Risks for a neobank: Can Revolut Reach a $200 Billion Valuation?

Revolut has set a goal of becoming a global bank with a valuation of $150–200 billion. Photo: Veja / Shutterstock.com

Revolut’s IPO is one of the most anticipated events on the European stock market. It may not take place until 2028 at the earliest. What should investors be paying attention to right now, and what risks might Revolut face?

New Terms and Conditions

Revolut co-founder Nikolai Storonsky first mentioned a possible IPO back in 2021. At the time, he did not provide a specific timeline or financial target, other than the need to generate “several billion dollars” in revenue per year. In 2020, Revolut’s adjusted revenue totaled 261 million pounds ($359 million), while its operating loss doubled to 201 million pounds ($280 million).

But since 2023, the fintech company has been consistently profitable. At the end of 2025, Revolut’s total revenue reached a record 4.5 billion pounds ($6 billion), and its net profit was 1.3 billion pounds ($1.7 billion).

Storonsky now says the IPO will not take place until at least 2028. He has set a new goal for Revolut: to become a global bank with a valuation of $150–200 billion by the time it goes public.

In the most recent secondary share offering in November 2025, the fintech company was valued at $75 billion. This means Revolut plans to at least double its valuation.

This year, Revolut may conduct a secondary offering—at a valuation of $115 billion. The Nasdaq Private Market states that only institutional or accredited private investors will have access to shares in Revolut’s secondary offering. They must meet strict SEC criteria. For example, they must demonstrate an annual income of $200,000 (or $300,000 jointly with a spouse) for each of the previous two years, or have a net worth of $1 million, excluding the value of real estate used as their primary residence.

Is the new goal achievable?

The icing on the cake

Revolut currently serves 75 million customers in 160 countries worldwide, but holds a full banking license in only 30 of them. By 2030, it aims to expand its licensed operations to 100 countries and serve more than 100 million customers. That is why the bank is actively expanding its business right now. The large user base that Revolut is actively building will add value to its valuation, says Valeria Ishkova, a corporate client specialist at JPMorgan.

In the United Kingdom, where Revolut is headquartered, the fintech company finally obtained a full banking license this year after several years of waiting and scrutiny. In June 2026, it announced its entry into the UAE market. It has already obtained full banking licenses in Mexico and Colombia, filed an application in Peru, acquired a bank in Argentina, and entered the Brazilian market. By 2028, the fintech startup plans to launch in South Africa. Previously, it reported that it was preparing to launch in India, opening a tech hub in the Philippines, and applying for banking licenses in Australia and New Zealand. In addition, it is in talks to acquire the digital bank FUPS in Turkey and to enter the Moroccan market.

This year, he expects to receive a license from the French regulator. Operating under the supervision of the central banks of France, the United Kingdom, or Germany could make it easier to obtain a license in the United States, Storonsky explained.

In the U.S., Revolut also expects to receive a license as early as this year. Gaining a foothold in this country is a major challenge for any fintech company, BCG analysts warn. The local market is crowded with established players, the percentage of the population without access to banking services is low, costs are high, and regulation is complex—due to differences in state laws and the large number of regulators.

Revolut has been operating in the U.S. since 2020 through partner banks, using their licenses—it offers its product to the banks’ customers but does not hold deposits on its balance sheet or issue loans. In 2021, the fintech company began the process of applying for a license but did not complete it, as it decided to acquire an existing bank. However, it abandoned that idea as well—due to the requirement to maintain physical branches, which was incompatible with its digital model, and regulatory complexities.

In March 2026, Revolut applied for a license in the U.S. According to FT sources, the neobank hopes for a swift approval process thanks to the U.S. administration’s more lenient approach to regulation. U.S. President Donald Trump announced earlier this year that he would ease requirements for fintech companies and foreign banks. The license will give Revolut access to the Federal Reserve’s payment infrastructure; it will also allow the company to offer loans and issue credit cards in the U.S. market.

Without a U.S. license, Revolut will be missing the “icing on the cake.” It is precisely this license that will secure it entirely different terms for its listing, enhance its reputation, and raise investors’ expectations.

Under the hood of the record-holder

"Great companies start with their metrics," write analysts at Andreessen Horowitz about Revolut's financial results (the venture capital firm participated in the neobank's most recent secondary share sale).

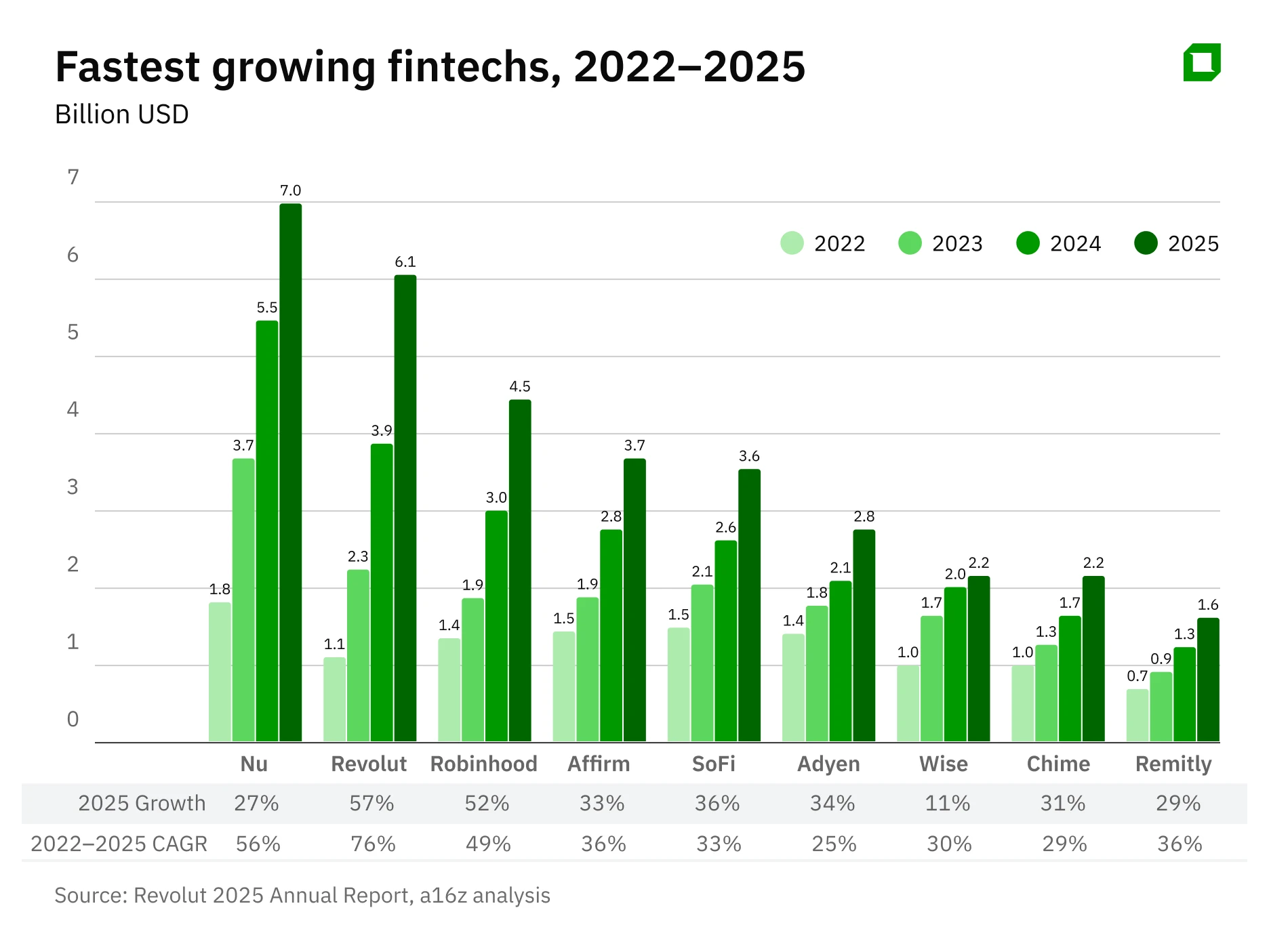

Andreessen Horowitz applies the so-called "Rule of 40" to Revolut, a metric that evaluates the performance of companies—primarily in the SaaS industry—and shows how a company balances profitability and growth rates (calculated as the sum of revenue growth and profit margin growth). For 2025, this metric stands at 75% for Revolut, which is significantly higher than that of its competitors, according to analysts at Andreessen Horowitz. In 2022, Revolut’s revenue was lower than that of Robinhood, Affirm, SoFi, Adyen, Wise, or Chime. Now, however, it exceeds that of each of them, they point out.

If Revolut can maintain this pace of growth, a valuation of $150–200 billion at its IPO in two years’ time would be more than justified, Ivan Tikhononenko believes.

Analysts at Andreessen Horowitz note that it is important that Revolut is no longer a fintech company with just one “selling point.” In 2015, that selling point was prepaid cards with the ability to instantly exchange currencies at the interbank rate. Now, according to Revolut’s press release and financial reports, all of its key business segments have grown over the past year: revenue from subscriptions—up 67%, from the business division—up 53%, from the card business—up 45%, from currency exchange—up 43%, and from wealth management—up 31%.

However, 76% of its revenue still comes from fee income, while interest income accounts for just under 22%. This is an atypical situation for a traditional bank, where 70% of revenue comes from interest income, according to analysts at Andreessen Horowitz.

This is partly due to Revolut’s established reputation as a convenient bank for currency exchange and payments. And partly by the nature of its business: at the end of 2025, Revolut’s loan-to-deposit ratio was only about 6%, compared to 70–90% at traditional banks.

The neobank's total customer deposits grew by 66% in 2025, reaching $67.5 billion, while its loan portfolio, although it increased by 120%, grew to only $2.9 billion.

Revenue from currency exchange, card payments, and cryptocurrency services is cyclical and depends on market conditions, according to analysts at the Insights4VC research project (which specializes in digital asset markets, Web3 technologies, and venture capital investments).

According to its financial statements, Revolut’s net interest income is primarily generated from the placement of liquidity: government bonds, securitized assets, swaps, and so on. However, the capital and funding reserves—approximately $6.6 billion as of the end of 2025—appear to provide a solid foundation for expanding lending activities, according to Oninvest analyst Aldiyar Anuarbekov.

Lending is just one of many product lines, currently available in only 13 markets where the company holds a license for this service, a Revolut spokesperson told Oninvest. The neobank’s revenue is diversified across payments, subscriptions, foreign exchange transactions, asset management, and trading, as well as interest income from deposits and loans in both established and new markets, he added.

Even Andreessen Horowitz acknowledges that Revolut is not yet fully leveraging its credit potential. However, its relatively low interest income, combined with low costs, ensures a high return on equity (ROE) of 35%.

At the end of 2025, Revolut’s ROE was significantly higher than that of leading fintech companies and roughly 3 to 4 times higher than that of established banks, Andreessen Horowitz adds. If Revolut’s ROE remains high, this will help ensure a high valuation at its IPO.

Revolut's Main Risks

Most analysts whose reports Oninvest reviewed or with whom it spoke in person consider regulatory risks to be Revolut’s main challenge. It needs to adapt to the requirements of central banks in different countries, balancing expansion with high anti-money laundering standards and compliance with all sanctions regimes.

Revolut’s rapid growth has already drawn the close attention of regulators, according to analysts at Insights4VC. In 2025, the Bank of Lithuania fined Revolut’s European subsidiary €3.5 million for violating anti-money laundering requirements. British regulators long delayed granting the fintech company a full banking license, expressing doubts about the quality of its cross-border risk controls.

"Whether Revolut's anti-money laundering management and compliance systems will scale in line with the company's growth remains to be seen," write analysts at Insights4VC.

Operating under a variety of regulatory regimes is not a risk unique to Revolut; this is how any banking group operates, a spokesperson for the neobank told Oninvest. According to the spokesperson, Revolut actively invests in local governance and oversight in each market and recruits top management with in-depth knowledge of local conditions.

The second group of risks is related to future growth in lending. As long as loans account for a small portion of Revolut’s balance sheet, investors will view it as a fintech company, evaluating its user base, technology, and ability to scale, says Valeria Ishkova. But as soon as lending begins to grow, traditional banking “metrics”—capital adequacy, reserve quality, liquidity, and funding stability—will come to the forefront.

At the same time, Revolut’s credit risks may increase, as it plans to expand its lending operations, including in markets with high levels of informal employment and a weak legal framework for debt collection. Mexico is one such example. In the local market, delinquency rates reach 15–27% of outstanding loans among customers employed in the informal sector, and even when lenders manage to collect the debt, they do so at a 30–50% discount, according to Oninvest.

“We maintain a prudent approach to lending, scaling our operations accordingly. Our loan portfolio has grown to 2.2 billion pounds ($2.9 billion)—more than double the previous year’s figure—while our expected coverage of credit losses has remained at the same level,” a Revolut spokesperson said.

Ivan Tikhonenok believes that clients’ lack of financial discipline is a problem for any market: “It all depends on the company’s own risk policy—on how much risk it is willing to take. Banks can go bankrupt in Europe and thrive in emerging markets.”

Revolut faces a truly challenging task: to maintain its fintech appeal while transforming into a traditional bank, so that it can command the industry’s high valuation multiples.

Finally, the last group of risks relates to maintaining the fintech industry’s appeal to investors. This sector is already overheated, and new players are constantly entering it, notes Ivan Tikhonenok. In his view, competition here will only intensify in the near future, while investor interest, on the contrary, may decline.

Storonsky himself, when discussing the IPO, also made a caveat regarding favorable conditions: the timing would “depend on market conditions.”

This article was AI-translated and verified by a human editor