 26.5% in the first half, while its cap-weight peer advanced 57.5%, outperforming both the Russell 2000 and the S&P 500. The Oninvest indexes' basket includes biotechs with generative AI drug-design platforms, semiconductor software developers, chip architecture licensors, and manufacturers of sensors, equipment, and components for data centers.

The rally was driven by more than a rerating of undervalued names. According to LPL Financial, fundamentals also improved markedly over the last six months, with the consensus forecast for 2026 earnings growth among Russell 2000 companies rising from about 23% to 38%. Investors have also become far more selective. Capital is increasingly flowing to companies where demand for AI solutions is already supported by contracts and revenue rather than driven solely by expectations.

Top performers

Within the Oninvest indexes, three companies stand out for having clear and verifiable growth drivers.

Absci (ABSI)

Absci is a biotech company that uses generative AI to develop new medicines. Its platform designs molecules for specific biological targets, while its in-house laboratory rapidly validates the most promising candidates.

In the first half of 2026, Absci was the best-performing constituent of the Oninvest indexes, with its shares gaining 221%. The primary catalyst was phase I results for ABS-201, the company's investigational treatment for androgenetic alopecia. On June 24, Absci reported that no serious adverse events had been observed among 32 volunteers and that the drug's estimated half-life was at least 65 days. That supports the potential for a patient-friendly dosing schedule of just two or three injections over a six-month period.

On the same day, Absci raised $100 million through a stock offering. Eli Lilly participated in the financing with a $40 million investment. Following the announcements, Absci shares surged around 36% in a single session.

The company's next key milestones include interim proof-of-concept data in the second half of the year, full study results in early 2027, and the launch of an ABS-201 trial in endometriosis scheduled for the fourth quarter. Around 80 million Americans suffer from androgenetic alopecia, and ABS-201 has the potential to become the first fundamentally new treatment for hair loss in almost 30 years. Today, the market still largely relies on minoxidil and finasteride.

The main risk is that ABS-201's efficacy has not yet been proven. Following the June data release, several houses have raised their target prices on Absci. H.C. Wainwright has increased its target price to $16 per share while maintaining its "buy" rating. It thus has one of the highest TPs in the market, implying 51% upside from the closing price on Friday. Morgan Stanley has also raised its TP to $10 per share from $4 per share while maintaining its "equal weight" rating.

Absci shares have gained around 200% year to date. According to MarketWatch data, the stock has nine "buy" calls versus one "hold" rating, with no "sell" recommendations.

PDF Solutions (PDFS)

PDF Solutions develops software for the semiconductor industry. Its Exensio platform integrates design, manufacturing, testing, and assembly data for semiconductors. According to the company, it is the only platform in the industry covering the entire chip development and production cycle.

In the first quarter, revenue increased 26% year over year to $60.1 million, while net income and earnings per share rose 56% and 48%, respectively. The order book also expanded 9% year over year to $246 million.

The main catalyst for the stock over the next year is expected to be shipments of the company's eProbe wafer inspection systems. PDF Solutions plans to ship six such systems in 2026, while Craig-Hallum estimates the addressable market at around $1 billion. Another potential catalyst is the planned third-quarter beta launch of the Exensio platform with AI capabilities.

The main risk is the company's dependence on a small number of major customers using leading-edge semiconductor manufacturing processes, meaning the loss of any one of them could materially affect financial results. Craig-Hallum has reiterated its "buy" rating with a $60 per share target price, while Northland has maintained its "buy" rating and $51.50 per share TP. However, the stock is already trading close to those levels, meaning further gains will largely depend on the success of eProbe sales.

The shares have about doubled year to date. According to MarketWatch data, all four analysts covering the company rate it "buy." The average target price is $62 per share, implying 12% upside from the Friday closing price.

CEVA (CEVA)

CEVA is one of the leading licensors of semiconductor intellectual property and Smart Edge technologies. According to the company, its technologies are used in more than 21 billion devices by over 400 customers worldwide. CEVA's core investment thesis centers on "physical AI" – devices that not only process data but also interact with the physical world.

In the first quarter, revenue increased 11% year over year to $27 million, while licensing revenue rose 18% to $17.8 million, its highest level in three years. Against that backdrop, the management raised its 2026 revenue growth outlook to the top end of its previously communicated 8-12% range.

One of the key growth drivers has been the start of mass production using CEVA technology in the 2026 Toyota RAV4, laying the foundation for long-term royalty growth. Another potential catalyst is Apple's transition to its own 5G modems. CEVA has said its technology is used in the modem of a leading U.S. smartphone manufacturer. While the company has not identified the customer, analysts believe it is referring to Apple and its C1 modem. Needham expects CEVA's royalty revenue to grow as the modem is adopted across new iPhone and iPad models.

CEVA CEO Amir Panush believes the industry is gradually approaching the limits of scaling cloud AI computing, meaning more computing workloads will shift directly onto devices.

Roth Capital has reiterated its "buy" rating with a $60 per share target price, implying around 30% upside from the Friday closing price. Meanwhile, Needham has initiated coverage with a "buy" rating and a $55 per share TP. Further gains will depend on whether the company can convert its new licensing agreements into a sustainable royalty stream and capitalize on the growth of physical AI.

The shares have gained around 112% over the first half of the year. According to MarketWatch data, Wall Street analysts have assigned the stock eight "buy" ratings versus one "hold" rating. The average target price is $48 per share.

Looking ahead

The semiconductor selloff at the end of June served as another reminder of how fragile the AI rally remains. Narrow market leadership and many companies' dependence on a small number of major customers continue to be the key risks. At the same time, two of the three stocks mentioned above have already approached Wall Street's average target prices. That suggests most of the valuation rerating is likely behind them, and future performance will now depend largely on whether the firms can turn expectations into tangible operating results.

This text is for informational purposes only and does not constitute personalized investment advice.