Eight years under pressure: the three trials of Jerome Powell

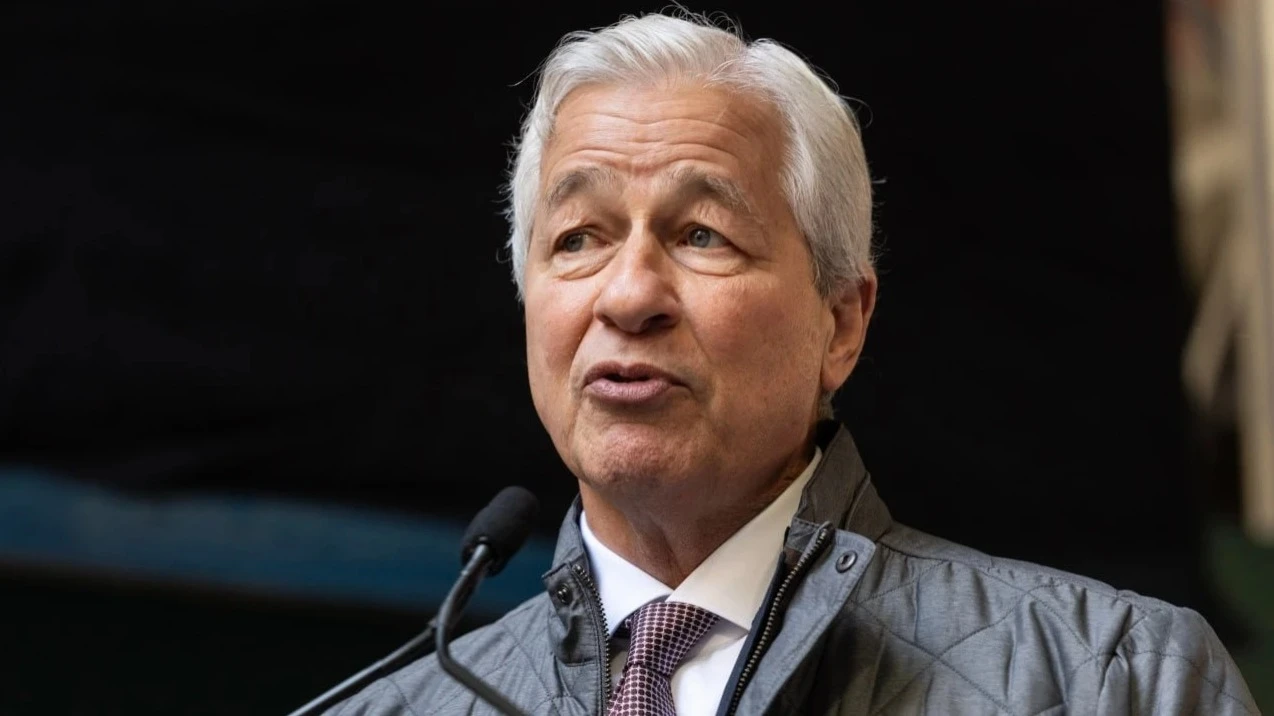

Jerome Powell leaves his successor to deal with high inflation, which has accelerated to a three-year high of 3.8% over the past 12 months / Photo: Al Drago/Getty Images

Today, Ma 13, the U.S. Senate is expected to confirm Kevin Warsh as Fed Chairman. His predecessor Jerome Powell led the Fed in 2018 with the S&P 500 index at 2,650 points and a benchmark interest rate of 1.25-1.5%. In May 2026, the index is above 7,400 points and the Fed's key rate is in the 3.5-3.75% range. In those eight years, the Fed chief has had to make decisions in the face of a pandemic, the worst spike in US inflation in four decades, a banking crisis and unprecedented political pressure from the man who nominated him for the post. Ekaterina Komarova wrote about Jerome Powell's three challenges

Volmageddon

On February 5, 2018, the fear index, the Cboe Volatility Index (VIX), rose over 100% for the day. The Dow Jones Industrial Average Index flew down 4.6%, recording at the time the largest drop in points in its history. Investors lost money - as it was later calculated that the losses for one day amounted to almost $2 billion. The day, which financial experts and brokers would later call "Volmageddon", was Jerome Powell's first working day as Chairman of the Board of Governors of the U.S. Federal Reserve System. Volmageddon had no serious consequences for the economy, becoming only a symbolically hard start for Janet Yellen's successor.

Major mistake: COVID-19 and its consequences

The real test for the Fed chief began in the pandemic. COVID-19 completely changed the trajectory of the Fed's monetary policy, forcing the U.S. Central Bank to take radical measures. One of the major decisions during that period was to cut the prime rate to almost zero. The Fed also resumed its quantitative easing (QE) program, buying assets - about $80 billion of government bonds and $40 billion of mortgage-backed securities per month.

We've crossed a lot of red lines. This is exactly the kind of situation where you do it first and then deal with the consequences.

All these measures allowed the US to avoid a second Great Depression: the recession caused by the pandemic was the shortest for the US - it lasted only two months - and the economy recovered faster than other G10 countries.

However, COVID-19 was not without complications for the Fed. Until 2020, the main problem for the regulator remained too low inflation - it was unsuccessfully tried to "pull up" to the target 2% per year. But large-scale fiscal stimulus worth trillions of dollars accelerated price growth in 2020 and 2021 to dangerous levels. And here the Fed made a major mistake: inflation was perceived as a temporary phenomenon, so it was not responded to in time. As a result, by June 2022, it reached 9.1% - a figure that the U.S. residents have not seen since 1981.

However, according to Hong Tran, a former IMF deputy director, now an analyst at the Atlantic Council's GeoEconomics Center, the problem was not that high inflation was simply "missed". The mistake was in the Fed's new strategy, which was adopted in the spring of 2020. It assumed flexible targeting of average inflation (FAIT). The Fed allowed prices to rise above the 2% target if inflation remained low for a long time before that. According to experts, the strategy was not bad in itself, but it was not suitable for such an extraordinary situation as a pandemic. The U.S. Central Bank realized this too late.

Ultimately, the Fed was forced to abandon FAIT and revert to its traditional inflation targeting approach, a prime example of closing the stable door after the horse has run away.

"In hindsight, the Fed was indeed slow to respond to inflation at the outset, but there is no denying that once the tightening cycle began, it moved to one of the fastest pace of rate hikes in history." said Stefan Cates, a financial analyst at Bankrate.

The rate of increase was really impressive: from March to December 2022, the key rate rose from 0.25% to 4.5%. However, even here it was not without negative consequences.

Banking Crisis 2023

The Fed's actions triggered a major crisis in the banking industry. It began in March 2023 with the collapse of Silicon Valley Bank (SVB), which served about half of all technology and biotechnology companies in the United States.

In terms of assets ($209 billion), it was in 16th place. By 2022, 94.4% of deposits were placed in long-term HTM securities - in particular, in government bonds and mortgage-backed securities.

The sharp rise in the interest rate led to two things at the same time: the value of these securities fell, and the bank found itself with large unrealized losses. And the bank's customers, frightened by the Fed's actions, began to withdraw their deposits en masse.

As a result of accelerating outflow of funds, SVB faced liquidity shortage and was closed by regulators. Following SVB, two other credit institutions - Silvergate Bank and Signature Bank - closed down.

And on Ma 1, 2023, First Republic Bank announced it would cease operations. Like SVB, First Republic was a niche bank from California. And just like SVB, it experienced a sharp outflow of deposits(to the tune of $100 billion - more than 40% of all deposits) as a result of customer panic. The collapse of First Republic, with its $213 billion in assets, moved SVB from second to third place in the ranking of the largest bank failures in U.S. history.

In total, 22 credit organizations reported about sharp outflow of deposits in that period.

As calculated by American Forbes, 2023 was not a record-breaker compared to 2008-2013 in terms of the number of failed credit institutions, but it broke all historical records in terms of total assets that were on the accounts of failed banks.

And yet a major crisis was avoided, thanks in large part to the Fed's quick action, says Tim Sablik, an economic analyst at the Richmond Fed. After the collapse of the SVB on March 10, the regulator sharply increased emergency lending to banks through the discount window. And on March 12, the Fed launched a new support program, the Bank Term Funding Program (BTFP), under which it was possible to borrow against government bonds and other safe assets.

"Dumbass. Moron. Too stupid" - conflict with Donald Trump

If not the biggest, then the most enduring test for both the Federal Reserve and Jerome Powell personally has been Donald Trump.

Despite the fact that it was Trump who proposed Powell's candidacy to head the Fed in 2017, the first conflicts between the politician and the financier began in 2018. The businessman who became president both terms reacted extremely sharply to the Fed's decisions to raise the interest rate or keep it at a high level. How acutely - it was always possible to judge by the politician's posts on social networks.

Jerome "Too Late" Powell has done it again!!!! He is WAY too LATE to react and frankly, WAY too angry, WAY too stupid and WAY too POLITIZED to hold the position of Fed Chairman.

The head of the White House did not limit himself to insults - he also repeatedly threatened Powell with dismissal if he did not start lowering the key rate.

Jerome Powell did not get into a verbal altercation with the president, did not respond to rudeness, did not comment on the policy of the head of the White House. And he explained his position simply: "We don't take sides. We don't pit one against the other and we stay away from issues that are not our responsibility. We are simply focused on ensuring economic stability in the interests of all citizens."

This dubious status quo appeared to be destroyed in January 2026 when it was revealed that an investigation had been launched against Jerome Powell.

The formal reason for it was the cost of reconstruction of two Federal Reserve buildings in Washington: it rose from $1.9 billion in 2017 to $2.5 in 2023. In July 2025, Powell had to explain this growth in front of the U.S. Senate.

"No one in the civil service wants to engage in a large-scale reconstruction of a historic building during their term. It is much nicer to leave it to the successors - and the current situation perfectly shows why this is so," the Central Bank head told the senators.

Nevertheless, the Republican side of Congress and other supporters of President Trump have continued to develop a public narrative about a "Taj Mahal in downtown Washington" that is supposedly being built at Powell's behest.

A few days after the hearing, Congresswoman Anna Paulina Luna asked the Justice Department to check whether there were no grounds for a criminal case against Powell. Mrs. Luna believed that the Fed Chairman might not have told the whole truth about the planned works and their price.

At about the same time, the President personally came to inspect the construction site.

It marked the first visit by a White House chief of staff to a U.S. central bank in 20 years.

Afterward, Trump wrote on social media Truth: "Let's just bring this to a close and more importantly, LOWER THE PRECEDENT BIDS!"

Powell left the rate unchanged. In November, prosecutors opened the case, by January the first subpoenas were sent to the Federal Reserve, and the media became aware of the process.

After that, the head of the Fed for the first time allowed himself to comment on the situation frankly:

The threat of criminal prosecution arises because the Fed sets interest rates based on its own assessment of what is in the public interest, not the President's preferences.

Many people, including Republicans, were ready to agree that the case was nothing but political pressure. North Carolina Senator Thom Tillis even blocked a committee vote on the nomination of a new Fed chief because of the investigation against Powell.

In the end, federal judge James Boasberg also concluded that there was no crime and that the prosecution was politically motivated. "There is ample evidence that the primary - if not the only - purpose of these requests [subpoenas - Oninvest's note] is to pressure Powell to either obey the President or resign to make way for a more convenient Fed chief. In doing so, the government has presented no evidence that Powell has committed any crime - except to displease the president."

The case against Powell was closed. But D.C. Attorney General Janine Pirro was quick to say the investigation could reopen. "Any construction project where cost overruns are nearly 80 percent of the original budget deserves a serious audit. And these people are in charge of monetary policy in the United States?".

Jerome Powell: the bottom line.

The question of how to evaluate the years of work of the Fed under the leadership of Jerome Powell is still open. Judging strictly by key economic indicators, the merits of the Central Bank head seem modest but obvious. The unemployment rate under Powell was around 4% (with a jump to almost 15% during the pandemic) - historically a very low figure.

The labor market has recovered much faster since the pandemic than it did after the 2008 economic crisis, although the labor market has lost momentum in the last couple of years - few hires, few self-determined transitions.

As for the annual inflation rate (CPI), after the pandemic, the Fed failed to fix its rate at the desired level. The regulator fixed the cherished figure of 2% at the beginning of 2026, but after that it went up again - against the background of the war with Iran.

But a far more important outcome of Jerome Powell's 8 years in office seems to have been articulated by Michael Folkender, former US Deputy Treasury Secretary in Donald Trump's government:

Fed chiefs are usually judged by how they handled inflation. From that perspective, Powell would probably not go down in history with the best results. But I think he will probably be remembered for the way he fought for Fed independence.

The 73-year-old financier intends to continue to do so: Powell said he plans to remain on the Fed's Board of Governors after leaving the chairmanship: his term expires in a year and a half. The last time this happened at the Fed was almost 80 years ago.

This article was AI-translated and verified by a human editor