Oninvest Index: Top AI Small-Caps for the First Half of the Year

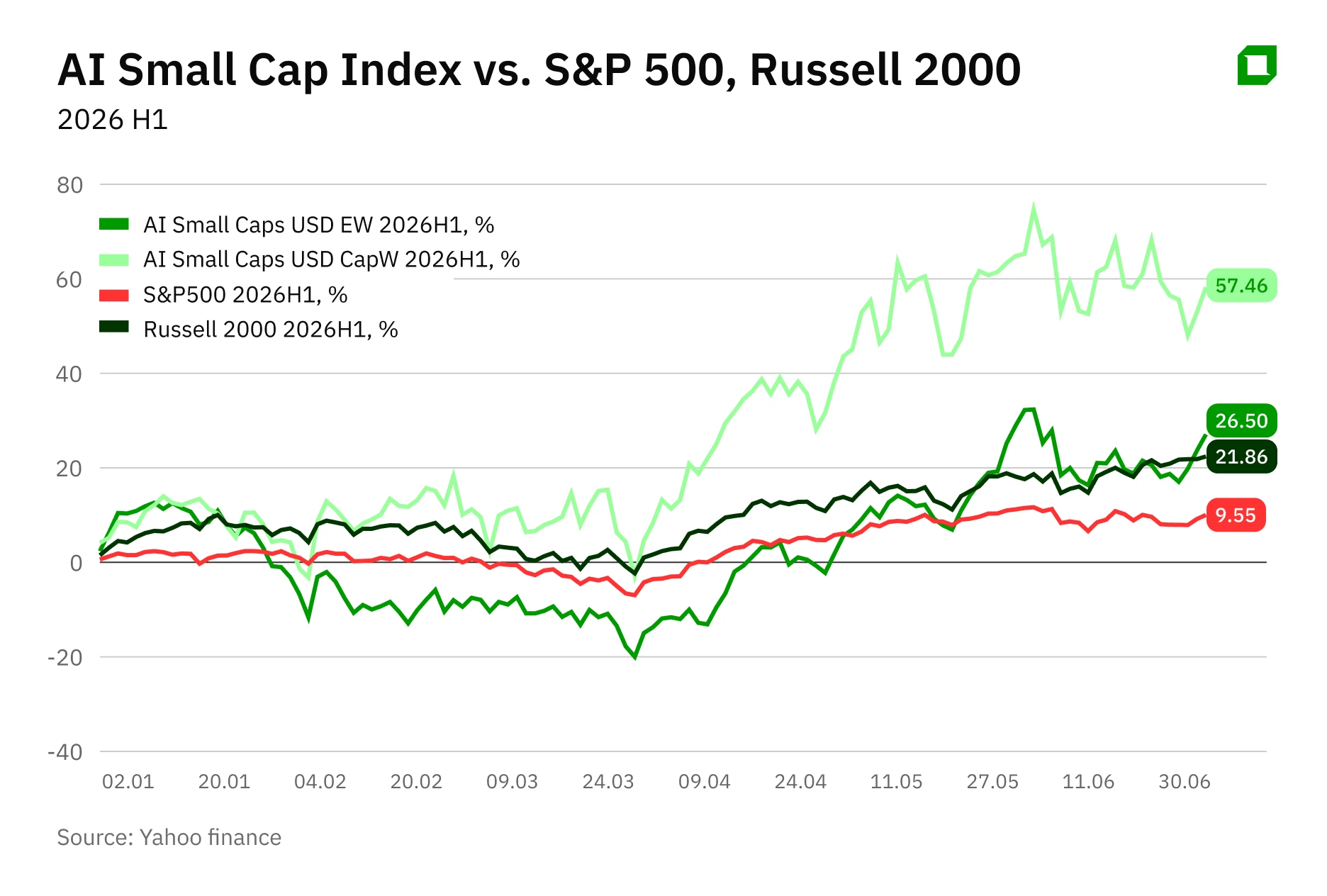

The AI Small Cap EW equally weighted index, calculated by Oninvest and comprising more than 40 companies in the AI sector, rose 26.5% in the first half of the year / Photo: Shutterstock.com

In the first half of 2026, growth driven by artificial intelligence extended beyond the tech giants. Some of the main beneficiaries were small-cap companies operating in the AI infrastructure sector.

The AI Small Cap EW equally-weighted index, calculated by Oninvest and comprising more than 40 AI-focused small-cap companies, rose 26.5% over the same period. Its market-cap-weighted version, the AI Small Cap CapW, gained 57.5%, outperforming both broad market indices. Oninvest’s sample includes biotech companies with generative molecular design platforms, semiconductor software developers, chip architecture licensors, as well as manufacturers of sensors, equipment, and components for data centers.

The growth is not solely due to the revaluation of previously undervalued companies. According to LPL Financial, fundamentals have also improved significantly over the past six months: the consensus earnings growth forecast for companies in the Russell 2000 Index for 2026 has risen from approximately 23% to 38%. At the same time, investors have become much more selective. Capital is increasingly being directed toward companies where demand for AI solutions is already backed by contracts and revenue, rather than being based solely on expectations.

Among the leaders of the Oninvest index, three companies were singled out for having clear and verifiable growth drivers—in the fields of biotechnology, semiconductor software development, and chip architecture licensing.

Absci (ticker symbol ABSI)

Absci is a biotechnology company that uses generative AI to develop new drugs. Its platform generates molecules for a given biological target, and its in-house laboratory quickly tests the most promising candidates.

In the first half of the year, Absci shares led the Oninvest index, rising 221%. The main driver was the results of the Phase 1 trial of ABS-201, a drug for the treatment of androgenetic alopecia. On June 24, the company reported that no serious adverse events were observed in 32 volunteers, and the drug’s half-life was at least 65 days. This suggests a patient-friendly treatment regimen requiring only two to three injections over the course of six months.

At that time, Absci raised $100 million in a stock offering. Eli Lilly was one of the investors, contributing $40 million. On the news, Absci’s stock surged nearly 36% in a single trading session.

Upcoming key milestones for the company include interim efficacy data for the drug in the second half of 2026, the publication of full study results in early 2027, and the launch of ABS-201 trials for endometriosis, scheduled for the fourth quarter of 2026. Approximately 80 million Americans suffer from androgenetic alopecia, and ABS-201 could become the first fundamentally new drug for treating hair loss in nearly 30 years. Today, the market continues to rely primarily on minoxidil and finasteride.

The main risk is that the drug’s efficacy has not yet been proven. Following the release of the June results, several analysts immediately raised their price targets for Absci shares. H.C. Wainwright raised its target price to $16 with a “Buy” rating—one of the highest targets for the company’s stock, implying a 51% increase from the closing price on July 10. At the same time, Morgan Stanley raised its target from $4 to $10 with an “Equal Weight” rating (market-neutral, recommend holding the stock).

Absci's stock price has risen by nearly 200% since the beginning of the year. According to MarketWatch, the company's stock has a total of nine "buy" ratings and one "hold" rating; there are no "sell" recommendations.

PDF Solutions (PDFS)

PDF Solutions is a software developer; its Exensio platform integrates data from the design, manufacturing, testing, and assembly of semiconductors. It is the only system in the industry that covers the entire chip development and production cycle.

In the first quarter of 2026, revenue rose 26% year-over-year to $60.1 million, net income and earnings per share increased by 56% and 48%, respectively, while the order backlog grew by 9% year-over-year to $246 million.

Deliveries of eProbe wafer inspection systems are expected to be the main driver for the stock over the coming year. The company expects to deliver six such systems in 2026, and Craig-Hallum analysts estimate the potential addressable market at approximately $1 billion. An additional catalyst could be the third-quarter launch of the beta version of the Exensio platform with AI capabilities.

The main risk is the company’s reliance on a few large clients that use cutting-edge technologies; therefore, the loss of any one of them could significantly worsen its financial results. Craig-Hallum maintained its “buy” rating with a price target of $60, while Northland recommended buying the stock with a target of $51.5. However, the stock is already trading near these levels, so further growth will largely depend on how successful sales of the eProbe systems turn out to be.

Since the beginning of the year, the stock has risen by nearly 100%. According to MarketWatch, the stock has four ratings, all of which are “Buy,” with an average price target of $62—12% above the closing price on July 10.

CEVA (CEVA)

CEVA is one of the leading licensors of intellectual property (IP) for semiconductors and smart edge devices. According to the company, its technologies are used in more than 21 billion devices across more than 400 customers. CEVA’s main focus is on “physical AI”: devices that not only process data but also interact with the world around them.

In the first quarter of 2026, revenue increased by 11% year-over-year to $27 million, while licensing revenue rose by 18% to $17.8 million—a three-year high. Against this backdrop, management raised its revenue growth forecast for 2026 to the upper end of the 8–12% range.

One of the main drivers was the start of mass production using CEVA technologies in the 2026 model year Toyota RAV4, which lays the foundation for long-term royalty growth. Additional potential stems from Apple’s transition to its own 5G modems. CEVA reported that its technology is used in the modem of one of the leading U.S. smartphone manufacturers. Although the company has not disclosed the manufacturer’s name, analysts believe it is Apple and the C1 modem. Needham expects CEVA’s royalty payments to grow as this modem is incorporated into new iPhone and iPad models.

CEVA CEO Amir Panush believes that the industry is gradually reaching the limits of scaling cloud-based AI computing, so more and more computing will be moved directly to devices.

Roth Capital maintained its “buy” rating with a price target of $60, roughly 30% above the closing price on July 10. Needham initiated coverage of the stock with a “buy” rating and a target price of $55. Further growth will depend on whether the company can convert its new licenses into a sustainable stream of royalties and capitalize on the development of physical AI.

Over the past six months, the stock has risen by nearly 112%. The company's stock has eight "Buy" ratings and one "Hold" rating from Wall Street analysts. The average price target is $48.

What's next?

The sell-off in the semiconductor sector in late June 2026 served as yet another reminder of just how fragile the AI rally remains. Narrow market leadership and the heavy reliance of many companies on a few large customers continue to be the main risks. That said, two of the three stocks reviewed have already approached analysts’ average price targets. This suggests that the bulk of the re-rating is likely already behind us, and future performance will depend on whether companies can back up their expectations with actual results.

This is not a personalized investment recommendation.