Likely additions and deletions to Russell 2000 as June rebalancing approaches

With more than $11 trillion in benchmarked assets under management, the Russell U.S. indexes serve as the benchmarks for many large asset owners and institutional investors / Photo: Unsplash / Kanchanara

The first semiannual Russell reconstitution will conclude at the end of June (see here on why it matters). Below we look at five companies that might join the Russell 2000, along with four likely candidates for deletion.

About Russell reconstitution

The Russell 2000, the main benchmark for U.S. small-cap companies, is moving to a new rebalancing format in 2026: FTSE Russell indexes will now be reconstituted twice a year, in June and December. Rank day, the date on which companies’ market capitalizations are measured to determine future index membership, took place on April 30. Preliminary lists of additions and deletions will be released on Friday, May 22.

More than $11 trillion in assets are benchmarked to Russell indexes, meaning any membership changes trigger significant capital flows from index funds and ETFs. According to Nasdaq, trading volume on reconstitution day last year exceeded $200 billion. Following the 2025 reconstitution, the breakpoint between the Russell 1000 and Russell 2000 remained around $4.6 billion market capitalization, while the smallest company in the Russell 2000 was valued at $119.4 million.

We analyzed the holdings of BlackRock’s iShares Russell 2000 ETF (IWM) and iShares Micro-Cap ETF (IWC) and identified 378 names that are present only in the micro-cap segment and absent from the Russell 2000. In addition, more than 130 companies currently in the lower tier of the Russell 2000 have market capitalizations below $180 million.

According to Nasdaq, inclusion in Russell indexes typically attracts new long-term investors and boosts stock liquidity for months afterward. The reverse is also true: deletion from the index can trigger forced selling by passive funds tracking roughly $2 trillion in assets.

We selected five likely candidates for inclusion in the index, along with four deletion candidates, based on current market data.

Likely incoming stocks

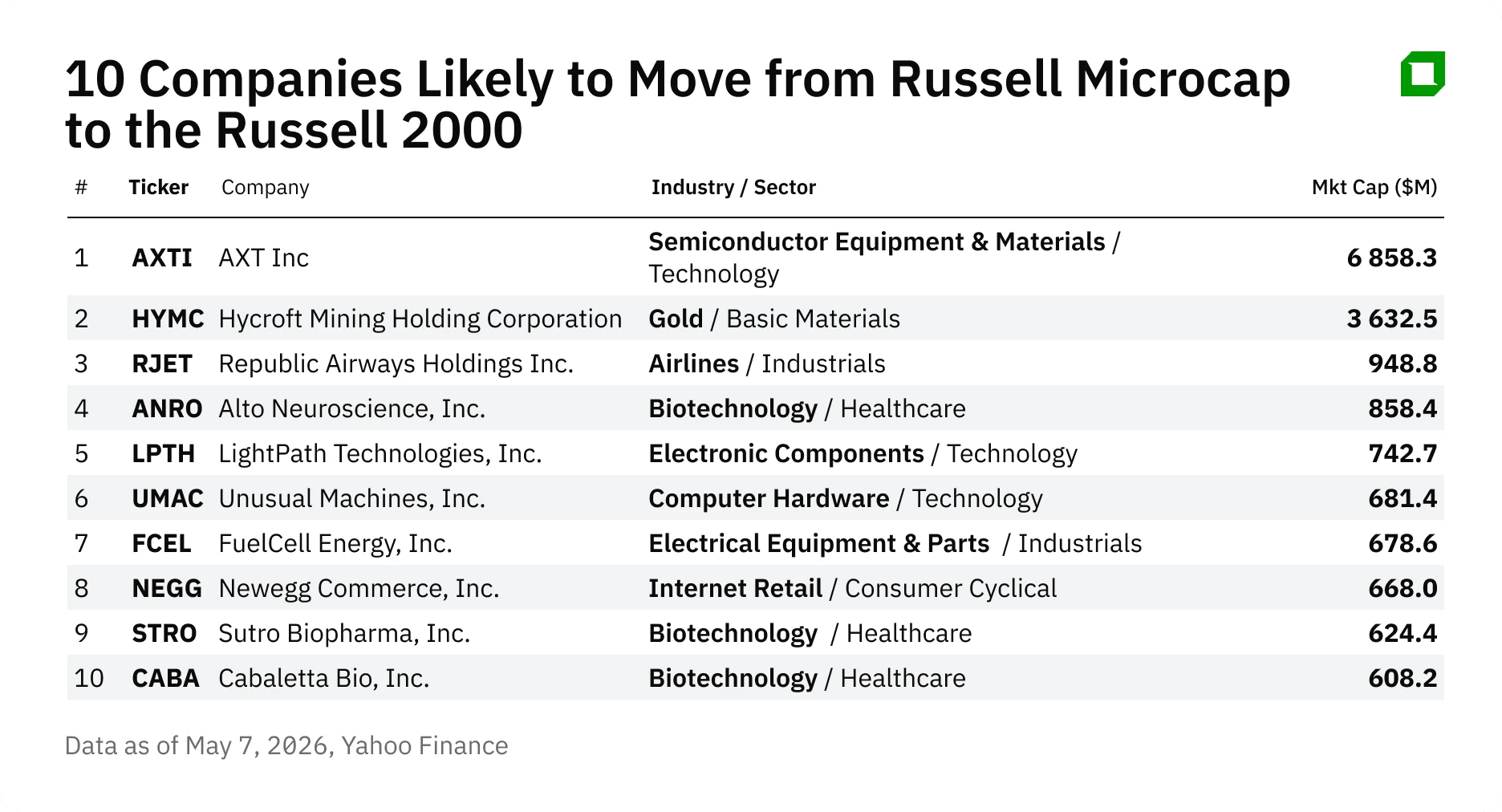

AXT (AXTI)

AXT, a producer of substrates for optoelectronics and data centers, has emerged as one of the market’s standout AI-related winners. Just a year ago, the company’s shares traded near $1 per share, but by May its market capitalization had climbed to roughly $8 billion – technically large enough to vault directly into the Russell 1000, bypassing the Russell 2000 altogether.

In the first quarter, AXT increased revenue nearly 39% year over year to $26.9 million. The adjusted net loss came in at $0.01 per share, versus the $0.04 per share net loss expected by analysts surveyed by Zacks. The order book topped $100 million amid strong demand tied to AI-related projects. In April, the company raised $632.5 million through a stock offering to expand production capacity.

On May 1, Wedbush Securities raised its target price on AXT to $93 per share from $80 per share and reiterated an “outperform” rating. B. Riley Financial increased its target to $73 per share from $72 per share while maintaining a “neutral” rating. The stock has already surged about 645% year to date and traded near $120 per share as of May 14. The main risk for investors is that, despite negative earnings over the last 12 months, the company continues to fund growth through equity offerings, diluting existing shareholders.

According to MarketWatch data, three Wall Street analysts rate AXT shares a “buy,” while three recommend holding them. The average target price is $81.20 per share.

Unusual Machines (UMAC)

NDAA-compliant drone component maker Unusual Machines has become one of the beneficiaries of the U.S. Drone Dominance program. The company doubled revenue in 2025 to $11.2 million. The gross margin expanded to 36% in the fourth quarter from 24% in the first quarter. The GAAP net loss totaled $19.2 million, though $15.7 million of that came from noncash stock compensation expenses.

Unusual Machines secured an order worth more than $5 million for counter-UAS system components and also entered into a partnership with Lantronix to develop autonomous drone components with onboard AI capabilities. Litchfield Hills analyst reiterated a “buy” rating with a $25 per share target price. The key risk is that the company remains unprofitable and continues to raise capital through equity offerings, diluting existing shareholders.

The company’s market capitalization stood at about $753 million at the beginning of May. According to MarketWatch data, the stock carries six “buy” ratings from analysts. The average target price is $24.30 per share, implying upside of nearly 60%.

LightPath Technologies (LPTH)

LightPath Technologies supplies infrared optics and thermal imaging systems for defense and commercial markets. In the third quarter of its fiscal 2026, revenue rose 109% year over year to $19.1 million. Gross profit increased 161% to $7 million, while adjusted EBITDA remained positive for a third consecutive quarter at $1.1 million. In February, the management unveiled a strategy aimed at generating more than $300 million in revenue within five years.

The company’s order book reached a record $110.6 million, up 196% from the start of the fiscal year. At its February investor day, the management outlined a strategy targeting revenue growth to more than $300 million over the next five years. Notably, Ondas Holdings and Unusual Machines invested $8 million in LightPath Technologies to support development of infrared solutions for the drone market.

LightPath Technologies has a market capitalization of about $760 million. On May 11, Canaccord Genuity reiterated a “buy” rating and raised its target price to $16.50 per share from $15.50 per share. Risks include a net loss of $16.4 million over the first nine months of the fiscal year, as well as a negative operating margin that persists as the business scales. According to MarketWatch data, LightPath Technologies carries four “buy” ratings. The average target price is $15.98 per share, implying 31.5% upside.

FuelCell Energy (FCEL)

FuelCell Energy, one of the pioneers of hydrogen power founded in 1969, is experiencing renewed investor interest amid surging electricity demand from data centers. The company is positioning its carbonate fuel cells as a distributed power solution, effectively competing with Bloom Energy.

In the first quarter, FuelCell Energy increased revenue 61% year over year to $30.5 million, while the order book stood at $1.17 billion versus $1.31 billion a year earlier. During the quarter, the company submitted commercial proposals totaling more than 1.5 GW of data center capacity and entered into an agreement with SDCL covering projects with combined capacity of 450 MW.

FuelCell Energy’s market capitalization stands at about $1.14 billion. In March, Wells Fargo lowered its target price on the stock to $6 per share from $7 per share and maintained an “underweight” rating. The bank noted that competitor Bloom Energy does not face manufacturing capacity constraints, while FuelCell Energy still lacks visibility into sustainable profitability. Risks include a gross loss of $5.9 million for the first quarter and a net loss of $26.1 million – the company remains deeply unprofitable.

The stock currently carries five “hold” ratings versus two “buy” ratings from Wall Street analysts. The average target price is $8.40 per share, implying about 60% downside.

Republic Airways (RJET)

Republic Airways is one of the largest regional airlines in North America, operating roughly 1,300 daily flights under the American Eagle, Delta Connection, and United Express brands with a fleet of 314 Embraer E175 aircraft.

In the first quarter, the company increased revenue 34% year over year to $527.4 million. Net income declined less than 1% to $26.9 million. Republic reaffirmed its guidance for approximately $2 billion in 2026 revenue.

At the end of last year, Republic Airways completed its merger with Mesa Air Group. Following the merger, Republic Airways Holdings became the owner of the world’s largest Embraer E-Jet fleet, with 310 aircraft, according to the company.

Republic Airways has a market capitalization of more than $1 billion. The stock is currently included only in the Russell Microcap Index, but at its current valuation the company comfortably fits within the Russell 2000 range. Republic Airways currently carries just one “hold” rating, as major investment firms do not yet cover the stock – something that could change after inclusion in the index.

Risks include heavy dependence on contracts with three airline partners, debt totaling $1.2 billion, and a sharp increase in jet fuel prices following the closure of the Strait of Hormuz.

Likely outgoing stocks

Hain Celestial (HAIN)

Hain Celestial, once one of the leading companies in the healthy food segment with brands including Celestial Seasonings and Earth’s Best Organic, has lost nearly 75% of its market value over the last year. The company’s market capitalization has fallen to $72 million. In the third quarter of Hain Celestial's fiscal 2026, net sales declined 13% year over year to $338 million. The net loss reached $106 million versus a net loss of $135 million a year earlier.

At the end of March, Nasdaq sent Hain Celestial a notice over noncompliance with the minimum $1 per share stock price requirement. Barclays maintained a “sell” recommendation, while Mizuho cut its target price by a third to $1 per share and maintained a “neutral” rating. Overall, Hain Celestial shares carry four “hold” ratings and one “buy” and one “sell.” The stock last closed at $0.80 per share on May 14.

Sleep Number (SNBR)

Sleep Number, the maker of adjustable-firmness mattresses whose shares traded above $12 per share as recently as February, has plunged to roughly $1.60 per share. The company’s market capitalization stood at about $37 million. In its 2025 annual 10-K report, the company disclosed substantial doubt about its ability to continue as a going concern. At the end of April, Sleep Number secured an emergency $55 million loan maturing on June 30 – effectively a temporary measure to support liquidity ahead of the sales season.

In May, Piper Sandler lowered its target price to $3 per share with a neutral recommendation, while UBS cut its target price to $2 per share, noting that the emergency $55 million loan expires at the end of June and that sources of new financing remain undefined. Sleep Number shares currently carry four “hold” ratings.

DocGo (DCGO)

The provider of mobile healthcare services and medical transportation faced a sharp 48% revenue decline in 2025 after losing its New York migrant-services contract: revenue fell from $617 million to $322 million.

However, the first quarter showed signs of a turnaround: revenue excluding migrant-related programs rose 19% year over year to $75.6 million. The management also raised its 2026 revenue guidance to $300-315 million, citing strong demand for SteadyMD virtual healthcare services.

The company’s market capitalization stands at about $58 million. Analysts at Canaccord Genuity lowered their target price to $1.00 per share from $1.50 per share while maintaining a “hold” rating. At the same time, Stifel maintained a “buy” recommendation but lowered its target price to $2.50 per share from $4.00 per share.

Bloom Energy (BE)

Bloom Energy, a producer of solid oxide fuel cells for distributed power generation for enterprises and data centers, also stands out. The company remains part of the Russell 2000, but its market capitalization has surged more than 1800% over the last year to $86 billion. That is roughly 17 times higher than the threshold for inclusion in the Russell 1000.

In the first quarter, Bloom Energy reported 130% year-over-year revenue growth to $751 million. Adjusted earnings came in at $0.44 per share versus a consensus forecast of $0.09 per share – 389% above expectations. The management also raised its full-year revenue guidance to a range of $3.4-3.8 billion. One of the catalysts was an expanded agreement with Oracle to supply up to 2.8 GW of fuel cell capacity for data centers. In April alone, the stock surged 109%, and during the rebalancing the company will almost certainly move from the Russell 2000 to the Russell 1000.