Oninvest military drone index outperforming small caps and broad market

The UAV industry is undergoing a structural shift: demand is moving away from one-off rush orders to formal, long-term procurement programs / Photo: parrot.com

At the end of last year, at the NATO summit in The Hague, members set a new benchmark: defense spending at 5% of GDP by 2035. Of that, at least 3.5% is to be allocated to core military needs, and up to 1.5% to resilience, innovation, and the development of the defense industrial base. In the U.S., this has translated into consistent regulatory policy: following a White House executive order in June 2025, the Pentagon in July moved to accelerate procurement and deployment of small drones for the military. In January, the new National Defense Strategy established countering drones as a priority. For the UAV industry, this marks a structural shift: demand is moving from one-off rush orders to formalized, long-term procurement programs. According to forecasts, the global UAV market will grow from $42.4 billion in 2026 to $261.3 billion by 2034, implying a CAGR of 25.5%.

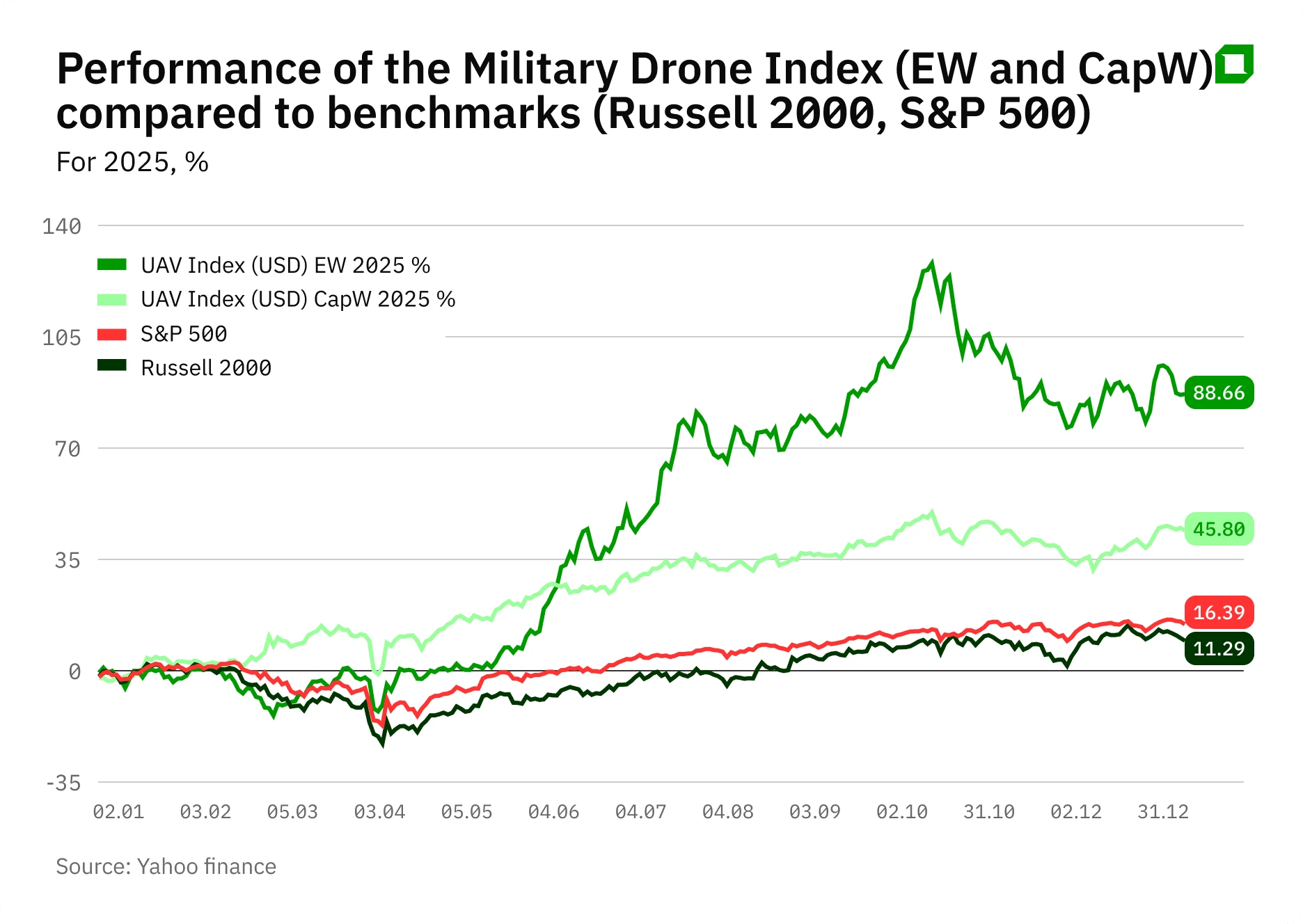

Performance of military drone index

In 2025, analyst Aldiyar Anuarbekov's equal-weight military drone index, put together specially for Oninvest, rose 88.7% (in dollar terms). The capitalization-weight version gained 45.8%. For comparison, the Russell 2000 index and the S&P 500 rose 11.3% and 16.4%, respectively, last year.

In 2026, the rally has continued: year to date, the equal-weight index has gained 17.2%, while the cap-weight one is up 6.8%. Over the same period, the Russell 2000 has risen 2.0%, while the S&P 500 is down 3.7%.

Investor interest in the segment is now driven by three factors at once: government policy, technological progress, and companies’ ability to rapidly scale mass production. A telling example: in December, the Finnish Defence Forces placed an additional order for Parrot Anafi UKR systems worth about EUR15 million, with deliveries starting in 2026. This signals a transition from the testing phase to repeat procurement and scaled deliveries.

Three stocks from the index

We selected three companies from the index that investors should watch: two of the strongest performers of 2025 – Red Cat Holdings and Ondas Holdings – and the early 2026 leader, Parrot. All three share a common investment thesis: the market is not paying for current earnings, but for the probability of entering the next defense procurement cycle. In that cycle, the key factors are the ability to scale serial production, access to government contracts, and resilient supply chains.

Red Cat Holdings

Red Cat (RCAT) focuses on small reconnaissance drones while simultaneously expanding its lineup of maritime unmanned platforms for U.S. military and government customers. According to its third-quarter report, revenue rose 646% year over year to $9.6 million, while gross profit totaled $0.64 million versus a gross loss of $0.39 million. Cash reached $206.43 million.

The key driver over the next 6-12 months is the transition from pilot deliveries to larger contracts. In early February, the company reported new orders for its Black Widow system from a second U.S. ally in the Asia-Pacific region, with deliveries scheduled for 2026.

Since the start of the year, Red Cat shares have more than doubled. According to Market Screener data, the company has four ratings, all “buy.” The average target price of $21.75 per share implies 37% upside versus the closing price on Wednesday. In March, Needham reiterated its “buy” rating and set a target price of $16 per share. Analysts say Red Cat is gradually moving beyond being viewed as a single-product manufacturer and is transforming into a player with solutions across both aerial and maritime unmanned segments. According to Needham, the key argument in the investment case is the company’s ability to rapidly scale production.

Ondas Holdings

Ondas (ONDS) develops autonomous surveillance and communications solutions for the military, security services, and critical infrastructure. Revenue in the third quarter increased more than eightfold year over year to $10.1 million, while gross profit reached $2.6 million versus $0.05 million a year earlier. Cash rose 14.4 times to $433.39 million. At the same time, operating cash flow for the first nine months remains negative: minus $26.02 million versus minus $25.36 million a year earlier. This reflects a typical growth-stage dynamic: the business is scaling rapidly but still requires significant investment.

The key near-term driver is the deal with Mistral. Under the agreement, Ondas gains access to a prime contractor role in Pentagon programs, while Mistral is already involved in U.S. Department of Defense contracts worth more than $1 billion. In addition, Ondas’ Optimus drone is included in the Blue UAS list, which simplifies and accelerates procurement by U.S. federal customers.

Ondas shares have risen nearly 10% year to date and more than 1,000% over the last 12 months. According to Market Screener data, the company has eight ratings, all “buy.” The average target price of $19.12 per share implies the stock could nearly double from current levels. Northland Securities in its latest report maintained an “outperform” rating on Ondas and a target price of $16 per share. Analysts say the Mistral deal strengthens Ondas’ position in the U.S. market and creates potential for additional growth beyond the current 2026 forecast.

Parrot

Parrot (PARRO) is a French manufacturer of small professional drones and the owner of Pix4D, a software solution for aerial imaging and mapping.

The company is expected to publish its full audited results for 2025 on Friday. In its fourth-quarter operating update, Parrot said revenue rose 10.6% year over year to EUR29.2 million ($34.4 million). For full-year 2025, revenue increased 2.2% to EUR79.8 million ($93.9 million). In the first half of 2025, the company reported a net loss of EUR14.7 million versus EUR10.1 million a year earlier.

Last year, the company sold more than 4,000 premium reconnaissance micro-drones. The main driver in the coming months is repeat military procurement in Europe. The key risk for the business is uneven tender timing: even with strong demand, revenue recognition may be delayed, extending the path to breakeven.

Parrot shares have risen about 30% year to date. Analyst coverage remains limited. Cantor Fitzgerald initiated on February 26 with an “overweight” rating and a target price of EUR11 per share, implying more than 10% upside from current levels. Analysts highlighted Parrot’s strong order backlog.

This material does not constitute individualized investment advice.

* The Oninvest index includes 22 companies. It comprises both major players like Lockheed Martin, Northrop Grumman, and Raytheon, as well as smaller companies focused exclusively on unmanned systems.