Which nuclear small caps have benefitted from AI-driven rising electricity demand?

Goldman Sachs projects spot prices to reach $91 by the end of 2026, indicating at least a 20% increase / Photo: Matthew G Eddy / Shutterstock.com

Shares of uranium miners significantly outperformed the underlying commodity market in 2025: the Sprott Uranium Miners ETF gained nearly 40% over the year. Against this backdrop, price dynamics in the global uranium market were more subdued: spot prices traded in the $63-83 per pound range, while long-term contract prices rose from $80 to $86 per pound. By the end of 2026, Goldman Sachs has projected spot prices would reach $91 per pound, driven by a uranium deficit that is expected to widen by nearly 12% to 1.914 billion pounds over the 2025-2045 period.

At the same time, the market remains volatile: as early as January, prices briefly exceeded $100 per pound, the highest level in more than two years. The start of the Iran war in late February triggered a correction, with spot prices returning to around $83 per pound by March. Speaking at the Bloor Street Capital Virtual Uranium Conference on March 28, John Ciampaglia said, “we've definitely had a cooling off, you know, as people have kind of stepped away and de-risked and taken money off the table in terms of not really knowing how this is all going to play out.” At the same time, he noted that “the longer term fundamentals, the story remains very intact. And we would argue that this recent energy crisis, no matter how long it lasts, is another positive development, longer term for uranium and nuclear energy.”

Which nuclear stocks led last year

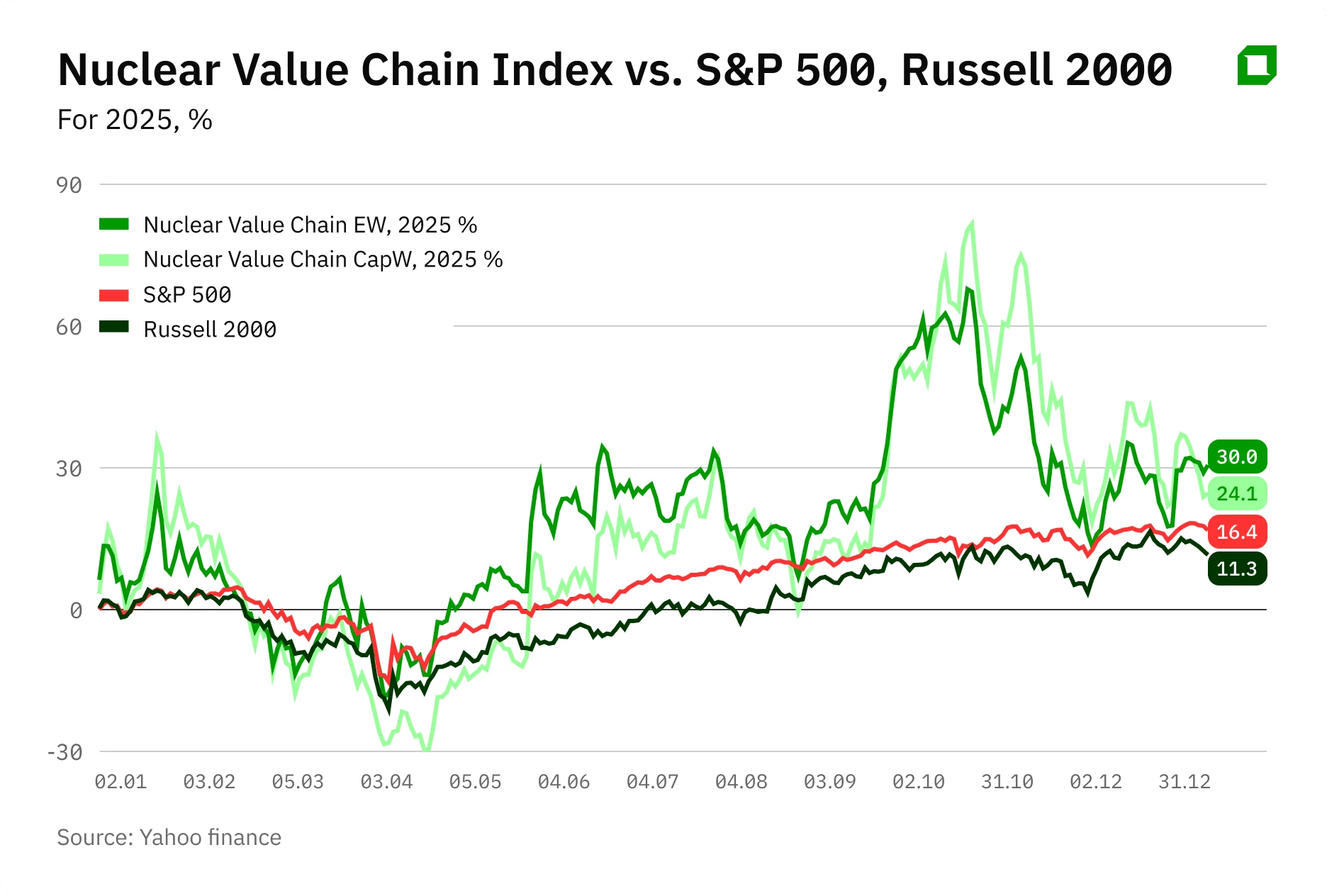

For 2025, the equal-weight version of an index comprising 18 smid-cap companies in nuclear infrastructure, made for Oninvest by analyst Aldiyar Anuarbekov, gained 30%. The cap-weight version of the index rose 24%. The difference in returns suggests that gains were broad-based and not limited to a narrow group of large players.

Among the top performers in the index in 2025 were Lightbridge Corporation, which returned 147.8%, Silex Systems with 83.3%, and Elevate Uranium with 24.5%.

In the first quarter of 2026, leadership rotated toward exploration-stage companies: Alligator Energy gained 57.0%, Western Uranium & Vanadium Corp. rose 29.3%, and Forsys Metals added 23.1%. At the same time, last year’s leaders corrected: shares of Lightbridge fell 25.6%, Silex Systems declined 38.7%, and Nano Nuclear Energy dropped 26.9%. Such volatility is typical for the sector, where project development milestones and news flow can quickly reshape the competitive landscape.

Leaders of the index YTD

All three leading companies share a key factor: they are on the verge of transitioning from the exploration and development stage to operations or initial revenue generation. The realization of their potential largely depends on uranium prices – according to Sprott Asset Management, long-term prices need to remain at no less than $100 per pound for new projects to remain economically viable.

In the long term, the sector outlook remains positive: according to the World Nuclear Association, global nuclear capacity could increase from the current 398 GW to 746 GW by 2040. At the same time, such an investment case is suited to investors willing to accept elevated volatility in exchange for potentially high growth in a sector receiving significant policy and investment support.

Alligator Energy

Alligator Energy (ASX: AGE) is focused on the Samphire project in South Australia, with a resource base of about 18 million pounds of uranium and targeted production of 1.2 million pounds per year over 12 years. In early 2026, the project entered a key phase: a pilot plant was completed in February, and field trials began in March, delivering initial positive results – uranium-bearing solution is being processed.

The company remains in the investment stage: for the financial half-year ended December 31, Alligator Energy reported a net loss of AUD4.96 million ($3.3 million) versus AUD1.47 million ($970,000) a year earlier, with AUD3.51 million ($2.3 million) related to discontinued operations following the sale of Northern Australia assets. As of December, cash stood at about AUD21 million ($13.8 million), providing financial flexibility to execute current programs.

Analysts at Bell Potter Securities on March 27 assigned the stock a speculative “buy” rating with a target price of AUD0.07 per share, implying upside of about 90%. The key risk lies in the transition from pilot to commercial production – it is at the scaling stage that technological challenges may arise, potentially affecting timelines and project economics.

Western Uranium & Vanadium Corp.

Western Uranium & Vanadium Corp. (CSE: WUC) focuses on high-grade uranium and vanadium production in Colorado and Utah. Its core asset is the Sunday Mine Complex in the Uravan belt, one of North America’s richest uranium regions. In April 2025, the company signed an agreement with Energy Fuels to supply ore for processing at the White Mesa Mill – the only operating conventional uranium and vanadium mill in the U.S. According to CEO George Glasier, “this Agreement strengthens Western’s strategic position and accelerates our generation of revenues.”

At the same time, the company is developing its own infrastructure: in October, it raised funding for the Mustang processing project and drilling at the San Rafael site. In December, Western announced a share buyback program for 6.67 million shares, or about 10% of the free float. In early 2026, Glasier purchased 100,000 shares on the open market, increasing his stake to 7%. For the first nine months of 2025, the company reported its first revenue from ore sales at $297 thousand. The net loss for the period totaled $5.8 million, down 23% year over year. Cash declined 41% year over year to $3.2 million.

Analysts at HoldCo Markets in March set a target price of CAD0.55 per share, noting a lack of operational updates on the Energy Fuels agreement following initial deliveries, while the stock currently trades at CAD0.79 per share. Alliance Global Partners in August assigned a “buy” rating with a target price of CAD4.00 per share, implying upside of about 400%. The main risk is revenue dependence on a single agreement with Energy Fuels, as well as uncertainty around the timing of licensing for the company’s own processing facility.

Forsys Metals

Forsys Metals (TSX: FSY) is developing the Norasa project in Namibia, one of the key countries in the global uranium market. The asset combines the Valencia and Namibplaas deposits, with total resources of about 88 million pounds. In October, the company raised nearly CAD19 million to advance the Valencia project, and in January published drilling results confirming high uranium grades.

From a valuation perspective, the company appears undervalued: according to its own estimates, the stock is trading at a discount of about 73% to the sector’s average EV/resource multiple. With a market capitalization of about CAD88 million and no debt, Forsys retains financial flexibility, although it remains outside of the focus of major investment banks. The key risk is the need to raise additional funding to transition to the mine construction stage.

This material does not constitute individualized investment advice.